The Million Dollar Mirage: What Game Show Prizes Teach Us About Real Returns

I remember watching “Who Wants to Be a Millionaire” when it premiered in 1999.

Regis Philbin would lean forward, pause dramatically, and ask:

“Is that your final answer?”

The million dollar prize felt monumental.

Life-changing.

The kind of money that let you quit your job and never look back.

I wanted to be on the show so bad that I practiced at home when the game came out for “Personal Computers” via the relic known as a CD ROM.

Twenty-six years later, the prize is still a million dollars.

The show hasn’t gotten cheaper to produce. Ad rates have increased. Regis has been replaced (twice). But the grand prize sits frozen in late-90s amber, quietly losing value with every passing year.

This is not a complaint about game shows.

It’s an observation about something more important: the slow, invisible erosion that affects every portfolio, every retirement plan, and every long-term financial assumption we make.

The Math Behind the Mirage

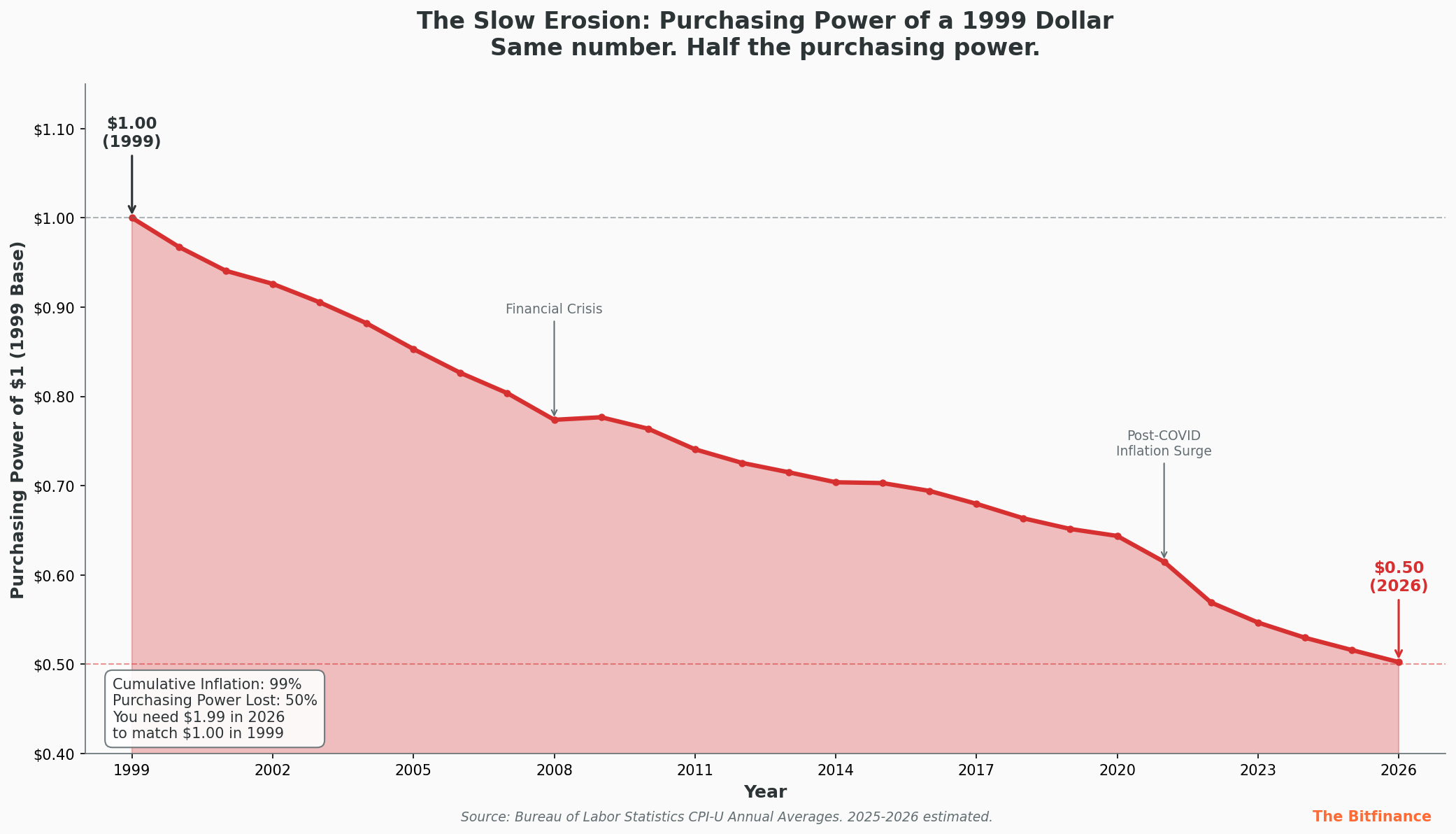

A million dollars in 1999 had the purchasing power of roughly $1.95 million in 2026, according to Bureau of Labor Statistics CPI data. That’s a 95% cumulative increase over 27 years. Put another way, a dollar today buys about 51 cents worth of what it could in 1999.

The prize hasn’t changed. Your purchasing power has.

And it gets worse when you factor in taxes. A million dollar game show win typically nets around $600,000 after federal and state taxes take their share. Adjust that for inflation, and you’re looking at the equivalent of roughly $300,000 in 1999 purchasing power.

Congratulations!

You’ve won enough for a house down payment in a decent school district. Woot!

Family Feud: Where Things Get Really Uncomfortable

If “Millionaire” represents the flagship example, “Family Feud” represents the structural worst of the category.

The Fast Money grand prize has been $20,000 since September 2001.

That prize is split five ways, giving each family member $4,000.

Before taxes.

Here’s the math that no one discusses:

$20,000 in 2001 required approximately $36,000 in 2026 to maintain equivalent purchasing power.

The prize has lost nearly 45% of its real value while Steve Harvey makes increasingly shocked facial expressions at answers that probably weren’t that surprising.

The show still draws millions of viewers. The production costs remain low (estimated at around $1 million per episode). Ad revenue continues to flow. But the contestant value proposition has quietly deteriorated by nearly half.

The Broader Pattern

This isn’t unique to game shows. It’s a feature of every system that anchors to nominal numbers.

Social Security benefits get adjusted for inflation. CEO compensation packages get restructured regularly. But game show prizes, savings account interest rates, and many employment benchmarks remain frozen for years or decades at a time.

“Wheel of Fortune” offers a million dollar wedge that has been won exactly five times in the show’s history with an episode catalogue of over 8,000.

The typical bonus round win averages around $40,000. “Jeopardy!” pays whatever contestants actually win, which varies wildly. “The Price is Right” showcase packages run between $40,000 and $80,000, which sounds impressive until you realize the show has been running since 1972.

The nominal numbers sound substantial because we’ve been conditioned to respond to them.

A million dollars still feels meaningful.

But the purchasing power reality tells a different story.

What This Means for Your Portfolio

The game show example is instructive because it strips away the complexity that obscures this dynamic in more sophisticated financial contexts.

When someone reports a “6% annual return” during a period of 4% inflation, the real return was 2%. When a savings account offers “high yield” at 4.5% while inflation runs at 3%, you’re barely treading water.

When a salary stays flat for three years during moderate inflation, that’s not stagnation. It’s a pay cut.

The financial services industry has every incentive to report nominal returns.

They’re bigger numbers.

They look better in marketing materials.

They make last year’s performance seem more impressive than it was.

But real returns, after inflation, are the only metric that matters for long-term purchasing power.

The Incentive Structure Tells the Story

Why haven’t game shows updated their prizes?

The incentive structure provides the answer.

The word “million” still carries psychological weight, even as its purchasing power diminishes. Audiences respond to the drama. Production costs stay flat while the real value of prizes declines.

Networks capture the spread between what they used to pay in real terms and what they pay now.

It’s not malicious. It’s simply rational behavior given the incentives. Contestants still apply in record numbers. Ratings remain strong. The system continues to function.

This same dynamic plays out across financial products, employment contracts, and institutional arrangements of all kinds. Nominal anchors persist long after their real value has eroded. The entities benefiting from this erosion have no incentive to highlight it. Those affected by it often don’t notice until the gap becomes undeniable.

The Takeaway

The million dollar prize was genuinely transformational in 1999. In 2026, after taxes and inflation adjustment, it’s a nice windfall. Maybe enough to pay off some debt, fund a few years of college, or make a meaningful dent in a mortgage.

That’s the quiet tragedy of nominal thinking.

The number hasn’t changed.

Your expectations were just calibrated to a different era.

The next time you see a financial product promising impressive nominal returns, or a prize pool that sounds substantial, or a salary benchmark that seems generous, ask the more important question: what does this buy?

The answer might look different than you expected.

If this framework for thinking about real vs. nominal returns is useful, share it with someone who might benefit. And if you have game show inflation examples I missed, I’d genuinely like to hear them.

— Matthew

X: @bit_finance_

Want to level up your life?

Read more.

We took 1,300+ pages of wisdom from the Oracle of Omaha and condensed it into a snackable, easy-to-read guide for digital asset investors. Pick up your copy today!