Thirteen Trading Trials, Zero Survivors

Outwit, outplay, outlast.

That's the Survivor tagline I memorized as a kid, entranced by a game show that dropped strangers on an island and made them vote each other off one by one.

Twenty-five years later, sitting at my desk testing trading strategies on the new Forge, the parallel was hard to miss. The mechanics are nearly identical. You start with a roster of contestants, you put them through a series of challenges, and the ones who can't perform get sent home.

As it happens, it’s also a fair description of what a quantitative research process is supposed to do to its own ideas. Three contestants stepped onto the island this week.

By Friday, all three were sitting on the jury bench with their torches snuffed.

A few months ago we committed to publishing the strategies that didn’t work alongside the ones that did. Most of what gets written about quant trading shows you the winners. The losers, which are nearly all of them, get quietly buried. We’re trying not to do that. Here’s how the week went.

Meet the cast

Three trading ideas walked onto the beach Monday morning, each with real intellectual pedigree and a publication trail.

None of them were obscure. All of them have been written about by serious people.

The point of the exercise was to find out whether any of them could survive a fee-adjusted, regime-stress-tested, multi-decade backtest. The Forge, our new Mac Studio, did the chopping.

The pre-FOMC drift. A 2015 Federal Reserve paper documented that U.S. equities tended to drift upward in the days before scheduled FOMC announcements. The story was simple: investors got compensated for holding Fed-meeting uncertainty, and the premium evaporated once the news hit. Academic finance treated this as durable, structural, and tradable. Castaway #1.

Turn of the month. An older anomaly, more retail-friendly. Long SPY on the last trading day of each month, hold for a few days. The theory: pension and retirement contributions cluster at month-end and create a predictable flow into equities. Castaway #2.

A regime-filtered version of the pre-FOMC trade. Our own variant, designed to fix what looked like a weakness in the original. Early testing hinted that the drift might live mostly in calm, low-volatility environments, so we built a filter to only take the trade when markets were quiet. Castaway #3.

Each one had a story going in. None of them had immunity.

The Immunity challenge

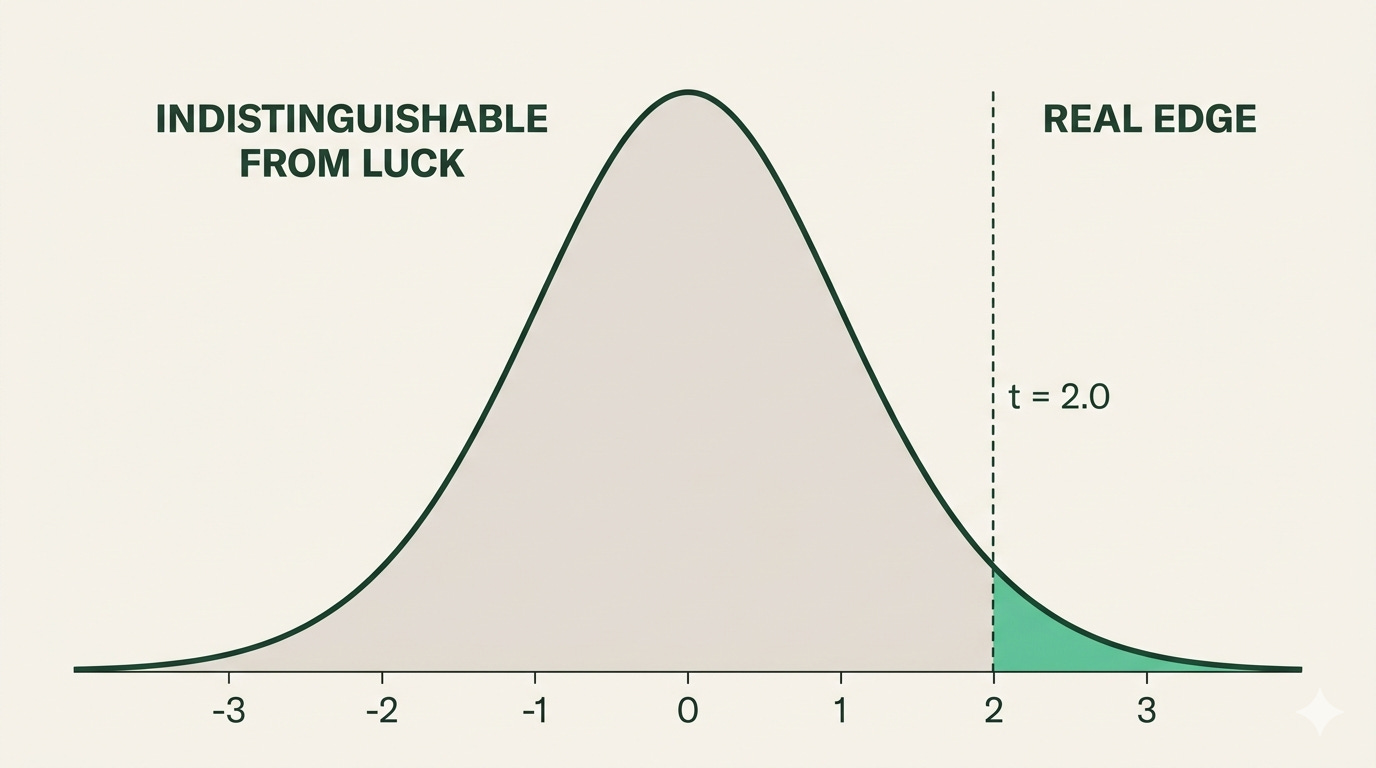

Before we go to tribal council, you need to know about the one number that does most of the work in our framework. It’s the t-statistic.

The t-stat measures how far a strategy’s returns are from what you’d expect from pure luck. A bigger number means we can be more confident the edge is real. A smaller number means we can’t reliably distinguish the strategy from a coin flip run 209 times.

Our bar is a t-stat of 2.0. That corresponds to roughly a 5% chance the observed returns came from randomness alone. Below 2.0, we don’t trust the result enough to move the idea forward, no matter how good the equity curve looks. Think of it as the immunity challenge.

Clear it, you live another week.

Miss it, the tribe gets to vote.

Tribal Council #1: The pre-FOMC drift

This was the most painful vote of the week, because the strategy almost made it.

You’re looking at what twenty-six years of testing on SPY looks like with realistic retail trading costs baked in. Five basis points per side, roughly what a retail subscriber actually pays between commissions and bid-ask spread. 209 trades, a smooth-ish equity curve, and a 22.6% drawdown.

The t-statistic landed at 0.93.

That’s statistician-speak for “indistinguishable from luck.” Damn.

Here’s the curious part that you need to watch out for - accounting for FEES!

Before fees, the same strategy looked legitimately interesting. Sharpe of 0.31. T-stat of 1.57, close enough to the bar that you could tell yourself a story about the next parameter sweep doing the trick. Retail costs alone cut the Sharpe nearly in half and dragged the t-stat below 1.0.

The drift probably still exists somewhere in the microstructure. Retail costs have eaten it whole.

The tribe has spoken.

Tribal Council #2: Turn of the Month

This was the easier vote.

More trades, yes, which should mean more statistical power. But more trades also means more fees, and a drawdown profile that would end careers. At one of our parameter settings, peak-to-trough loss hit 51%. That’s the kind of number that drives retail investors to quit a system well before any hypothetical edge pays out.

Gate 1 never came close to clearing. Torch snuffed.

Tribal Council #3: The Regime Filter

I’ll admit I was rooting for this one. The theory had teeth. If the pre-FOMC drift lives in calm environments, filter out the chaotic ones and the edge should concentrate.

The filter did exactly what we hoped for risk, and nothing we hoped for edge. Drawdowns roughly halved, down from 25% to about 12%. Real risk reduction. The Sharpe ratio, though, barely budged. The implication is that the pre-FOMC effect isn’t being diluted by volatile regimes, it’s been arbitraged down roughly evenly across all of them. Our structural fix fixed the wrong thing.

Filed under: useful lesson, dead strategy.

Why this matters if you’re not a quant

Most strategy writing online shows you one carefully chosen parameter run, on a hand-picked time window, with zero trading costs. You’ve seen the equity curves. They rise from bottom-left to top-right and look like proof.

The three strategies in this post produce similar-looking pictures if you squint. It takes the fee layer, the full parameter sweep, and the 26-year regime backdrop to see what’s actually there, which in all three cases is not enough.

When a signal service or a quant influencer shows you a perfect-looking equity curve, three questions settle most of the argument.

What did they pay in costs?

How many variations did they try before showing you this one?

Does the edge survive in the regimes they didn’t cherry-pick?

Academic papers live in a frictionless world. Retail brokerages don’t.

Where this leaves us

Three strategies, thirteen logged trials, zero advanced.

That isn’t a bad week of research. That’s what a research funnel looks like. The guidance from the literature is roughly 100 to 200 ideas per viable system. We’re on pace.

Next up in the casting pool: VIX term structure trades and crypto funding rate mean reversion. Different failure modes, different data, different stress on the process. If any of them clears the fee-adjusted gates, you’ll hear about it. If none of them do, you’ll hear about that too.

The Forge is earning its keep. The framework is doing what it’s supposed to do, which is vote bad strategies off the island before our capital finds them. The only question is which contestants get cast next.

Moving right along…

This Week In 2 Minutes

$13 Billion Walked Out of DeFi This Weekend (Apr 21)

Bought a small Aave position Friday on solid fundamentals. By Sunday, $5B in deposits were frozen and the position was down 20%, not because Aave’s code failed but because the off-chain plumbing connected to it did. The piece argues the picks-and-shovels trade for this cycle is the regulated intermediary layer (Coinbase, BlackRock, Apollo) sitting one layer above the protocols themselves. The anchor question for any serious crypto allocation: if this position collapses tomorrow, who’s legally on the hook?

I Spent an Afternoon Talking About AI With a Local Nonprofit (Apr 23)

Spent an afternoon with a faith-based nonprofit’s operations team in Durham, walking them through the AI landscape. The framing that landed wasn’t about the tools but about giving people back the hours that administrative friction eats every week. The biggest opportunity for almost any small organization is grant writing, where AI can compress qualification scanning, narrative drafting, and budget work into a fraction of the time. Worth reading if you’re trying to think about how a small team adopts this technology without losing the human work that matters.

Weekly Winners 🏆

Markets shrugged off geopolitical noise and rode an earnings beat into another all-time high on the S&P. Chips ran the table.

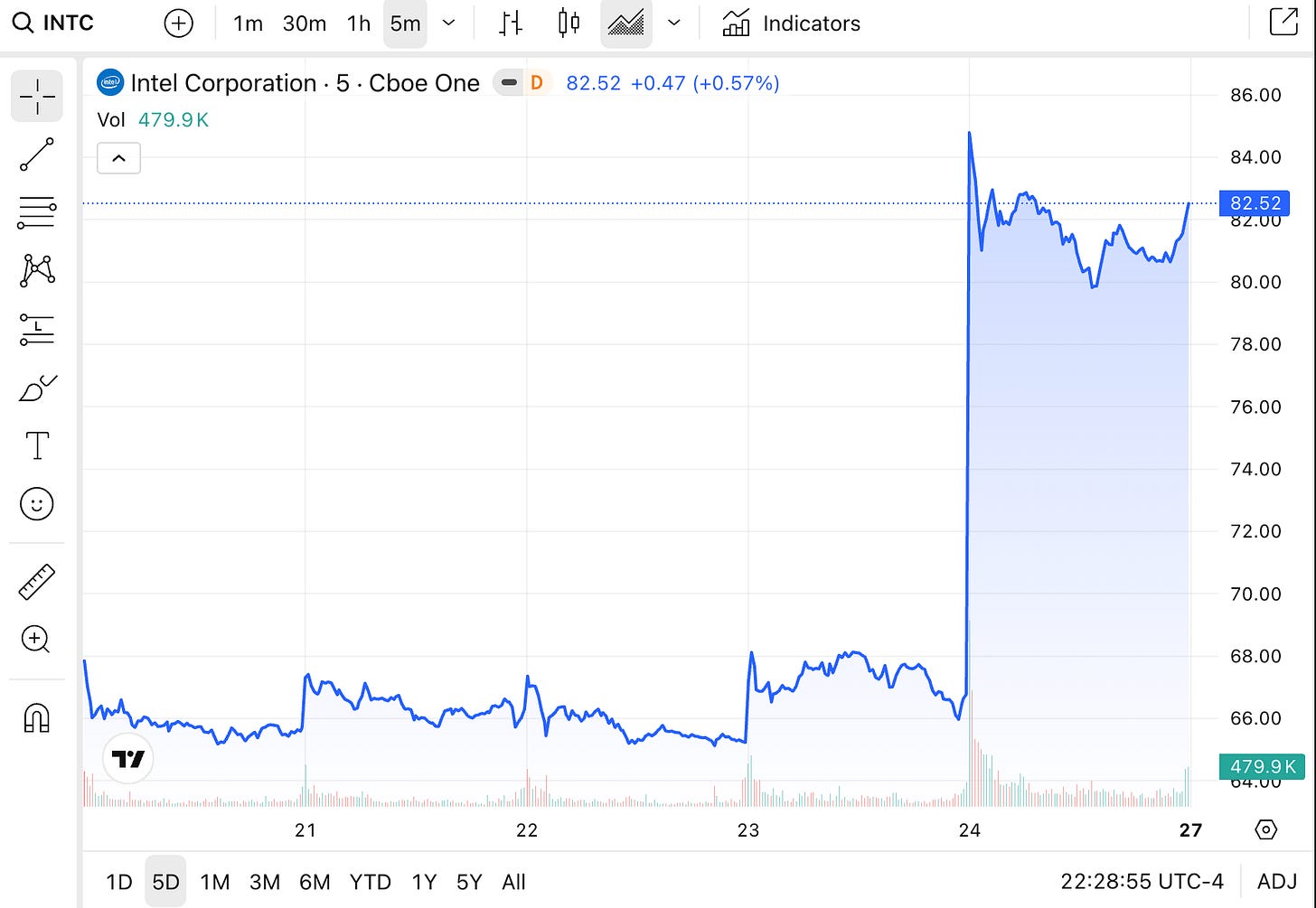

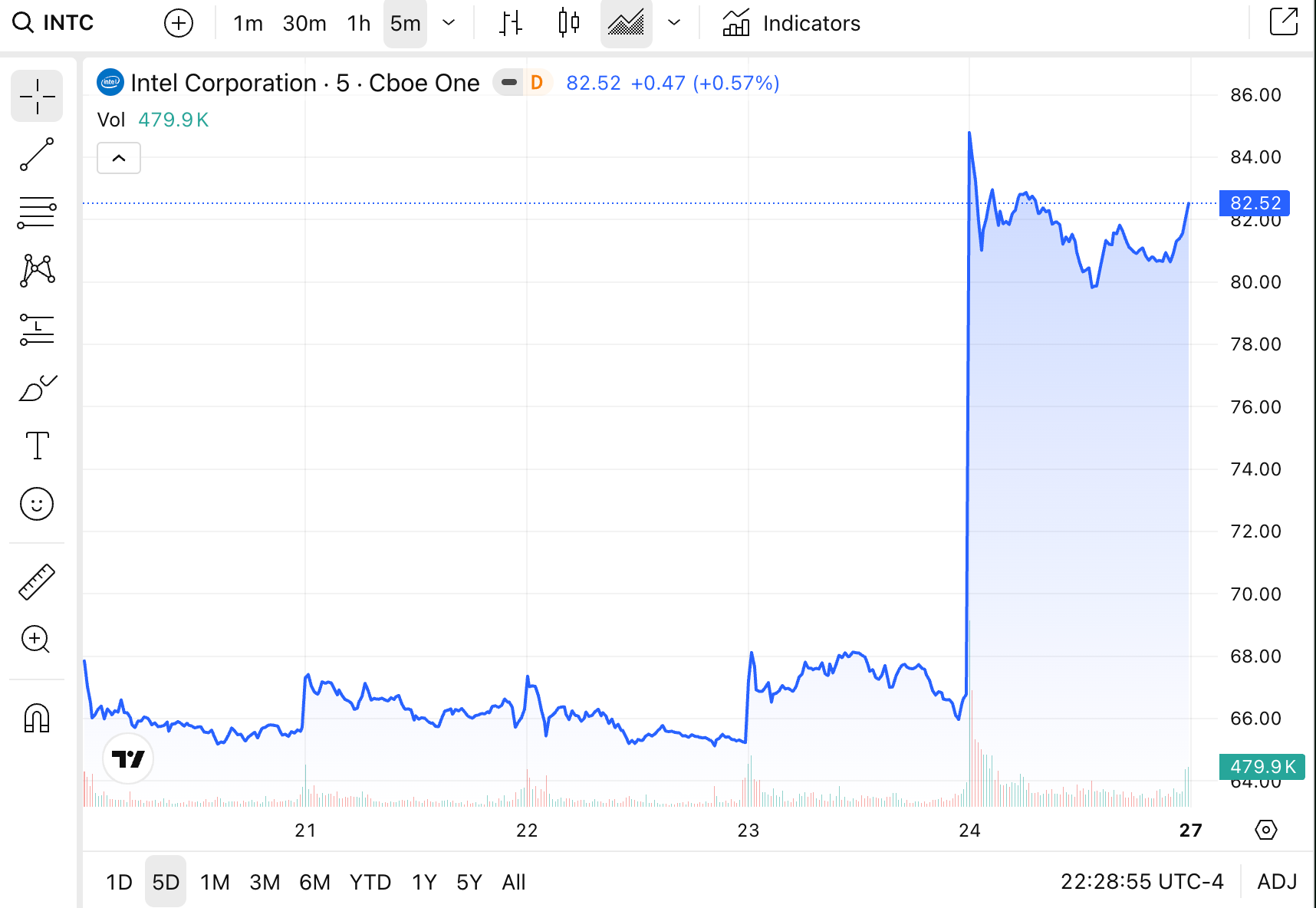

Intel (INTC). One word - YOWZA. Up 23.6% Friday on a blowout Q1 report, the chipmaker’s best single day since the dot-com era. AMD piggybacked for a 14% pop. Semiconductors closed higher for an 18th consecutive session.

Bitcoin. Up 13.6% on the month and on track for its strongest April in a year. Strategy added 34,164 BTC for $2.54B at an average $74,395, the company’s largest buy since November 2024. Holdings now sit at 815,061 BTC.

United Rentals (URI). Top S&P performer mid-week with a 24% pop on a clean earnings beat ($9.71 EPS vs. $8.95 consensus) and raised full-year guidance to $16.9 to $17.4B.

S&P 500. New all-time highs on Wednesday and Friday, closing the week at 7,165. The Nasdaq cleared 24,800. Woot woot!

Weekly Losers 📉

Software took a real hit, consumer sentiment hit a 74-year low, and ETH kept underperforming BTC.

Enterprise software. IBM and ServiceNow delivered ugly prints Thursday and dragged the broader software complex with them. The selloff bled into Palantir on Friday before stabilizing.

HCA Healthcare. Down 8.2% after guiding 2026 profits to the low end of prior range, citing storm-related disruptions from Hurricanes Helene and Milton.

Consumer sentiment. The University of Michigan final April reading came in at 49.8, the lowest in the series’ history going back to 1952. Markets ignored it. Worth watching whether they keep ignoring it.

Ether and DeFi. The ETH/BTC ratio fell nearly 3% on the week to 0.02965, its lowest since mid-March. Lido and Morpho dropped 3 to 4%, with sentiment still soft from last weekend’s $290M KelpDAO exploit.

On Deck

📍 Bitcoin 2026, Las Vegas, Apr 27–29

I’ll be on the ground at The Venetian for Bitcoin 2026 next week. The lineup is the most institutional version of this conference yet.

Saylor on the main stage with Calamos CEO John Koudounis.

AG Todd Blanche and FBI Director Kash Patel headlining the policy track.

Cynthia Lummis, Eric Trump, JD Vance.

The Bitcoin Policy Institute is using the conference to push a de minimis tax framework that would treat small Bitcoin transactions as cash-like, which is exactly the kind of regulatory clarity advisors have been waiting on.

If you’re a BitFinance reader, an RIA, or anyone working on the institutional side of digital assets, come find me. I’m happy to grab coffee, talk shop on the Buffett Bot build, walk through what’s working with the Forge, or just trade notes on what advisors are actually hearing from clients right now. Reply to this email and I’ll send my schedule.

April FOMC meeting. The Fed convenes next week against a backdrop of new equity highs, a 49.8 consumer sentiment print, and a Middle East ceasefire that’s holding for now. Bitcoin traders are watching $79K as the line between continuation and a slip back into the $75K to $77K range.

Big Tech earnings continue. Meta’s 10% workforce cut (~8,000 roles, effective May 20) tells you what to listen for on the call: AI capex discipline. Microsoft buyouts hint at the same theme. Watch how the Street separates AI-driven margin pressure from durable revenue.

Crypto policy watch. Beyond the Vegas conference, the de minimis tax push and the Morgan Stanley stablecoin reserves money market fund (MSNXX) launched this week are the kind of plumbing changes that move the institutional adoption curve more than any single price target.

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.