The Crypto Tax Checklist I Wish I Had in 2024

My favorite disclosure! I am not a tax advisor, CPA, or attorney. Nothing in this article constitutes tax advice. This is an educational overview of considerations I have encountered as a crypto holder and registered investment advisor. Consult a qualified tax professional for guidance specific to your situation. Seriously. This one matters.

******

I learned something about the tax code in 2021 that cost me $4,200.

Not because I was doing anything wrong but because I assumed I understood how losses worked. Short answer: I didn’t.

Here is what happened.

During the 2020 and 2021 cycle, I had some positions that went sideways. Significantly sideways. When I sat down to do my taxes, I figured the losses would offset my gains dollar for dollar. That seemed logical. That is how it should work, right?

Turns out that’s not how it works.

The IRS caps the amount of net capital losses you can deduct against ordinary income at $3,000 per year. If you have $30,000 in net losses, you do not get a $30,000 deduction. You get $3,000 this year, and the remaining $27,000 carries forward. At $3,000 per year, you are looking at nine years to fully realize those losses.

I was operating under the assumption that the losses were fully deductible. I was wrong, and it changed how much I owed. The $4,200 was the difference between what I expected and what my CPA told me I actually owed after applying the $3,000 cap. It was not a catastrophic number, but it was enough to make me sit down and build the checklist I am about to share with you.

Tax season is here. The new 1099-DA form is creating confusion. Deadlines are approaching. And if you are holding, trading, staking, or earning yield on digital assets, there are things you need to be thinking about right now.

This is not advice. This is the checklist I wish someone had handed me before I made assumptions that cost me money.

1. Understand What Triggers a Taxable Event

This seems basic, but it trips up more people than you would expect. Not every crypto transaction is taxable, but more of them are taxable than most people realize.

Taxable events include: selling crypto for fiat (USD, EUR, etc.), trading one cryptocurrency for another (yes, swapping ETH for SOL is a taxable event), using crypto to purchase goods or services, and receiving crypto as payment for work or services.

Events that are generally not taxable: buying crypto with fiat and holding it, transferring crypto between your own wallets, and gifting crypto (though the recipient may have tax implications later).

The one that catches people: trading one coin for another.

If you swap Bitcoin for Ethereum, the IRS treats that as selling Bitcoin and buying Ethereum. You owe tax on any gain from the Bitcoin sale, even though you never touched dollars. Plan accordingly.

2. The 1099-DA Is Here, and It’s Messy

This is the big change for the 2025 tax year.

For the first time, custodial brokers like Coinbase are required to report your crypto transaction proceeds to the IRS using the new Form 1099-DA. If you sold or traded crypto on Coinbase in 2025, you will receive one.

Here’s the problem though…For tax year 2025, Coinbase is only required to report gross proceeds. They are not required to report cost basis. That means your 1099-DA might show that you received $95,000 from selling Bitcoin, but it will not show that you paid $60,000 for it.

Without the cost basis, the IRS sees $95,000 in proceeds and assumes the entire amount is gain unless you correct it.

Don’t worry - It gets worse.

If you transferred crypto into Coinbase from another exchange or a hardware wallet, Coinbase has no way of knowing what you originally paid for it. Your cost basis will show as zero or unknown. One tax professional described it bluntly: Coinbase is sending forms to the IRS that are, by design, incomplete.

What to do: Do not rely on your 1099-DA to file your taxes. Track your own transactions. I personally use an Excel spreadsheet for every trade I make. I do not trade that much, which makes this manageable. I record the date, the asset, the amount, the price I paid, and the price I sold at. When tax season arrives, I hand the spreadsheet to my CPA and let them reconcile it against whatever forms the exchanges send.

If you have a higher volume of transactions, a dedicated crypto tax tool like Koinly can import your transaction history across exchanges and wallets and calculate your gains and losses. Koinly partnered with Coinbase this year specifically to help users navigate the 1099-DA confusion. That partnership exists because this problem is real and widespread.

The bottom line: your 1099-DA is a starting point, not a final answer. Treat it with appropriate skepticism and verify everything independently.

3. Find a CPA Who Actually Understands Crypto

This is arguably the most important item on this list.

A CPA who is unfamiliar with digital assets can cost you more in overpaid taxes and missed opportunities than their fee would have been.

I want to highlight two resources here because they are doing genuinely excellent work in this space.

Crypto Tax Girl (cryptotaxgirl.com) is a full-service crypto tax firm founded by Laura Walter, CPA. Her team specializes exclusively in crypto taxation and they are personally active in the space. They handle everything from simple buy-and-hold portfolios to complex DeFi activity, liquidity pools, staking, nodes, and cross-chain bridging. They carry a 4.8 rating on Trustpilot from 40 reviews, and the consistent theme in client feedback is that they find errors other CPAs missed. One client reported that Crypto Tax Girl discovered a mistake on previous returns that saved them over $50,000. They also offer a course if you prefer the DIY approach.

Koinly (koinly.io) is a crypto tax software platform that integrates with most major exchanges and wallets. It can generate tax reports compatible with TurboTax, H&R Block, and other filing software. For this tax season specifically, Koinly and Coinbase have partnered to help users fill in the cost basis gaps that the 1099-DA leaves open. If you have transactions across multiple platforms, Koinly can consolidate everything into one report.

Whether you use a specialized firm, software, or both, the key is having someone (or something) that understands the specific nuances of digital asset taxation.

A general-practice CPA who handles your W-2 and rental income may not know the difference between staking rewards and capital gains. That distinction matters.

(Quick Disclosure that I have ZERO affiliation with either of these firms)

4. The $3,000 Capital Loss Limitation (Learn from My Mistake)

This is the one that cost me $4,200, and I want to explain it clearly because the implications for how you manage your portfolio are significant.

If your net capital losses exceed your net capital gains in a given year, you can only deduct up to $3,000 of those excess losses against your ordinary income. The rest carries forward to future years, at $3,000 per year, indefinitely.

Here is where it gets strategic. If you have large unrealized losses sitting in your portfolio, the question is not just whether to realize them. The question is when and how much.

Consider this: If you have $50,000 in unrealized crypto losses, realizing them all at once gives you $3,000 in deductions this year and $47,000 in carryforward. But if you also have gains in other positions, you might be better off realizing enough losses to offset those specific gains, plus the $3,000 ordinary income deduction, and holding the remaining losses for a future year when you expect larger gains.

Also worth noting: the wash sale rule that applies to stocks, bonds, mutual funds, and ETFs does not currently apply to cryptocurrency. (yet)

That means you can sell a crypto position at a loss, immediately repurchase the same asset, and still claim the loss. This is called tax-loss harvesting, and it is one of the few structural advantages crypto holders have over traditional equity investors right now. Whether that regulatory gap persists is an open question, but for the 2025 tax year, it remains available.

The broader lesson: understand the mechanics before you assume how losses work. I assumed wrong, and it was an expensive education.

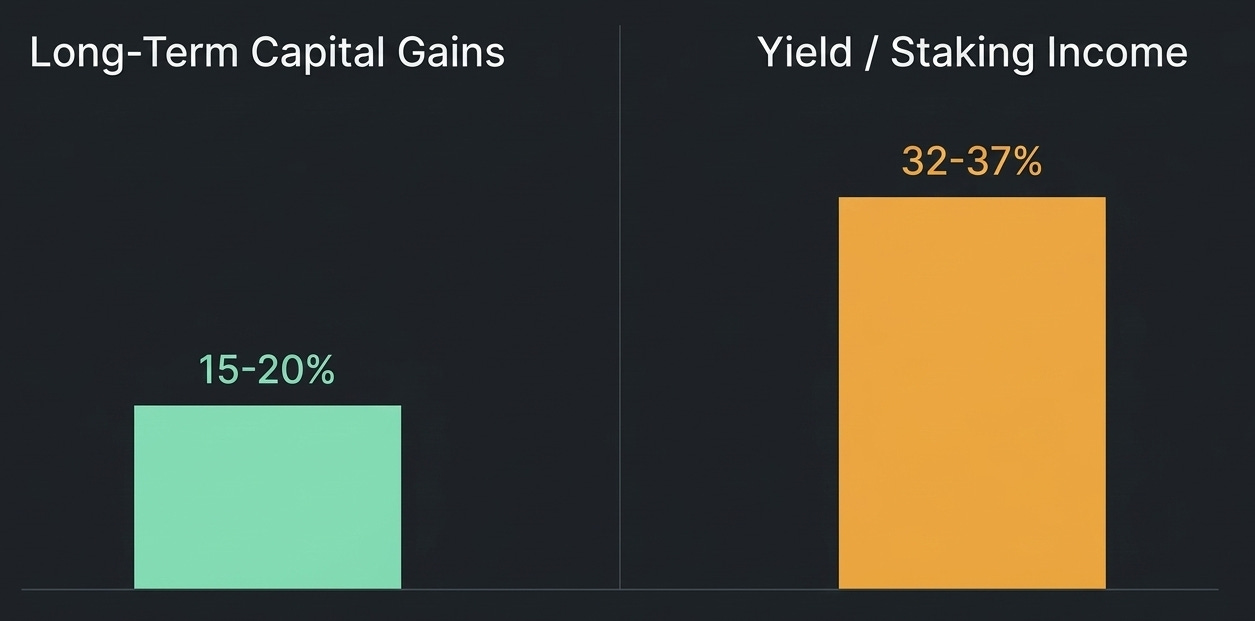

5. Income from Yield and Options Is Taxed Differently Than Capital Gains

This distinction catches a lot of crypto holders who have moved into more active strategies.

Capital gains (from buying and selling assets) are taxed at either short-term rates (same as your ordinary income if held less than a year) or long-term rates (0%, 15%, or 20% depending on your income bracket if held more than a year).

Income from yield (staking rewards, lending interest, liquidity pool fees) is generally treated as ordinary income, taxed at your marginal income tax rate at the time you receive it. The fair market value of the tokens at the moment they hit your wallet is what matters, not what they are worth when you eventually sell them.

Income from options activity (selling covered calls, earning premiums) is also typically taxed as ordinary income or short-term capital gains depending on the structure. The specifics vary based on whether the option is exercised, expires, or is closed out.

The practical implication: if you are earning yield or writing options on your crypto positions, those earnings are likely taxed at a higher rate than your long-term capital gains. Factor that into your strategy and your estimated tax liability.

6. If You Are Earning Yield or Options Income, You Probably Owe Quarterly Estimates

This is the one that sneaks up on people.

If you have income that is not subject to withholding (and crypto yield is not subject to withholding), the IRS expects you to pay estimated taxes quarterly.

The quarterly deadlines for the 2026 tax year are April 15, June 15, September 15, and January 15 of the following year. If you underpay by more than a certain threshold, you may owe a penalty on top of the tax itself.

If you earned meaningful yield or options income during 2025 and did not make quarterly estimated payments, talk to your CPA about whether you need to account for that in your filing. For 2026, if you are continuing to earn yield, set up a quarterly payment schedule now before the income accumulates and the estimate becomes guesswork.

The simplest approach: set aside 25-35% of your yield and options income as it arrives, keep it in a separate savings account, and pay the estimates on schedule. Do not spend yield before accounting for the tax liability. That is a mistake you only want to make once.

7. You Still Have Time to Contribute to a Roth IRA for 2025

This is a quick reminder, but an important one. You have until April 15, 2026 to make a Roth IRA contribution for the 2025 tax year. The maximum contribution is $7,000 if you are under 50, or $8,000 if you are 50 or older.

Income limits apply.

For single filers, your modified adjusted gross income must be below $150,000 for a full contribution (phase-out begins there and ends at $165,000).

For married filing jointly, the phase-out range is $236,000 to $246,000.

Why mention this in a crypto tax article? Because Roth IRA contributions grow tax-free. If you believe in the long-term appreciation of digital assets (or any asset class), putting contributions to work inside a tax-free wrapper is one of the most powerful tools available. Some self-directed IRA custodians allow crypto holdings within the Roth structure.

If you have not maxed out your 2025 Roth contribution, you have six weeks. Consider whether it makes sense for your situation.

8. Keep Records Like You Expect to Be Audited

I will end with the habit that underpins everything else on this list. Keep records. Detailed records. For every transaction.

The IRS is increasing its visibility into crypto transactions. The 1099-DA is just the beginning. The OECD’s Crypto-Asset Reporting Framework (CARF) is creating a global standard for cross-border reporting. Exchanges are sharing more data with tax authorities, not less. The era of crypto existing in a reporting gray area is ending.

What to track for every transaction: date, asset, quantity, price at time of transaction (both buy and sell), the exchange or wallet used, the type of transaction (purchase, sale, swap, yield, airdrop), and whether it was a short-term or long-term holding.

I do this in a simple Excel spreadsheet. I update it the day the transaction happens, not three months later when I am trying to remember details. If you prefer software, Koinly, CoinLedger, and several other tools can automate most of this by connecting to your exchange APIs.

The goal is not paranoia. The goal is that when your CPA asks for your records, you hand them a clean, organized file and the conversation is about strategy, not reconstruction.

The Broader Lesson

My $4,200 mistake was not really about the $3,000 capital loss cap. It was about assuming I understood something I had not taken the time to verify. In investing, assumptions are expensive. In taxes, they are expensive and avoidable.

Digital asset taxation is complex and still evolving. The rules are changing. The reporting requirements are expanding. The professionals who specialize in this space are becoming more important, not less.

Build your checklist. Find your CPA. Track your transactions. And do not assume the exchange is sending the right information to the IRS, because right now, by their own admission, they cannot.

— Matthew

X: @bit_finance_

Resources Mentioned in This Article

Crypto Tax Girl (cryptotaxgirl.com) - Full-service crypto tax firm, consultations, returns, and DIY course

Koinly (koinly.io) - Crypto tax software, integrates with Coinbase and 300+ exchanges

IRS Form 8949 - The form you will use to report your actual cost basis if your 1099-DA is incomplete

Roth IRA Deadline - April 15, 2026 for 2025 contributions ($7,000 under 50, $8,000 over 50)

The best investors I know got that way by reading widely and talking to the right people.

If BitFinance belongs in someone’s inbox, send it their way.

Referrals unlock free PDFs, paid access, and more.

oh! one last thing…if you want to dive deeper into how Buffett’s investing principles applies to digital assets, check out my book.

We took 1,300+ pages of wisdom from the Oracle of Omaha and condensed it into a snackable, easy-to-read guide for digital asset investors. Pick up your copy today!

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.