Your Software Is About to Start Paying Its Own Bills

For 200 hundred years, the financial system has been built for human hands.

Payments settled in days because humans needed days. Fees existed because humans paid people to staff the desks, run the wires, and resolve the disputes. The whole system was sized for analog speed and analog volume.

We finally have an alternative, and it didn’t arrive because Wall Street decided to upgrade the plumbing. It arrived because the open architecture of blockchain, with its immutability, transparency, and security, turned out to be the only foundation that could support stablecoin settlement and agentic payments at the scale software is about to demand.

Here’s the math that makes it concrete.

A USDC transfer on Base costs roughly one one-hundredth of a cent.

The same payment on a Stripe card rail costs nearly thirty-one cents in fees.

For a $0.31 transaction, the first rail leaves the merchant with $0.3099. The second leaves the merchant with $0.001.

What Just Happened

On May 21, the crypto market-making firm Keyrock published “Who Pays the Agent?” in partnership with Coinbase, Tempo, and Virtuals.

They curated, 12 months of actual data stemming from real machine-to-machine payments; not slides from a venture pitch.

The findings should tell you where the puck is going:

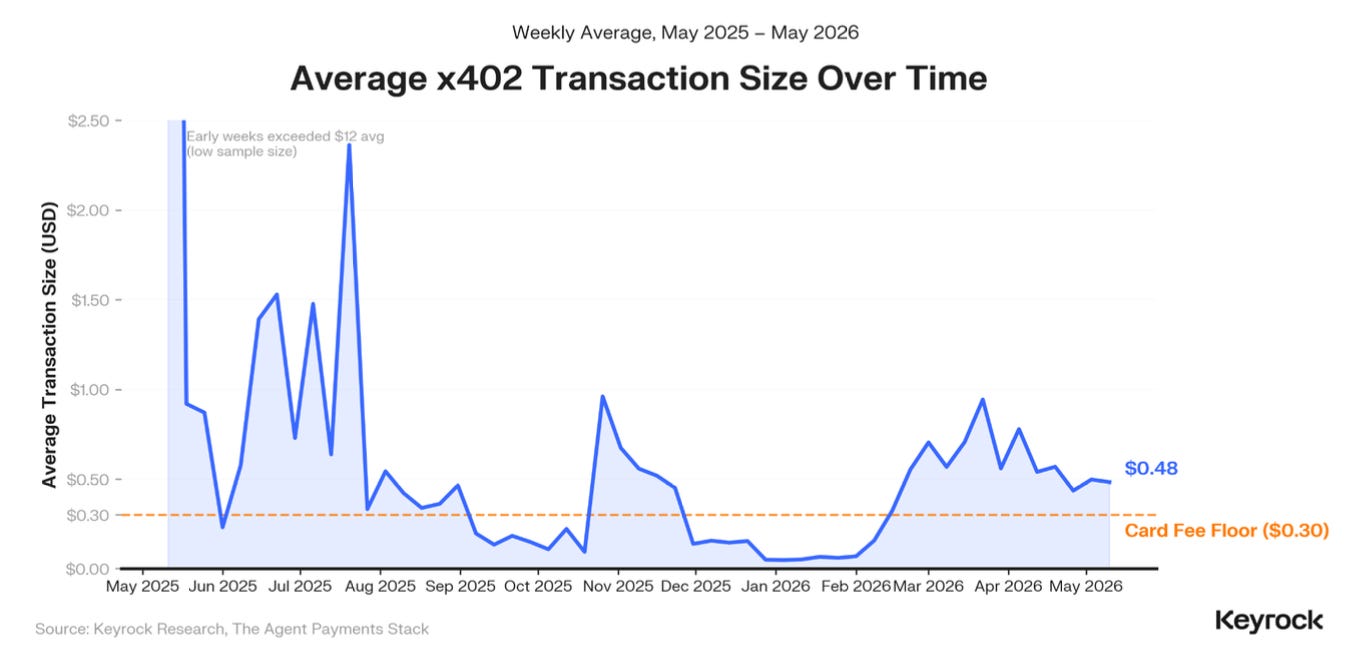

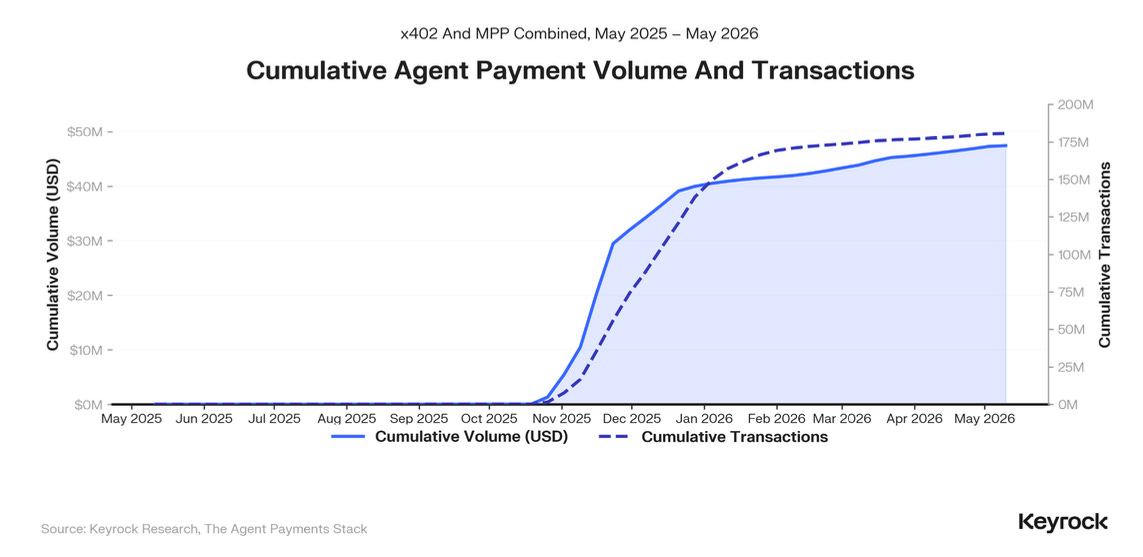

AI agents settled over $73 million across roughly 176 million transactions between May 2025 and May 2026, with 98.6% settling in USDC.

It’s worth noting that Keyrock themselves flag a caveat here revealing that onchain analysis might suggest a meaningful portion of those transactions reflect artificial or gamified activity, and the headline volume figure may overstate genuine commercial throughput by as much as half….but still, not nothing!

The more grounded signal is the sustained $11 to $15 million weekly run rate in Q1 2026, with a peak of $15.3 million in late March, coinciding with genuine integrations like Nansen and Alchemy rather than airdrop farming.

The agentic economy stopped being a pitch deck and started being an ecosystem with a measurable, if early, run rate.

Why the Dollar Can’t Carry This

Think about the post office and email.

The postal system works fine for shipping a letter, but it can’t carry a message that costs one ten-thousandth of a stamp to deliver. Email didn’t solve that by reinventing the post office; it built a different network with a different cost structure underneath. Both systems still exist. They serve different problems.

Agentic commerce is the same situation, just 50 years later.

Card networks were engineered around a human shopping at a register. Settlement clears in days. A floor fee exists because the rails are expensive to operate and someone has to pay for the chargeback infrastructure. None of that scales down to a software agent paying a data feed three cents for a real-time market quote.

Erik Reppel, who built x402 at Coinbase, frames it this way:

“Paying with stablecoins is actually the logical equivalent to paying in cash.

If I hand you $10, there’s no person who’s going to take 3% of the $10.”

That’s the deeper point. Blockchains haven’t merely made payments cheaper. They’ve returned payments to their pre-intermediation economics.

When three out of four agent transactions cost more in fees than they’re worth, the existing rails become structurally impossible to use.

The Four Lanes of the New Highway

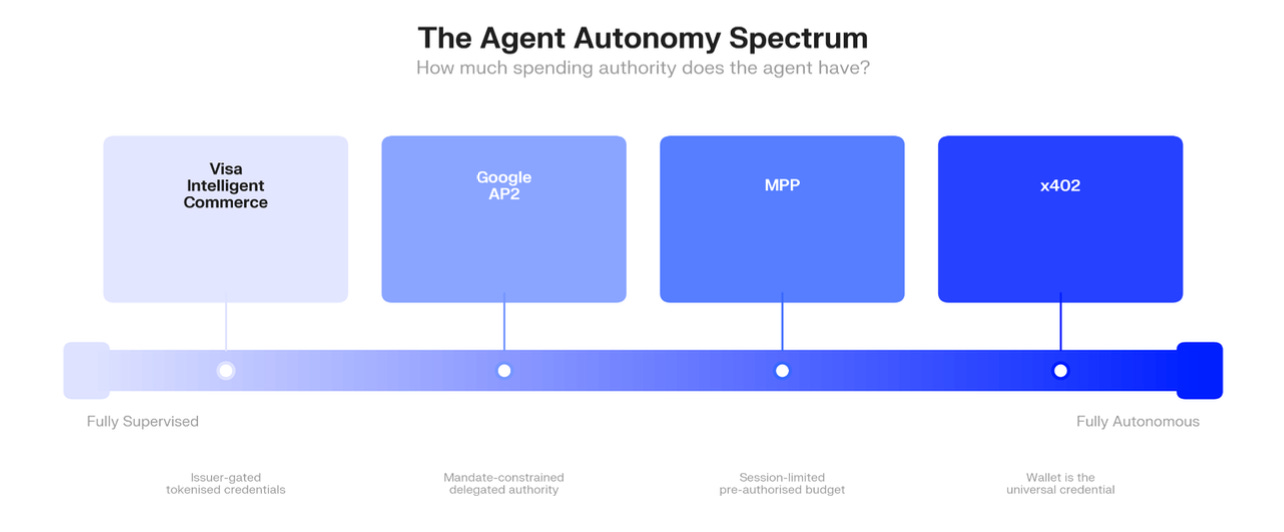

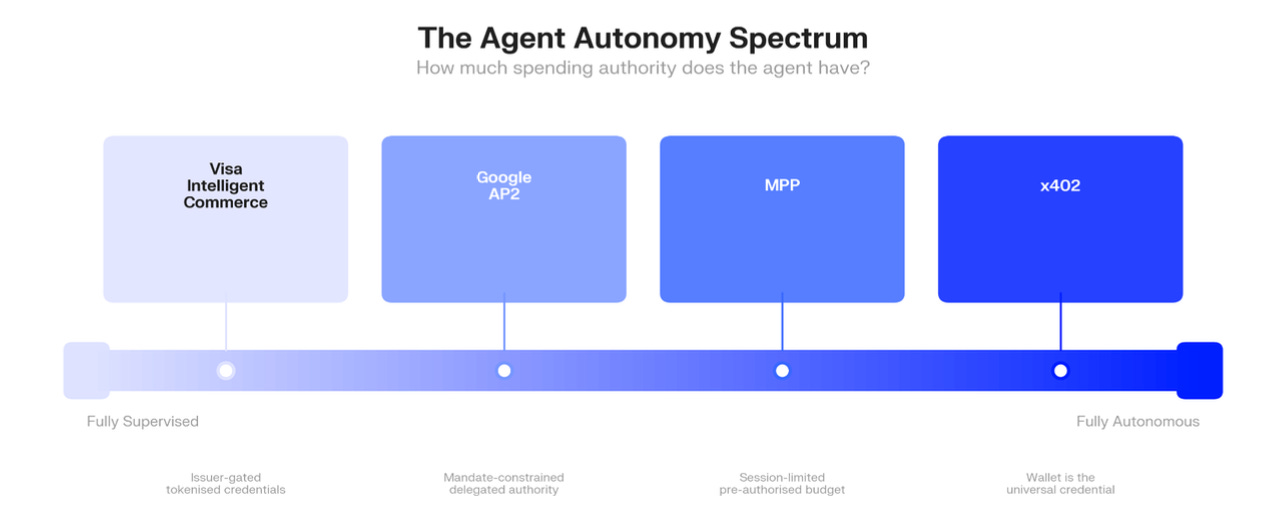

4 major protocols are emerging to serve this market. The names and functions matter more than the technical implementation.

Visa extended its existing card rails to provision AI-ready tokenized credentials agents can present at checkout.

Google released AP2, an authorization layer that lets users delegate spending authority to agents using cryptographic mandates.

Stripe and Tempo co-authored the Machine Payments Protocol (MPP), a payment-method-agnostic standard handling stablecoins, cards, and Lightning through a single HTTP flow.

Coinbase built x402, repurposing the long-dormant HTTP 402 status code to enable stablecoin payments between machines. (remember, I talked about them at Consensus)

The meaningful frame: these aren’t all competing on the same field; they’re stacking. AP2 handles authorization on top while x402 and MPP handle settlement beneath it.

Actual value moves on blockchain rails below that. Visa runs as a parallel lane for transactions where tokenized cards make more sense than stablecoins. For the longer arc on why x402 specifically matters, my earlier DIEM and VVV thesis walked through how this was already showing up in agent-payment tokens.

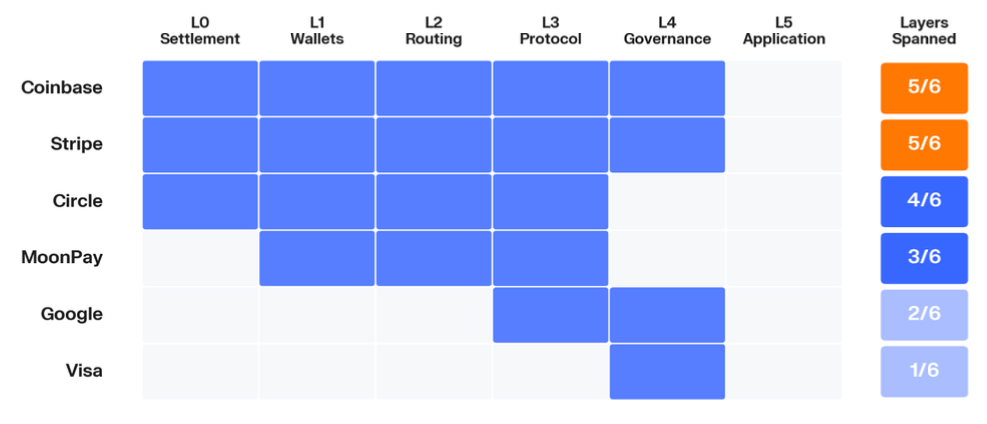

Who’s Building Which Lanes

Coinbase and Stripe each span five of the six layers Keyrock maps.

Coinbase covers settlement (Base), wallets (AgentKit), the payment protocol (x402), and governance as a 402 Foundation partner. Stripe mirrors this through Tempo, Privy, Bridge, and MPP. Circle covers four layers. Google and Visa span two and one respectively.

The legacy incumbents are paying real money to claim position.

Capital One acquired Brex for $5.15 billion specifically for its programmable card infrastructure.

Mastercard purchased BVNK for $1.8 billion.

Stripe acquired Bridge for $1.1 billion.

The named deals total more than $8 billion in twelve months. If you’re wondering whether the establishment is fighting or buying in, the M&A number is your answer.

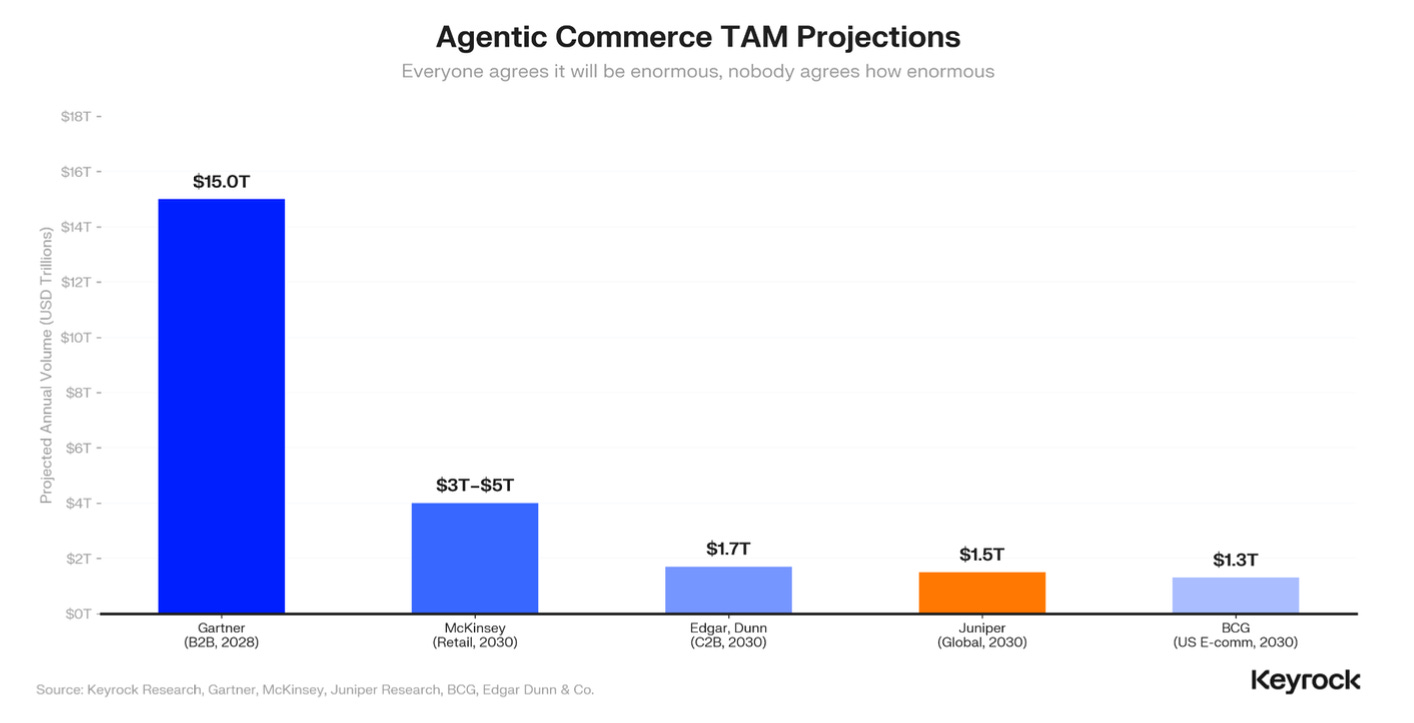

The Size of the Prize (where stuff gets nutty!)

Industry forecasts say this gets big. Like, really big.

Gartner projects $15 trillion in AI-agent-intermediated B2B purchases by 2028.

McKinsey estimates $3 to $5 trillion in retail agentic commerce by 2030.

Juniper Research forecasts $1.5 trillion.

BCG puts US e-commerce alone at $1.3 trillion.

Sure, it’s absolutely worth treating these with appropriate skepticism. Getting from today’s $600 million annualized run rate to $1.5 trillion in 4 years implies a compound annual growth rate of roughly 350%.

For context, the entire stablecoin market grew at about 100% CAGR over 6 years. The agentic projections require growth 3-5x faster than the most explosive period in stablecoin history.

That doesn’t make them impossible. It makes them aspirational, contingent on infrastructure, trust, and regulation all maturing in parallel. The infrastructure is mostly ready. The other two are not.

What This Means If You Keep Finance Honest

This is the section I’d ask you to read twice.

Most of the agentic commerce coverage you’ll see this year is breathless about the upside, with little of it speaking to the constituencies who actually keep finance honest: auditors, fund administrators, custodians, vendors, and compliance officers.

Those teams don’t have a playbook for this yet, because their existing playbooks all assume a human authorizer somewhere upstream.

A few questions each constituency is sitting with.

For external auditors, the question is who signs the audit trail when a software agent initiates a transaction. Google’s AP2 cryptographic mandate framework is the first serious substitute for human authorization. Auditors should be reading those mandate structures the way they read powers of attorney today.

For fund administrators, the question is how reconciliation works when trade count goes from hundreds per day to potentially millions across agent-originated activity. Existing NAV strike processes weren’t designed for sub-second activity at this density.

For qualified custodians, the question is what custody actually means for an agent wallet. Once funds land on stablecoin rails, they cannot be recalled, and there’s no chargeback. The BitFinance Vaults Deep Dive covers the broader programmable-custody architecture being rebuilt around this.

For vendors and merchants, the lesson is that agentic commerce runs on protocol endpoints, not visual checkout flows. OpenAI’s ChatGPT Instant Checkout was shelved in March 2026 after only about 30 Shopify merchants used it.

For compliance officers, the question is what an “agent of record” looks like inside a KYC stack. American Express launched Agent Purchase Protection in April 2026, covering erroneous purchases by verified agents in its registered ecosystem. That’s the first commercial answer. Expect more.

The Risks Worth Naming

Concentration is the obvious risk, and the report makes the picture sharper than most coverage admits. 98.6% in USDC means Circle is a single point of failure for the entire settlement layer.

Sharper still: roughly 74% of agent payment volume flows through Coinbase’s chain (Base), uses a stablecoin Coinbase co-issues (USDC), and is processed by Coinbase’s facilitator. That’s the most vertically integrated payment stack assembled since Stripe built its relationship with fiat banking. The protocols are open. The infrastructure isn’t.

Regulation is the second binding risk. 3 frameworks reach enforcement in a five-week window this summer:

MiCA’s transitional period ends July 1,

the GENIUS Act’s implementation deadline is July 18, and

the EU AI Act’s high-risk obligations take effect August 2.

None contain provisions for autonomous machine-to-machine transactions. The UK Competition and Markets Authority moved first in March 2026, placing full legal responsibility on businesses deploying AI agents, with fines up to 10% of worldwide turnover.

Expect other jurisdictions to follow.

Why Spend Time on This?

The Indicator Project is the work I’m doing on building agentic trading and investment solutions for individual investors, the people without an analyst team. That work is why I read the Keyrock report the morning it dropped.

The trajectory worth holding in mind is bottom-up.

Payment rails have always been rebuilt this way:

volume from below, not decree from above.

What starts as a $0.01 API call eventually pulls $50 SaaS payments onto the same settlement layer, then $500 procurement orders, and eventually flows that institutions currently assume will never leave their existing infrastructure.

The people who pay attention to the bottom of the curve now are reading the same map institutional buyers will be reading in three years. There’s an information asymmetry available, and it’s the cheap kind: the report is already public.

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.