The Results Are In: What I Learned Putting Real Money Behind an AI-Powered March Madness Model

A few weeks ago, I wrote about building a March Madness trading bot on Kalshi. The system used KenPom efficiency ratings, compared model probabilities to market prices, sized positions with quarter-Kelly, and sent trade alerts to Discord.

The bankroll was $580 and the thesis was straightforward: recreational bettors misprice prediction markets, and a systematic approach should capture the gaps.

The tournament is over and the bets have settled (outcomes below!). But the most valuable thing I got out of the experience wasn’t the P&L. It was a deeper understanding of what edge actually is, where it lives, and why it disappears.

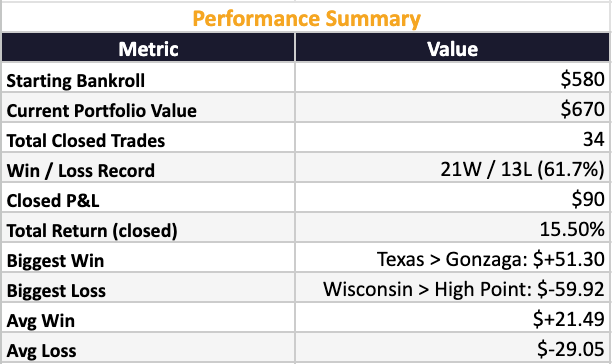

TL;DR Results

Where Edge Lives: The First 20 Bets

With 64 teams and a first weekend packed with games, the early rounds were where the system performed best. We went 12-8 in the first 20 bets. That’s a 60% hit rate against a market that’s theoretically efficient. Not spectacular, but meaningfully above breakeven when you’re sizing with Kelly.

I attribute the success here to information asymmetry.

With 64 teams, casual bettors lean on seed numbers and brand names. They overprice Duke because it’s, you know… Duke and underprice a mid-major with elite defensive efficiency backed by 40 years of data.

Our model didn’t have secret information. It just weighted the right information more consistently than the crowd.

Academic research backs this up. Studies of over 155,000 sporting events found that technical inefficiencies exist in betting odds, but they’re small and they vary by sport. The window is real. It’s just narrow.

The early rounds of March Madness widen that window because more teams means more uncertainty, more uncertainty means more mispricing, and more mispricing means more opportunities for a calibrated model to exploit the gaps.

But it doesn’t last into the later rounds of the tournament which means that edge fades away, fast.

Underdog Teams Lead to Black Swan Outcomes

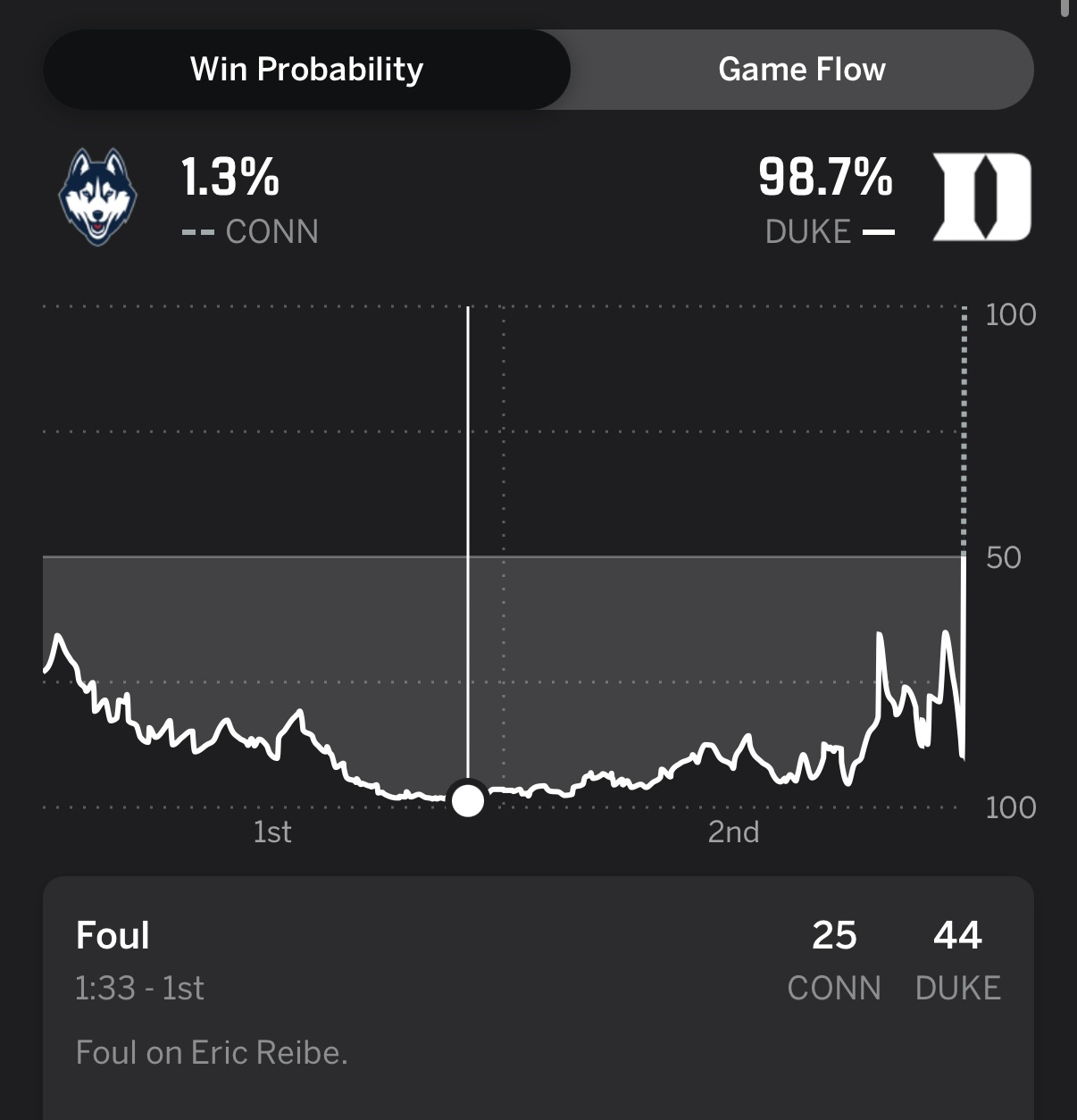

I had two bets placed on Duke in the Elite Eight. Going in, Duke was priced around 70-72% to win. They were the number one overall seed. Cameron Boozer, the National Player of the Year favorite, was dismantling everything UConn tried in the first half. Right before halftime, Duke led 44-29 and UConn had a 1.3% chance of advancing to the Final Four.

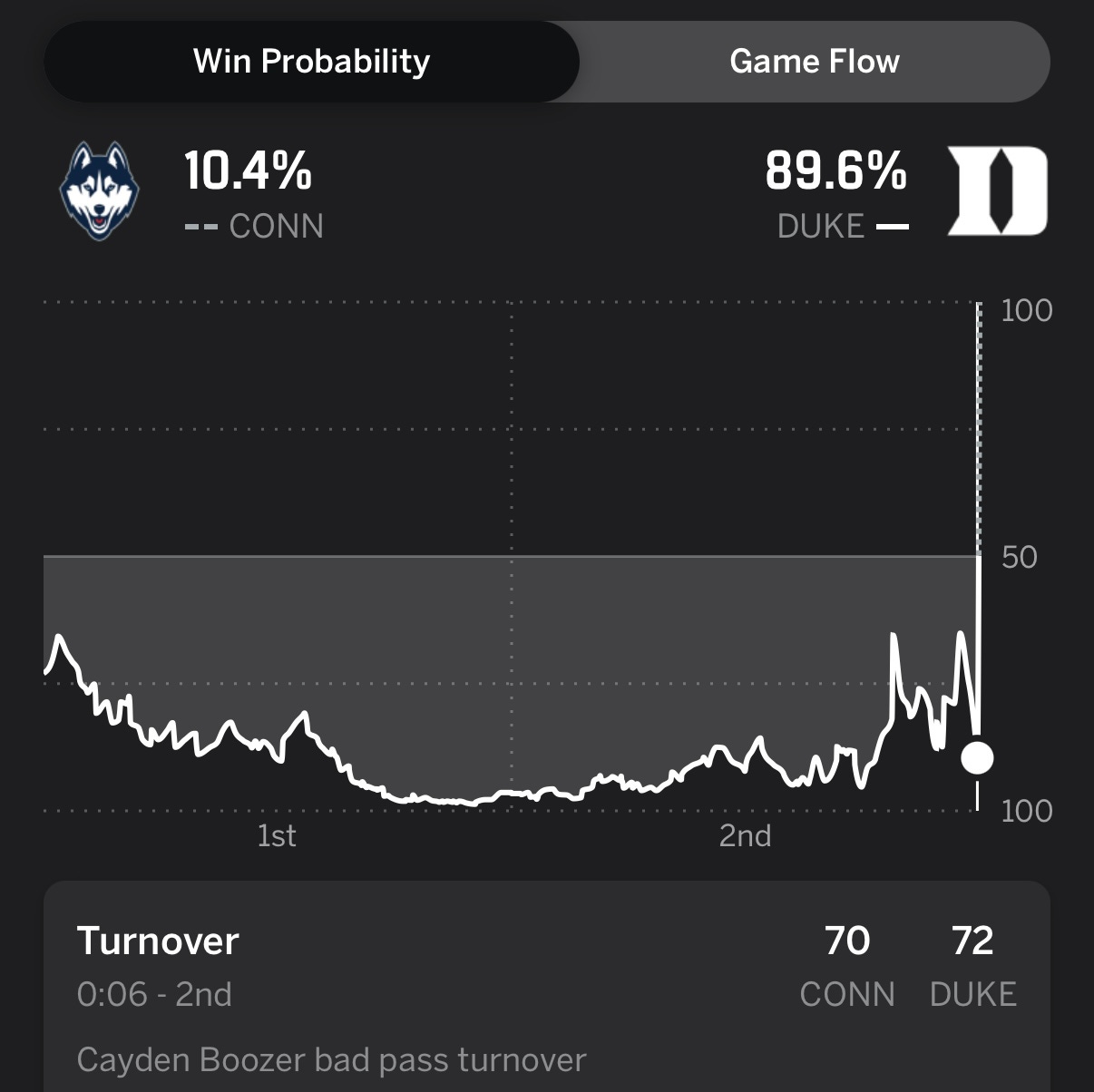

With 6 seconds left, UConn had come back with fury but were still down by 3 with only a 10% chance to win.

Then a freshman named Braylon Mullins, who was 0-for-4 from three, stole an errant pass with less than a second left and buried a 35-footer from the logo. UConn 73, Duke 72. Game over.

Let’s talk about what that actually means in dollar terms.

When Duke’s contract hit 97 cents, I was effectively short $97 to hold out for the last $3. That’s the math. $97 of guaranteed profit evaporated in half a second because I didn’t take it off the table. The marginal benefit of holding was three dollars. The cost of being wrong was everything.

This is the part that gets you.

At halftime, with Duke up 15, there was no rational reason to exit. The model said hold. The market said hold. Every piece of available information said Duke was going to win this game. But prediction markets are PVP (Player-versus-player). There’s no partial credit. Games don’t kind of finish. You either collect or you don’t. And when the contract settles at zero, it doesn’t matter how right you were for 39 minutes.

A 70% favorite is still wrong 30% of the time. And when the price climbs to 95% during the game, you’re psychologically locked in. Nobody sells a 95-cent contract because they’re worried about the 5% scenario. But that 5% scenario is exactly what happened. Duke blew a double-digit lead in all three of their losses this season.

Buffett never really liked this maxim, but I think it’s a strong one to live by:

You can never go broke taking a profit.

That’s not a cliché. It’s risk management. And the lesson isn’t that the model was wrong. The lesson is that being right about probabilities doesn’t protect you from outcomes.

The Disappearing Edge

As the tournament progressed, something predictable happened: the edge got smaller.

In the early rounds, you’re working with 64 teams that casual bettors barely know. By the Sweet 16, the field has been cut by 75%. Everyone’s watched the games. The market has absorbed two weekends of live performance data. The information gap that powered our early-round edge has closed.

By the Final Four, you’re looking at four teams that have each survived the same pressure cooker. Their rosters are well-scouted. Their tendencies are public. The matchups get tight. Michigan was a 1.5-point favorite. Illinois was favored by 2.5. These are coin-flip games dressed up with a slight lean.

I seriously considered sitting out the semifinals. Not because I’d lost confidence in the model, but because the model itself was telling me the edge wasn’t there. When your calibrated probability and the market’s price converge, the honest move is to do nothing. Knowing when not to bet is the most underrated skill in any market.

The Spectrum of Edge

This tournament reinforced something I’ve been thinking about for a while: edge exists on a spectrum, and its relationship to scalability is inverse.

At one end, the S&P 500. The most analyzed, most arbitraged, most liquid market on the planet. Finding consistent edge there is nearly impossible because millions of professionals are competing on every data point. At the other end, genuinely illiquid markets. A micro-cap stock with three analysts. A prediction market on an obscure event. A first-round NCAA game where a 12-seed has elite tempo control that casual bettors haven’t studied. Edge can be enormous in those pockets. But you can’t size it up. The liquidity isn’t there.

March Madness compresses that entire spectrum into three weeks. The early rounds are the illiquid end: information gaps, mispricings, but limited capital deployment per game. The Final Four is the S&P 500: efficient pricing, converging information, margins so thin that the house edge alone wipes out any remaining advantage.

The lesson for investing is the same. The biggest edges live where most people aren’t looking. But the moment a market gets crowded with attention, the edge collapses.

True in crypto.

True in venture.

True everywhere.

Why You Can’t Backtest Chaos

KenPom data is season-specific. The players who generated those efficiency ratings won’t be on the same rosters next year. With NIL deals reshaping college basketball, star players transfer constantly. You can’t meaningfully backtest a March Madness model the way you’d backtest a mean-reversion strategy on SPY. The inputs reset every season.

And then there’s the randomness problem. No model accounts for a 19-year-old from Greenfield, Indiana, stealing a pass and hitting a 35-footer to send his team to the Final Four. That’s not noise in the data. That’s the fundamental nature of the game.

Sports contain a level of irreducible randomness that financial markets, for all their volatility, don’t match. People love sports because of that randomness. But it makes them a terrible environment for building repeatable, systematic edge.

The Bottom Line

There’s an old line, usually attributed to Buffett: if you’ve been at the poker table for 30 minutes and you can’t figure out who the sucker is, you’re the sucker.

Remember that every time you open your Kalshi app and look at where the house and the sharps are pricing things. They have more information than you. They have faster models than you and they’ve been doing this a lot longer.

The house edge, the emotional pull, and the irreducible randomness of athletic competition make it structurally hostile to systematic profitability. Any edge you find is temporary, narrow, and impossible to compound.

Trade accordingly friends.

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.