The Biggest Crypto Conference in America Had One Problem. Nobody Talked About Crypto.

The Digital Asset Summit is the biggest institutional crypto conference in the country. Three days at Javits Center in New York City. Blockworks puts it on every year, and the speaker list reads like a who’s who of people actually moving capital in this space.

I went so you didn’t have to; here are some highlights:

SEC Chairman Paul Atkins opened the conference.

BlackRock’s Global Head of Market Development talked tokenization.

Franklin Templeton and Ondo announced a partnership from the floor.

Visa revealed it’s joining the Canton Network as a Super Validator.

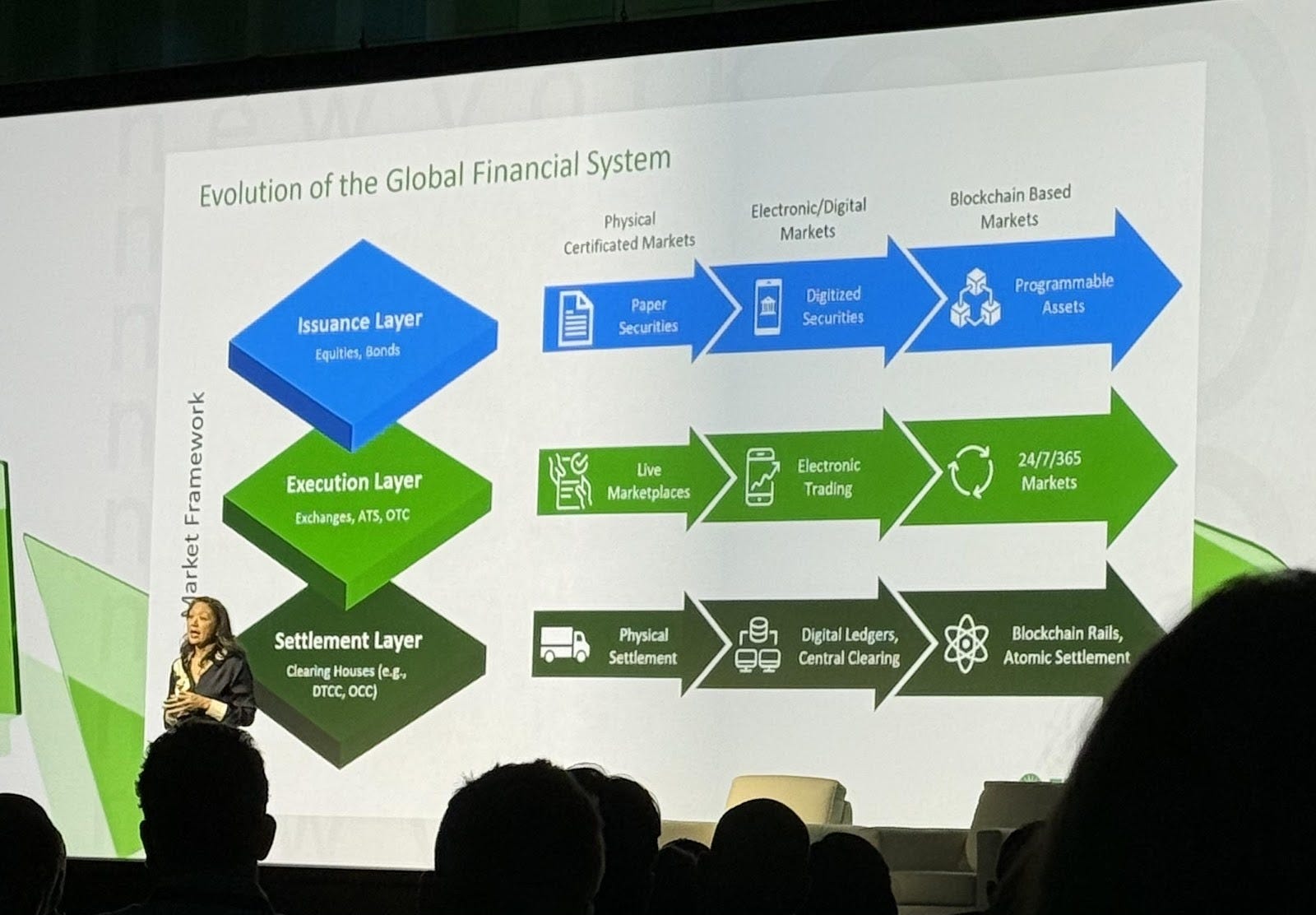

Fidelity walked through a full institutional infrastructure stack that made blockchain feel less like a technology bet and more like a plumbing upgrade.

Across 20+ intentional meetings with custodians, infrastructure providers, fund operators, and policy advocates, I heard exactly zero serious conversations about altcoins, memecoins, or retail speculation.

That’s not a criticism. It’s a signal.

Here are the five biggest takeaways.

1. The Clock Is Ticking on Regulatory Clarity

By the numbers:

The SEC published a token taxonomy last week distinguishing five categories of digital assets, four of which are not securities.

The Digital Asset Market Clarity Act passed the House in July 2025 (294-134) but remains stalled in the Senate.

GENIUS Act stablecoin implementation rules are due by July 18, 2026.

Industry sources estimate a 50-60% chance the Clarity Act passes before November 2026 midterms.

SEC Chairman Atkins opened the conference with what may be the most consequential speech the crypto industry has heard from a regulator. The SEC published a token taxonomy that draws clear lines between digital assets that are securities and those that aren’t. Five categories. Four of them fall outside the Commission’s jurisdiction. After years of enforcement-by-ambiguity, that’s a meaningful step.

But Atkins was careful to frame it as a foundation, not an endpoint. And that framing mattered, because the mood in the room wasn’t celebration. It was urgency.

The Clarity Act, which would finally resolve the SEC-CFTC jurisdictional turf war, passed the House last July with bipartisan support. It’s been stuck in the Senate ever since.

The sticking point? Stablecoin yield

Banks are lobbying hard to prevent stablecoin issuers and their affiliates from offering returns that could compete with traditional deposits. Senators Tillis and Alsobrooks reportedly struck a tentative compromise last week, but the bill still needs committee markups, reconciliation with the House version, and floor time.

The window is real but not guaranteed. Midterm elections in November could shift the balance of power in Congress. A new administration, or even a reshuffled committee, could bring a return to the kind of regulatory hostility the industry just escaped. Everyone I spoke with understood the stakes.

Buffett has always said that the best time to invest is when the rules are clear and the odds are in your favor. Right now, the rules are getting clearer. But the clock is running.

2. Tokenization Won the Narrative

By the numbers:

BlackRock’s Global Head of Market Development headlined a session called “Making Tokenization a Reality: Bringing Assets Onchain.”

Franklin Templeton and Ondo Finance announced a partnership during the conference to bring tokenized ETF exposure to blockchain users.

Ondo Global Markets reports $620 million in total value locked and $12 billion+ in trading volume across 60,000 users.

76% of institutional firms intend to invest in some form of tokenized assets by 2026 (EY-Parthenon).

If FutureProof Miami was the conference where I first noticed tokenization overtaking Bitcoin as the word generating the most curiosity among advisors, DAS was the conference where that shift became undeniable at the institutional level.

Tokenization wasn’t just a breakout session topic. It was essentially the main stage.

BlackRock’s Samara Cohen sat down with Blockworks co-founder Jason Yanowitz for a headline conversation about bringing assets onchain.

Not Bitcoin.

Not Ethereum.

Assets. (think equities, bonds, funds, real estate, all of it represented as programmable tokens on blockchain rails.)

Meanwhile, Franklin Templeton and Ondo Finance announced a partnership that landed during the conference itself.

Under the structure, Ondo will acquire shares of Franklin Templeton’s ETFs and issue blockchain-based tokens representing their economic exposure. The tokens don’t grant direct ownership of the underlying shares. Instead, they pass through returns, enabling those assets to be used as collateral or to interact with decentralized finance applications.

Said another way, this is a $1.7 trillion asset manager choosing blockchain as a distribution channel.

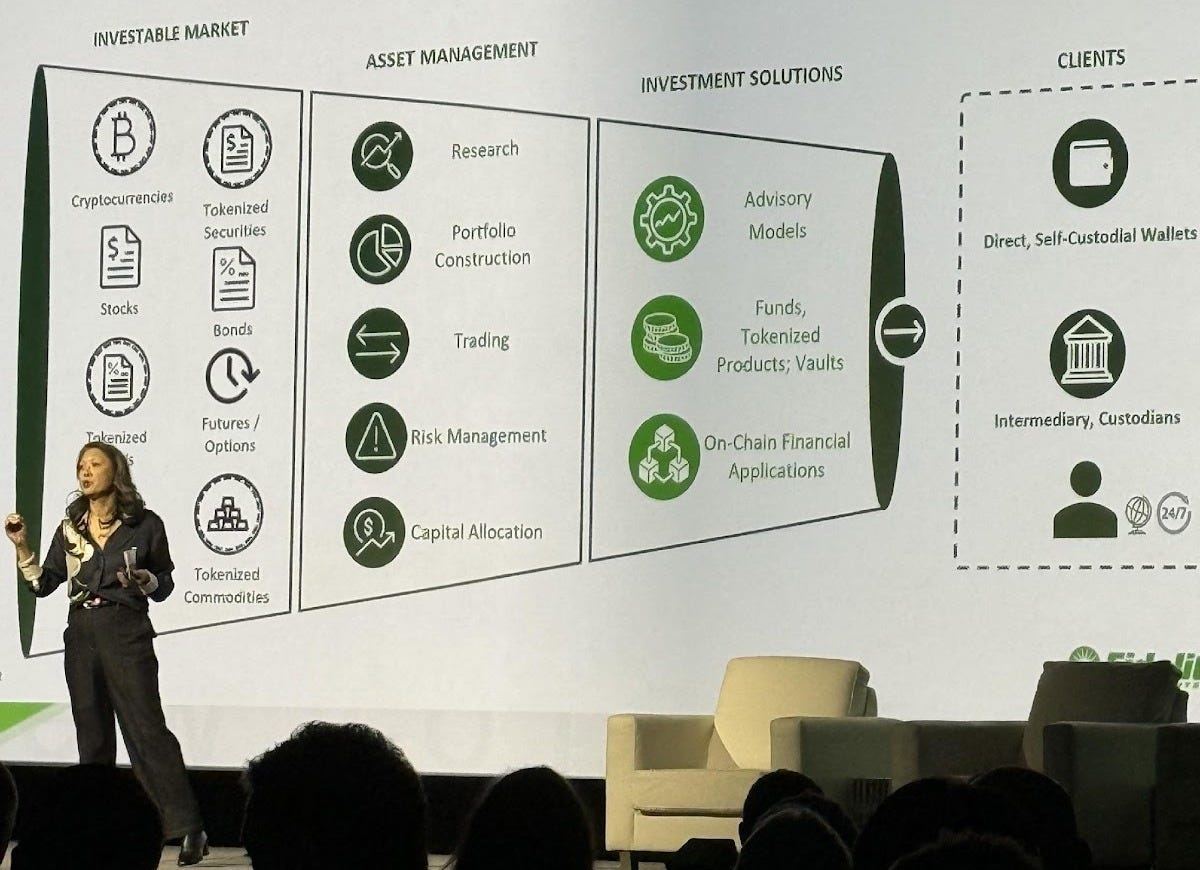

Fidelity reinforced the narrative with a presentation that walked through the full evolution of financial markets: from paper certificates to digitized securities to programmable assets. From live marketplaces to electronic trading to 24/7/365 markets. From physical settlement through central clearing to blockchain rails with atomic settlement. It was methodical, institutional, and entirely devoid of hype.

Munger used to say that the big money is not in the buying and the selling but in the waiting. The institutions represented at DAS aren’t waiting anymore. They’re building.

3. Stablecoins Are the Infrastructure Play

By the numbers:

Stablecoin market cap surged 49% in 2025, adding $102 billion to reach a record $311 billion (CoinGecko).

Visa’s stablecoin settlement volume reached a $3.5 billion annualized run rate as of November 2025.

84% of institutions are either utilizing or expressing interest in utilizing stablecoins (EY-Parthenon).

42% of middle market companies say they’ve discussed, tested, or used stablecoins (PYMNTS).

If tokenization was the narrative, stablecoins were the center of gravity.

Nearly every meaningful conversation I had circled back to stablecoins in some form: settlement infrastructure, institutional yield, treasury management, cross-border payments.

The biggest announcement came from Visa.

The payments giant revealed it’s joining the Canton Network as its first major Super Validator, bringing what it described as Visa-grade trust, governance, and operational rigor to privacy-preserving blockchain infrastructure. Canton is built specifically for institutional finance. It doesn’t use public stablecoins like USDC. Instead, regulated banks bring their own tokenized deposits onto the network for settlement. Think of it as the institutional plumbing layer that most retail investors will never see but that makes everything else possible.

This is a different conversation than the one happening in retail crypto. The stablecoin thesis at DAS wasn’t about yield farming or DeFi protocols. It was about replacing legacy settlement rails. Seven-day settlement windows instead of five. Atomic delivery-versus-payment instead of T+1 or T+2 clearing. Programmable treasury operations instead of manual reconciliation.

The GENIUS Act, signed into law last July, created a federal framework for payment stablecoins. Implementation rules are due by July 18 of this year. The banking industry is fighting to close what it sees as a yield loophole, while the crypto industry is fighting to preserve the ability to offer returns to stablecoin holders. That tension was everywhere at DAS.

But here’s what matters for allocators: stablecoins are no longer a crypto curiosity.

They’re becoming settlement infrastructure. Visa doesn’t join a blockchain network as a Super Validator because it thinks stablecoins are interesting. It does it because it thinks they’re inevitable.

4. Custody Is the New Arms Race

By the numbers:

BitGo expanded Canton Network support to CIP-56 token standard assets, including USDCx and cBTC, on the day of the conference.

Fidelity’s blockchain infrastructure slide stacked custody alongside tokenization, data oracles, and stablecoin integration as core institutional layers.

The DAS sponsor wall featured multiple custody and infrastructure providers: Komainu, Everstake, Fireblocks, and others.

If tokenization is where the narrative is moving and stablecoins are the settlement layer, custody is the boring but essential infrastructure that makes both of them possible. At DAS, custody was everywhere.

Walk the exhibit floor and the pattern was impossible to miss.

Komainu was pitching institutional digital asset custody and management.

Everstake was highlighting its validator infrastructure across industry standards.

Even BitGo, which wasn’t on the floor but made news the same day, announced expanded support for Canton Network’s CIP-56 token standard, covering both USDCx (Circle’s Canton-native stablecoin) and cBTC (wrapped Bitcoin for Canton’s settlement ecosystem).

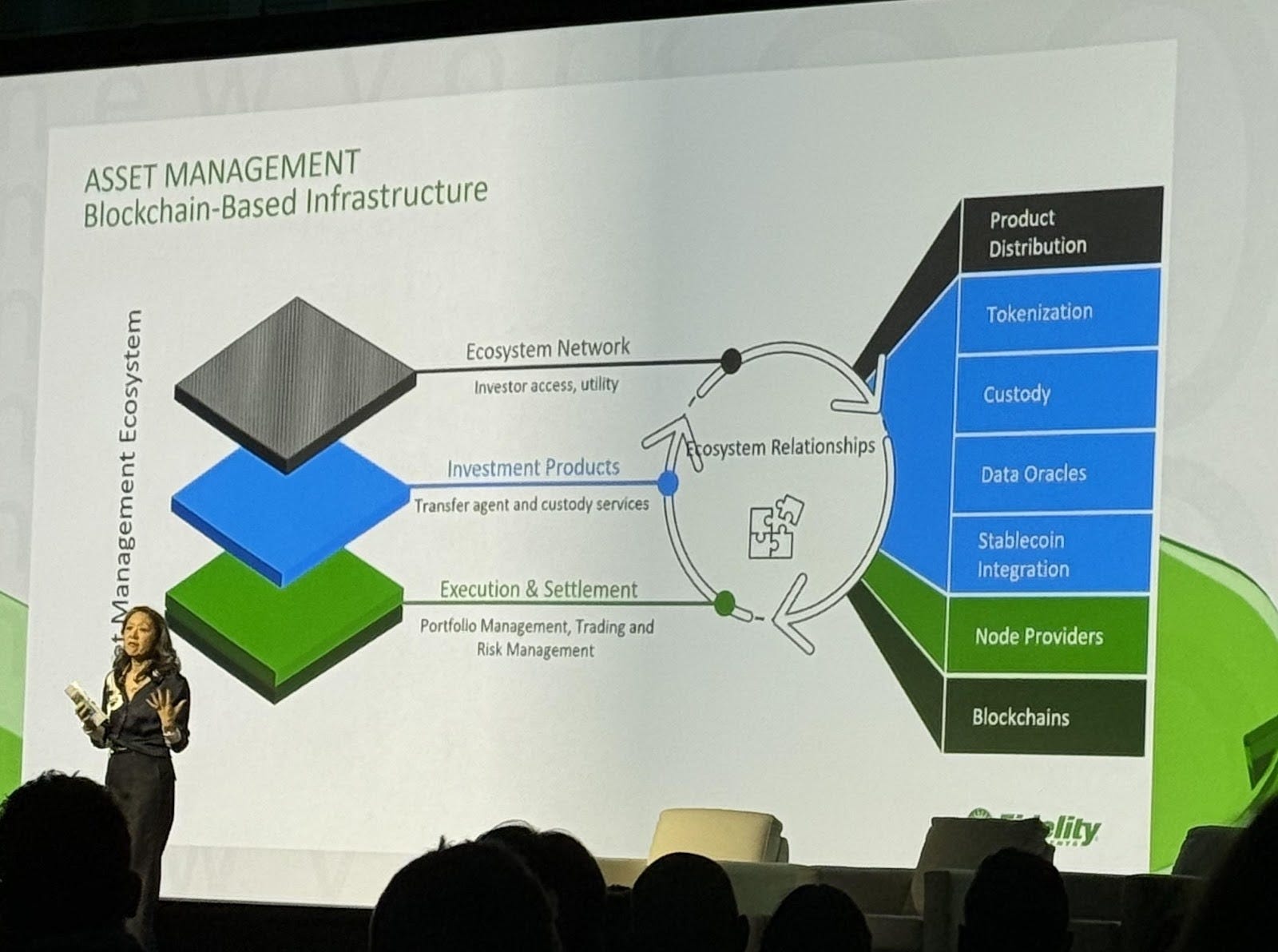

Fidelity’s presentation made the architecture explicit.

In one slide, they stacked out the full blockchain-based infrastructure layer: product distribution, tokenization, custody, data oracles, stablecoin integration, node providers, and the underlying blockchains themselves.

Custody wasn’t an afterthought. It was the central layer connecting investment products to the ecosystem network.

This is the part of the market that most retail investors and even most allocators never think about, but it’s where the real competitive dynamics are playing out. The question isn’t whether institutions will hold digital assets. It’s who they’ll trust to hold them. And that question is being answered right now, quietly, in partnership agreements and infrastructure builds that don’t make headlines.

Buffett has always said he likes businesses with wide moats. In digital assets, custody is becoming the moat.

5. The Dog That Didn’t Bark

By the numbers:

Bitcoin was the only individual digital asset that received sustained attention across main stage sessions.

Hedera and Stellar network had a muted precense.

57% of advisors report clients asking about crypto, but institutional conversations have narrowed to Bitcoin, stablecoins, and infrastructure (CoinShares, 2025).

In the Sherlock Holmes story Silver Blaze, the critical clue was the dog that didn’t bark. The same principle applied at DAS.

This was the biggest institutional crypto conference in the country. The sponsor banner included dozens of companies. The speaker list featured regulators, asset managers, and infrastructure builders from nearly every major financial institution. And across three days, I heard almost no serious institutional conversation about any specific digital asset other than Bitcoin.

No Ethereum roadmap debates.

No Solana versus Avalanche panel.

No one pitching the next layer-2 solution or making cases for specific altcoins.

The exhibit floor had protocol logos on sponsor banners, but the conversations happening in front of those banners were about infrastructure, not tokens.

That silence is the signal.

Institutional capital doesn’t follow narratives. It follows infrastructure and regulatory clarity.

The conference made clear that the institutional thesis has consolidated around three pillars:

Bitcoin as a store of value,

stablecoins as settlement and yield infrastructure, and

tokenization as the mechanism for bringing traditional assets onto blockchain rails.

Everything else, for now, is noise.

That doesn’t mean altcoins don’t have a future. It means the institutional conversation has moved past them. The money at DAS wasn’t asking which token to buy. It was asking which rails to build on, which custody provider to trust, and whether the regulatory window will stay open long enough to build something durable.

What I’m Watching

DAS confirmed several trends I’ve been tracking.

The institutional digital asset ecosystem is consolidating around infrastructure rather than speculation.

The regulatory window is real but time-limited.

And the companies that will capture the most value in the next cycle are the ones building the plumbing, not the ones promoting tokens.

For advisors, allocators, and retail investors the takeaway is straightforward.

The conversation has moved. If you’re still framing digital assets as a bet on token price appreciation, you’re having last cycle’s conversation. The institutional thesis is now about rails, settlement, custody, and regulatory positioning.

Like what you’re seeing? Go ahead and subscribe below if you haven’t already.

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.