The Greatest Roster in Sports History Can’t Save This Stock.

This weekend, Rory McIlroy walked off the 18th green at Augusta National as a back-to-back Masters champion. He hugged his daughter Poppy. He put on a second green jacket. He joined Jack Nicklaus, Nick Faldo, and Tiger Woods as the only golfers in history to win consecutive titles at the Masters. Six major championships and counting.

Scottie Scheffler finished one shot behind him. Between the two of them, they have four green jackets, eight major championships, and 60 combined PGA Tour victories.

Both were wearing Nike from head to toe.

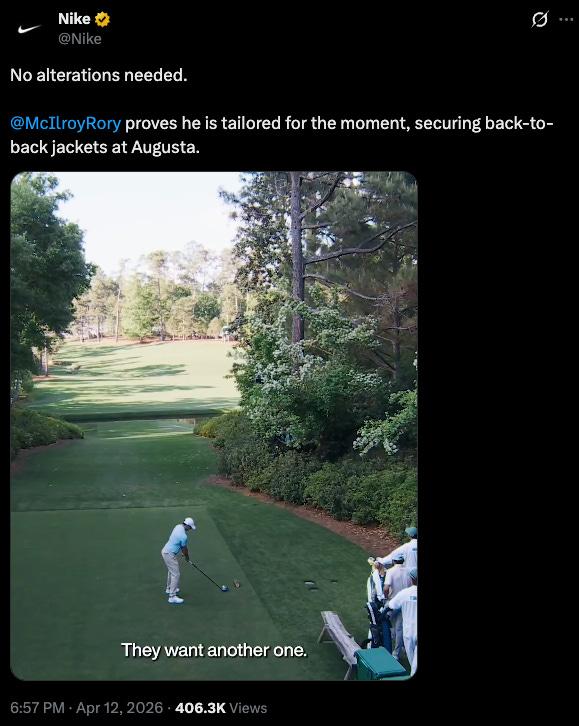

Within hours of McIlroy’s win, Nike dropped one of the cleanest sports ads of the year. Black background, swoosh, and a single line: the greatest golfers in the world don’t want a jacket, they want another one. It racked up 345,000 views, 10,000 likes, and nearly 600 retweets overnight. The creative department is still elite. The cultural antenna is still perfectly tuned.

And the stock?

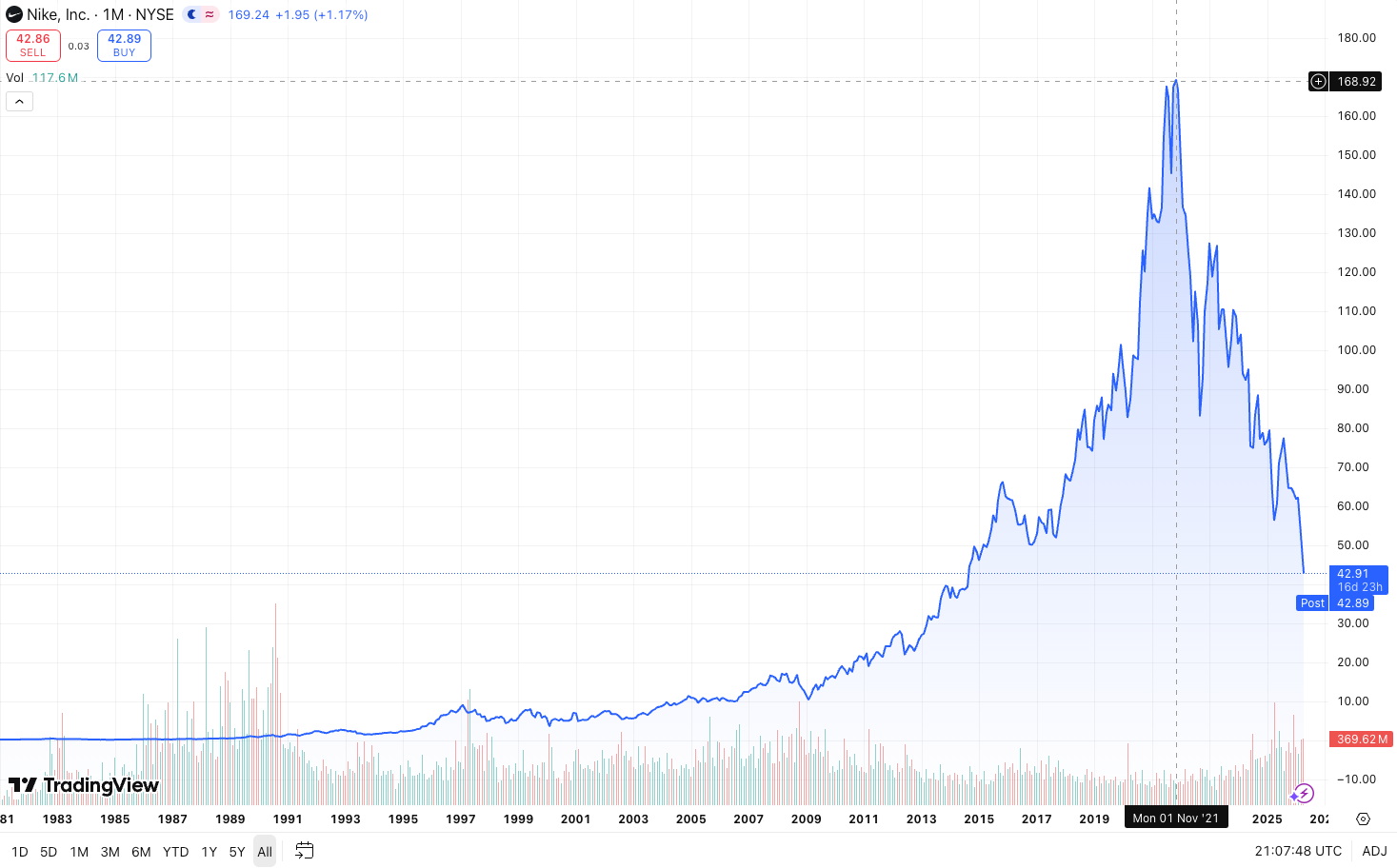

Currently sitting around $42. The price is down 76% from its all-time high of nearly $180, and trading at its lowest level since 2014. A company that employs the two best golfers on the planet, the most dominant basketball player of the last two decades, and the most decorated female tennis player in history cannot get out of its own way on Wall Street.

That’s the paradox I want to examine because it’s worth understanding. It tells you something important about the difference between brand power and business fundamentals.

Buffett Framework:

“Would I pay $67 billion for a company whose greatest competitive advantage, athlete endorsements, is failing to generate shareholder returns?” That’s the question Buffett would ask and it’s the one Nike investors should be asking right now.

The Numbers Are Brutal

In November 2021, Nike touched an intraday high of $179.10. The stock was powered by a pandemic-era boom in direct-to-consumer sales, strong momentum in Greater China, and a broader market environment that rewarded growth at any price.

Every one of those tailwinds reversed.

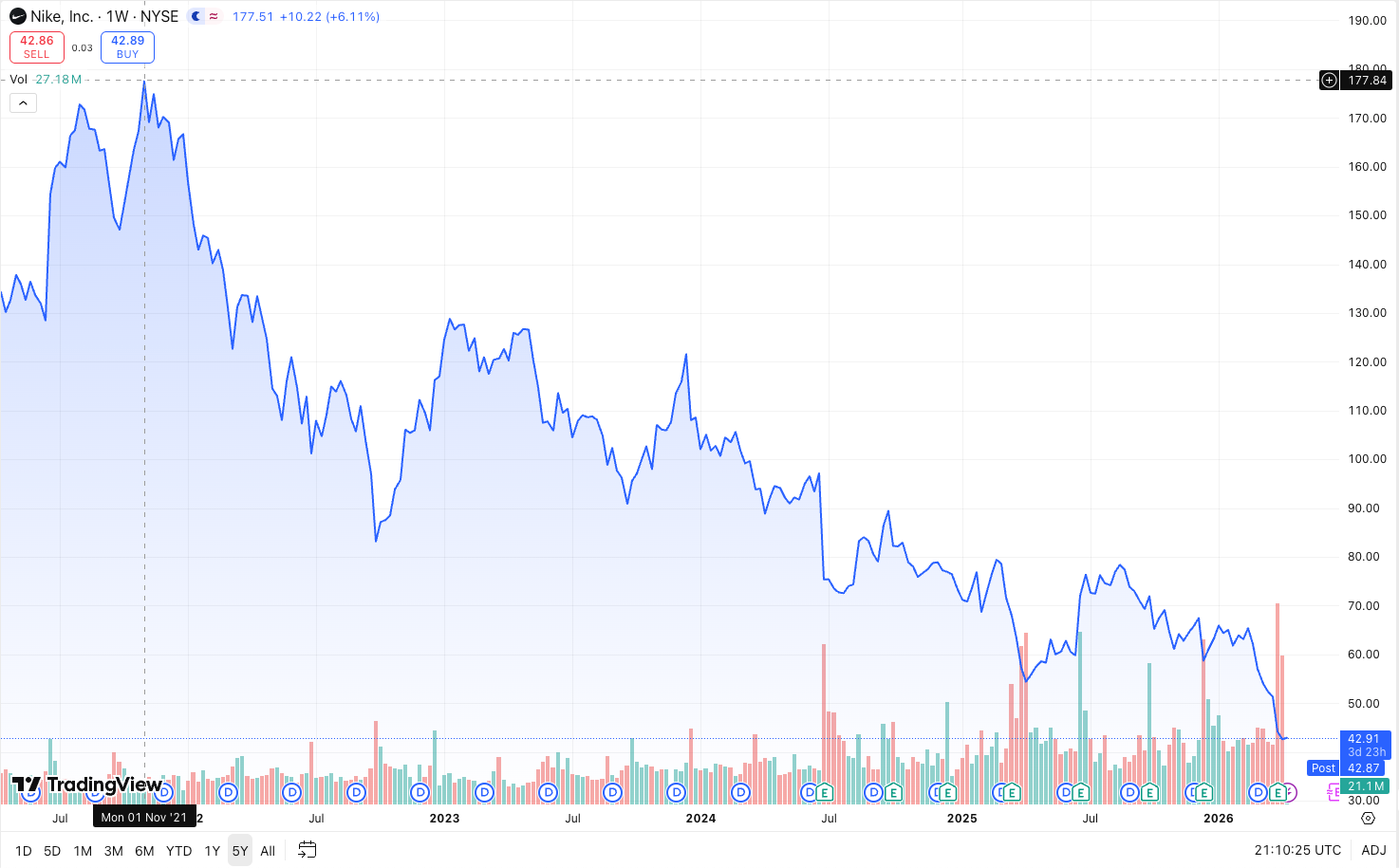

On April 1, 2026, Nike reported fiscal Q3 earnings that sent the stock down 15.5% in a single session. Revenue was flat at $11.3 billion. The company projected another 20% decline in China sales for the upcoming quarter and guided for a 2-4% revenue decline overall. JPMorgan cut its price target from $86 to $52 and downgraded the stock to neutral. Goldman Sachs and Bank of America followed with their own downgrades.

The CEO, Elliott Hill, a Nike veteran who came out of retirement to lead the turnaround, told employees he was “so tired” of the company’s struggles. The chief innovation officer left after less than a year. Johnson Fistel, a shareholder litigation firm, announced it was investigating potential claims on behalf of Nike investors.

Just last week, Piper Sandler downgraded Nike from Overweight to Neutral and cut its price target to $50. Analyst Anna Andreeva warned that the athleisure market is becoming saturated, that Nike’s shrinking Classics business has no clear replacement, and that the stock is “in penalty box” with no catalyst until an Investor Day sometime in the second half of this year. She set a bear case of $35 (another 15%+ decline from today’s prices).

This week, HSBC piled on, slashing its EBIT estimates for fiscal 2026 through 2028 by 35% and calling the turnaround a “show me” story with limited forward visibility.

Five major downgrades (JPMorgan, Goldman Sachs, Bank of America, Piper Sandler, HSBC), all within two weeks don’t signal a difference of opinion, they signal a collapse of consensus among institutions allocating Nike to client portfolios.

This is not a stock that’s quietly underperforming. This is a blue chip that’s been in freefall for the last 5 years.

The Roster That Should Be Enough

Here is what makes Nike’s decline so fascinating from an investment perspective. The athlete roster has never been stronger and it’s never mattered less.

Rory McIlroy just won back-to-back Masters titles wearing Nike apparel. He earned $4.5 million from a record $22.5 million purse. Scottie Scheffler, who finished second, is also a Nike athlete. LeBron James is still the face of Nike Basketball in his 22nd NBA season. Serena Williams remains a Nike ambassador. The U.S., Brazil, England, and France will all wear Nike kits at the 2026 FIFA World Cup this summer.

This is, by any reasonable measure, the most decorated athlete roster in the history of sports marketing. Tiger Woods. Michael Jordan. Cristiano Ronaldo. Rafael Nadal. The list goes on.

And the market does not care…not even a little.

That tells you something important about what drives stock prices. It’s not brand awareness or cultural relevance. It’s not even the quality of the product.

Stock prices are driven by:

margins,

revenue growth,

competitive positioning, and

the ability to convert attention into profit.

Nike is crushing the attention game but getting decimated in the business game.

Buffett Framework:

“It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” The question is whether Nike at $43 is a wonderful company at a wonderful price, or a formerly wonderful company at a trap price. The answer depends entirely on whether the moat, athlete endorsements, brand equity, is actually generating the economic returns it used to.

The Ad Tells the Whole Story

Go look at that Nike Masters ad again. It is genuinely excellent creative work. The speed of execution alone is remarkable. Nike had the ad locked, loaded, and deployed within minutes of McIlroy’s final putt. As always with their marketing production, the copy is sharp and the design is clean. It went viral instantly.

And that’s the entire problem distilled into a single social media post.

The marketing machine works perfectly. The brand engine is firing on all cylinders. Nike can still make you feel something. They can still own a cultural moment. Over 400,000 people have watched that ad in the days following his victory. Most companies would do anything for that kind of organic reach.

But no amount of brilliant marketing can fix a margin problem, a tariff problem, and a competitor problem all at the same time. The creative team is doing its job. The business is not doing its part. That disconnect is what a 76% decline looks like from the inside.

The Competitive Landscape Changed While Nike Was Looking at Its Phone

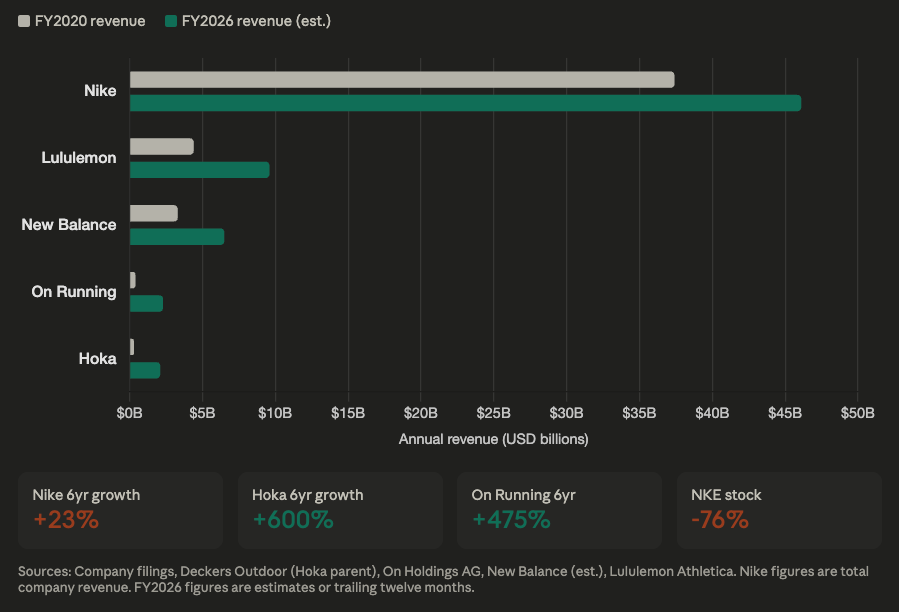

When I worked as a consultant at Nike between 2018 and 2020, primarily on brand strategy with some digital transformation overlap, the competitive set was manageable. Adidas was the main threat and their US campus was right across the bridge in Portland. Under Armour had faded. New Balance was a niche player.

That world does not exist anymore.

Hoka exploded from a niche running brand into a mainstream performance powerhouse. On Running has captured the premium athleisure consumer who used to default to Nike. Lululemon moved from yoga pants into running shoes and performance apparel. Vuori and Alo Yoga own the “lifestyle” segment that Nike’s Sportswear division used to dominate. Even New Balance has become a cultural force, driven by collaborations and a retro aesthetic that resonates with younger consumers.

The sneaker collectible market, which once served as a massive demand driver for Nike’s Jordan brand and Dunk franchise, has totally collapsed. Resale premiums have evaporated. The hype cycle that fueled billions in secondary market transactions has cooled dramatically. For a company that benefited enormously from artificial scarcity and drop culture, the normalization of the sneaker market is a structural headwind, not a cyclical one.

And then there are tariffs.

Nike manufactures roughly 50% of its footwear in Vietnam and another 25% in Indonesia and China. The current tariff environment is compressing margins on products that are already under pricing pressure from cheaper, trendier competitors.

The Fiduciary Question

A partner at financial advisory firm recently told me that Nike is in one of their client portfolios even thought it lost 75% of its value since they bought it. When I asked why they still held it, the response was: “Out of 50 stocks, we can’t all pick winners.”

That answer should concern anyone who pays an advisory fee.

A fiduciary obligation does not mean you have to be right about every position. It means you have to monitor your positions and act when the thesis changes. Nike’s thesis changed in 2022 when the direct-to-consumer pivot started faltering. It changed again in 2023 when competitive pressure became undeniable. It changed definitively in 2024 when the company reversed course on wholesale and admitted its strategy had failed.

At each of those inflection points, a fiduciary had the responsibility to evaluate whether the original investment thesis still held. Watching a position lose three quarters of its value and shrugging is not portfolio management; it’s inertia.

This article isn’t meant to be about Nike specifically. It’s about a broader pattern I see in wealth management where familiar names get held long past the point where the fundamentals justify the position.

Brand recognition is not a substitute for investment analysis, just like “hope” is not a strategy.

If your advisor is holding Nike because it’s a “great brand,” ask them to explain the margin trajectory, the competitive dynamics, and the China exposure. If they can’t, that’s a different kind of problem.

Buffett Framework:

“Should you find yourself in a chronically leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.” The fiduciary question isn’t whether Nike will eventually recover. It’s whether your capital should sit in a leaking boat while it tries.

One More Thing: The Masters Outbet the Super Bowl

Here’s a data point that caught my attention this week.

The 2026 Masters generated more betting volume on Kalshi than the Super Bowl did. Let that sink in. A four-day golf tournament, played by a field of fewer than 90 competitors in Augusta, Georgia, generated more prediction market activity than the single largest sporting event in American media.

That’s a signal about where sports attention and capital are flowing. Golf, driven by personalities like McIlroy and Scheffler and the gambling integration that has transformed how fans engage with the sport, is capturing a level of financial attention that was unimaginable even five years ago.

Nike sponsors the two golfers who finished first and second. They dominate the sport’s biggest moment. And the stock is at a decade low.

If that doesn’t crystallize the difference between cultural relevance and business performance, nothing will.

The Bottom Line

Nike’s brand is not broken. Its marketing is not broken. Its athlete roster is arguably the strongest in the company’s history. Rory McIlroy just joined Nicklaus, Faldo, and Tiger in one of golf’s most exclusive clubs, wearing a swoosh on his hat while he did it.

What’s broken is the business model that used to convert all of that brand equity into margin expansion and revenue growth. The competition caught up. The direct-to-consumer pivot stumbled. The sneaker hype cycle ended. China weakened. Tariffs compressed margins and the company is now guided by a CEO who is publicly exhausted by the scale of the turnaround.

For investors, the lesson is straightforward: brand power and business performance are not the same thing. A company can own the cultural moment and still lose 76% of its market value.

The ad was brilliant. The stock chart is brutal.

Both things can be true at the same time.

That’s the paradox worth sitting with.

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.