Volatility-Proof Loans Sound Great. That’s the Problem.

I’ve watched a margin call day from the desk side.

Bitcoin gaps down 15% overnight. Clients wake up to notifications telling them they have hours to wire in more capital or watch their collateral get sold out from under them. Some of these loans run on smart contracts, and code doesn’t wait for your wire to clear.

Miss the window and the liquidation executes automatically.

No phone call. No negotiation. No grace.

Over the last couple of years, I’ve built partnerships with digital asset lending desks and helped facilitate roughly $40 million in loans for clients through Maple Finance and Arch Lending.

Liberation Day last April, October 10 when nearly $20 billion in leveraged positions evaporated in a single session, this past February. Each one of those days meant clients scrambling to move assets under a clock.

So when Jack Mallers announced Strike’s new loan this month with the line “Volatility is inevitable. Liquidation isn’t,” I understood exactly why the pitch lands. He’s selling the removal of the worst day in crypto lending.

He’s also charging for it. That’s where this gets interesting.

Buy, Borrow, Die: The Hack Wealthy People Use

Why borrow against your bitcoin at all? Because selling has a price tag.

Sell $100,000 of bitcoin you bought at $20,000 and the IRS wants a cut of the $80,000 gain; call it $19,000 depending on your bracket. Borrow against it instead and you get cash today, keep every point of upside, and owe no tax, because a loan isn’t a sale.

Wealthy families have run this play against stock portfolios for generations. Musk has done it with Tesla shares. Estate planners have a name for the full strategy: buy, borrow, die.

The dying part matters because heirs receive a step-up in basis that erases the embedded gain entirely.

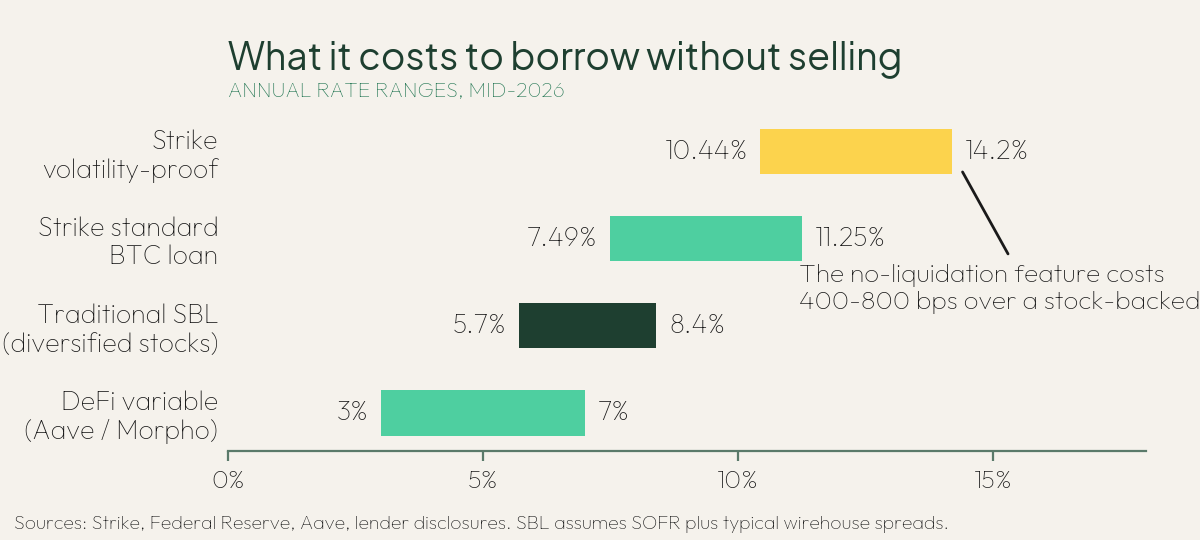

The catch is the rate. A wealthy borrower with a diversified stock portfolio pays roughly 6% to 8%. Strike’s volatility-proof loan runs 10.44% to 14.2%. That spread is the price of the promise.

Annual borrowing rate ranges by lender type, mid-2026. The no-liquidation premium is the widest spread on the board.

What Strike built

Credit where it’s due, the design is clever.

You post bitcoin, borrow up to 45% of its value, and for the six-month term there are no LTV warnings, no margin calls, and no price-based liquidations. Bitcoin could fall 80% and your coins stay untouched, as long as you make your payments. Miss one, and you get a 10-day grace period before Strike can touch the collateral.

For the right borrower, this is a real upgrade. The forced-selling problem, the one that turns a bad month into a permanent loss, is gone. Somebody who borrows a conservative amount, has income to make payments, and has a plan to repay principal gets to ride out a crash that would have wrecked them anywhere else.

The benefit is real, but so is the bill.

Mallers has said the roughly 3-point rate premium goes toward hedges Strike buys in the market to protect itself. Read that again: you’re paying extra so that someone, somewhere, is holding the risk that used to be yours.

Risk in lending never disappears. It relocates. The whole job is figuring out where it went.

Where it Went

Play out 3 futures:

Bitcoin dips 40% and recovers: the product performs beautifully. You would’ve been margin-called on any other platform. Here you sail through. This is the scenario in the marketing.

Bitcoin craters and stays down: your loan is now bigger than your collateral. A rational borrower stops paying and walks away, handing Strike the coins. You’ve effectively bought a put option with that rate premium, and Strike’s hedges eat the gap. Not a disaster for you, but notice you still lost the bitcoin, and here’s the insult on top: surrendering appreciated coins to settle a debt is a taxable event. You can lose the asset and owe capital gains on it in the same afternoon.

Bitcoin is merely down at month six: this is the quiet one nobody markets. Your balloon payment is due, the coins are worth less, and if you can’t repay, the collateral gets sold at the bottom anyway. The liquidation wasn’t eliminated so much as scheduled.

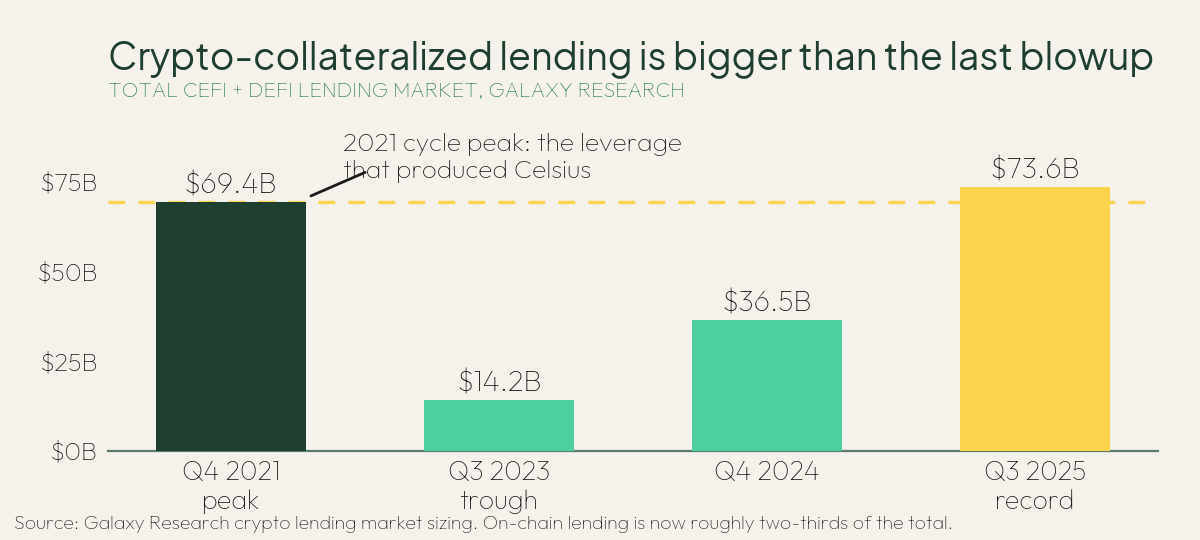

Total crypto-collateralized lending across CeFi and DeFi, per Galaxy Research. The market has now exceeded its 2021 peak.

Buffett Framework Question: When someone offers to take a risk off your side of the table, what are they charging for it, and can they carry it?

Strike hasn’t disclosed what’s in its hedging book.

The lending capital comes through a $2.1 billion facility from Tether, which is also a party to Strike’s pending merger, a related-party setup at least one institutional analyst has flagged. The terms say your bitcoin is never rehypothecated, and they also preserve Strike’s right to pledge collateral to its capital providers.

None of that is an accusation, but it’s a lesson from running diligence on lending partners: anybody telling you that you’ll never get liquidated is carrying an instrument or a counterparty exposure somewhere, and you may not be able to see it.

The 2022 lenders looked vetted right up until $46 billion of customer money got trapped in bankruptcy court.

The Allure of Leverage

In my experience, clients didn’t take these loans to buy houses or manage taxes.

They borrowed against bitcoin to buy more bitcoin. Levering up feels brilliant on the way up and wrecks people on the way down, and I watched both halves of that movie from the desk.

A margin call, for all its cruelty, is a forced discipline.

It caps how wrong things can go. Remove it, and a borrower can ride a losing trade the full six months, paying double-digit interest the whole way down, and still lose the coins at the end. The product’s loudest feature speaks directly to the borrower most likely to misuse it.

Would I take one?

I’ve debated it more than once, and I keep landing in the same place: I’ve seen too many people get wrecked levering a volatile asset, and no product design changes the math of borrowing against something that can fall by half in a quarter.

The fair read is this.

Strike built a better loan than anything the last cycle offered, with lower LTVs, segregated custody, and real protection for disciplined borrowers with income and a repayment plan. If that’s you, at 20% or 25% LTV, this deserves a look. The design isn’t the problem so much as the invitation.

The risk moved into the rate, the term, the hedge book, and your own judgment, and that last one has always been the weakest collateral in crypto.

Until next time…borrow safe my friends.

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.

Sources

The Block: Jack Mallers’ Strike launches ‘volatility-proof’ bitcoin loans (July 7, 2026)

Bitcoin.com News: Strike cuts bitcoin loan terms to 6 months to kill price liquidations

crypto.news: Strike bitcoin loans remove margin calls, add 14% APR trade-off

Galaxy Research crypto lending market sizing (via Yahoo Finance)

Federal Reserve: Estimating Securities-Based Loans Outstanding (FEDS Notes)

Protos: Mallers says no bitcoin rehypothecation at Strike, but what about re-pledging?