The Most Important Derivative Crypto Ever Built

Ten years ago (yesterday), an obscure exchange called BitMEX published the design for a financial contract that wasn’t supposed to work.

No expiration date.

No settlement.

No precedent in 200 years of derivatives history.

The Nobel-winning economist Robert Shiller had floated the theoretical idea in the 1990s, but nobody had built one. On May 13, 2016, Arthur Hayes and the BitMEX team shipped the first perpetual futures contract.

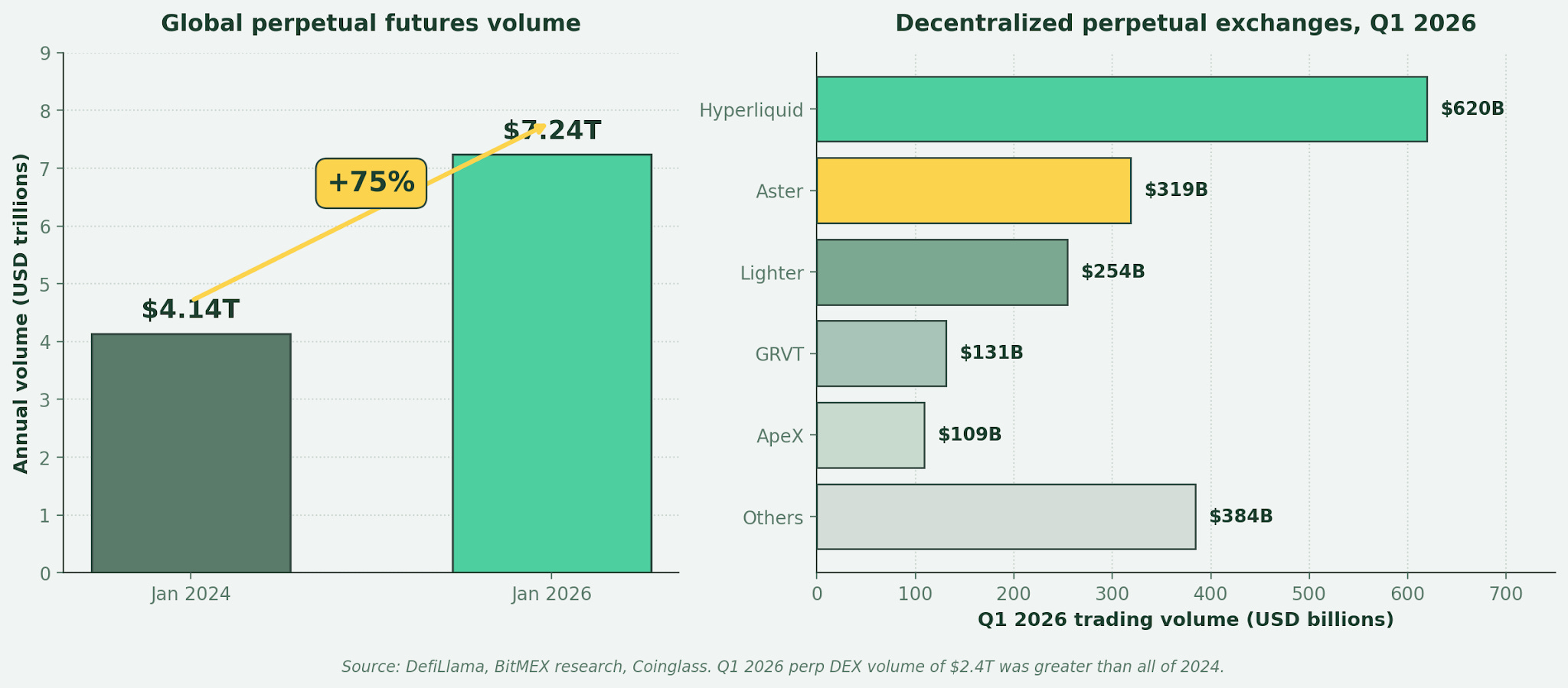

A decade later, it has become one of the most-traded financial instruments on the planet. The global perpetual futures market hit $7.24 trillion in January 2026, up from $4.14 trillion two years earlier. Decentralized exchanges alone processed roughly $2.4 trillion in Q1 of this year.

Most people I talk to have heard the term and have no idea what it actually means. Worth fixing. Here’s the primer I wish I had when I first started reading about Hyperliquid, Aster, and Euphoria.

BUFFETT FRAMEWORK QUESTION

“Do I understand this instrument well enough to use it intelligently, or stay away from it intelligently?” For perpetuals, most retail investors can’t answer either way. That’s a gap worth closing.

Start with a regular future

Forget crypto for a second.

A “future” is a contract that says:

I agree to buy something at a fixed price on a fixed date.

If the price goes up, I profit because I locked in a lower price than the market.

If the price goes down, I lose because I locked in a higher price than the market.

Buffett has used this exact structure for decades when Berkshire’s railroads and utilities lock in commodity exposure. Other analogies might include:

A corn farmer sells corn forward in spring to lock in his fall price.

An airline buys jet fuel forward to know what it will pay in six months.

CME crude oil or soybean contracts on the trading floor in Chicago.

Same structure, different underlying, but two important features matter here.

The contract expires.

Settlement happens at expiration.

If you want to keep your exposure beyond expiration, you roll the position into the next contract, which costs money in spread and creates tracking error against the underlying.

That cycle has worked fine for 200 years because traditional markets close.

Why this structure breaks in crypto

Bitcoin doesn’t close. It trades at the same intensity at 3am on a Sunday as it does at 10am on a Tuesday. A quarterly contract that settles on a Friday afternoon is awkward for an asset class that never sleeps. The rollover friction adds up fast for anyone who actually wants leveraged exposure for months at a time.

That was BitMEX’s problem in 2016.

no stopProfessional traders wanted leveraged Bitcoin exposure without rolling a quarterly contract every three months. The obvious solution was a contract that just keeps going. The non-obvious problem was that if the contract never expires, nothing forces its price to converge with the spot market. Without convergence, you have two prices for the same asset, and arbitrageurs can’t reliably close the gap.

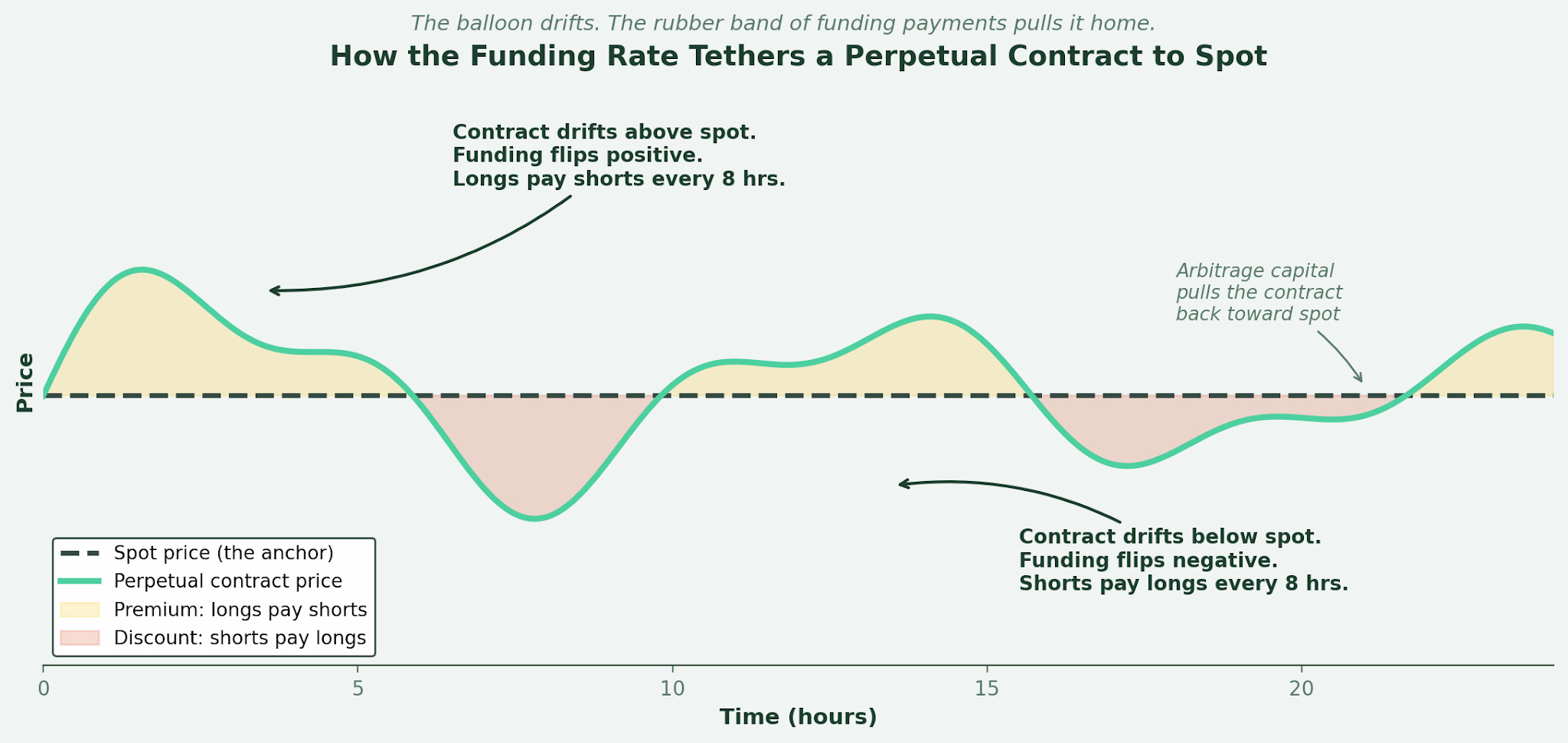

How to think about the “funding rate”

Here’s the metaphor that does most of the work.

Think of a perpetual contract as a dog on a leash.

The spot price is the owner.

The funding rate is the leash.

The dog can wander left or right, but every tug brings it back to the owner’s side.

As a finance nerd, I find the mechanism quite elegant.

Every eight hours, longs and shorts swap a small payment. The size and direction depend on the gap between the contract price and the spot price.

When the perpetual trades above spot, longs pay shorts. That payment makes it expensive to stay long and profitable to short, which pulls the contract price back down. When the perpetual trades below spot, the flow reverses. Shorts pay longs, the cost of being short rises, and the contract gets pulled back up.

The doggo can drift but it can’t escape (hopefully!). The further it tries to wander, the harder the owners pulls it back in line.

This single design choice is the entire innovation.

It replaces the convergence-by-expiration mechanic that has anchored futures markets since the 1800s with a continuous, market-driven payment system. Arbitrageurs do the heavy lifting. When the perpetual drifts above spot, sophisticated traders buy spot, short the perpetual, and collect the funding rate as a yield. That trade is mechanical and capital efficient. It’s also what Ethena built a $5 billion synthetic dollar around on Ethereum.

BitMEX’s own data shows extreme funding rates have dropped 90% since 2016 as more arbitrage capital has shown up. The market is doing what markets do when a mechanism works.

Smart money has filled the gaps, and the contract has become more boring and more reliable in the process.

What perpetuals actually let you do

Four things, and they’re the reasons the product spread:

24/7 markets matched to the underlying asset, with no closing bell and no overnight gap risk for assets that trade continuously.

No rollover. A position opened today can stay open for years without paying friction every quarter.

High capital efficiency. Leverage on most venues runs 10x to 100x. Some go to 1000x. That’s both the appeal and the destruction mechanism, depending on who’s using it.

Synthetic exposure to almost anything. If you have a reliable price feed, you can build a perpetual on it. Bitcoin, oil, gold, the S&P 500, a tokenized treasury bill, a basket of memecoins. The collateral and the underlying don’t need to live on the same chain or in the same asset class.

The business model behind perpetual exchanges

Perpetual exchanges make money the same way every other exchange does. Maker-taker fees, typically 0.01% on the passive side and 0.035% on the aggressive side.

The volume is what makes the math work.

Hyperliquid, built on its own Layer 1 blockchain, is currently the largest decentralized perpetual exchange in the world. Roughly 44% of perp DEX volume runs through it, with more than 70% of open interest. The protocol generates a $640M annualized fee run rate, of which 97% gets used to buy back HYPE tokens on the open market every day. Industrial-scale buy-and-burn tied directly to a real, measurable business.

Aster has carved out share with a different bet: aggressive incentives, multi-chain access, and a retail-friendly interface that feels closer to Binance than to a DeFi protocol. Euphoria, an early-stage MegaETH project that raised $7.5M from over 100 investors last year, is doing for crypto derivatives what Robinhood did for stock options. Mobile-first, tap-to-trade, designed for the user who doesn’t know what a maker-taker fee is and doesn’t want to learn.

Three different bets on who the next billion derivatives users actually are. The shared thesis is that the perpetual contract is too useful to stay in a niche, and the venue that wins the user experience battle captures a real business.

How sophisticated traders use perpetuals for alpha

This is the part most retail readers underestimate. Perpetuals aren’t only a leverage tool. They’re a yield instrument for anyone who understands the funding rate.

The cleanest example is the cash-and-carry trade. Buy spot Bitcoin, short the perpetual at the same size. When funding is positive, longs are paying you to hold a delta-neutral position. You collect a yield that’s mechanical, not directional. Ethena built an entire $5B+ synthetic dollar around exactly this mechanic.

Hedge funds run more complex versions. Funding rate arbitrage across venues, basis trading between perpetuals and dated futures, and delta-neutral yield strategies that use perpetuals to hedge directional exposure on yield-bearing collateral. Most of it looks boring on paper - which is kinda the point.

The takeaway is that “yield” in crypto often turns out to be a sophisticated trader understanding the plumbing well enough to harvest mechanical spreads that exist because the market is still pricing in maturation.

The risks worth saying out loud

Three things will hurt you in perpetual markets:

Liquidation. Leverage compounds in both directions. At 50x, a 2% adverse move wipes your position. Cascading liquidations are a feature of these markets, not a bug.

Funding rate flips. If funding moves against you and stays there, you bleed continuously even when your directional thesis is right.

Counterparty and oracle risk. On a centralized exchange, you carry the exchange itself (see FTX). On a DEX, you carry smart contract integrity and oracle reliability. Both are real.

Most retail traders who touch high-leverage perpetuals lose money. The instrument is brilliant. The way it’s typically used by retail is not. That distinction is worth keeping straight.

BUFFETT FRAMEWORK QUESTION

“Would I be comfortable explaining this trade to someone who has to live on what I make from it?” If the answer is no, the position is too big or the strategy is too complex.

What the next ten years might look like

Perpetuals have stopped being a crypto-only product.

Hyperliquid now offers perpetuals on oil, gold, silver, and the S&P 500. During the Iran conflict, crude oil perps cleared $1.7 billion in daily volume on a decentralized exchange that nobody at the CME would have given the time of day three years ago.

The S&P 500 perpetual cleared $100 million on its first day.

Combine perpetuals with tokenization and you get something more interesting than either alone. A perpetual on a tokenized treasury bill, a tokenized stock, an emerging-market currency, or a real-world asset that doesn’t usually trade after hours. The CME’s hours and the NYSE’s closing bell stop being binding constraints on synthetic exposure to any asset on earth.

That’s why TradFi keeps quietly investing in this space.

JPMorgan published research on Hyperliquid’s commodity perps last quarter.

Grayscale, Bitwise, and VanEck have all filed for spot HYPE ETFs.

CFTC opened formal consultations on perpetual futures 24/7 derivatives trading.

None of that happens unless serious institutions believe the instrument has legs.

The perpetual futures contract was invented to solve a narrow problem for a niche group of crypto traders in 2016. Ten years later it has become one of the largest financial markets on the planet, and the design choice that made it work is starting to reshape how derivatives function across asset classes.

You don’t have to trade perpetuals to benefit from understanding them, the same way you don’t have to short stocks to understand how short selling shapes price discovery. The financial innovations that matter usually start small and look like toys until they don’t. This one stopped looking like a toy a while ago.

Happy 10th birthday to the forever contract.🥳

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.

Sources

BitMEX, “The Evolution of Funding Rates: 9 Years of BitMEX’s XBTUSD Funding Rate Analysis,” Q2 2025 Derivatives Report.

DefiLlama Perp DEX Volume Rankings, Q1 2026 data.

Datawallet, “Crypto Perpetual Futures Statistics & Trends in 2026,” April 2026.

DL News, “Aster and Hyperliquid drive $2tn volume record as perp DEX competition heats up,” September 2025.

Yellow.com, “Hyperliquid Hits 44% Of All Perp DEX Volume,” March 2026.

The Block, “MegaETH-based crypto derivatives trading app Euphoria raises $7.5 million in seed funding,” August 2025.

Galaxy Research, “The Investable Universe 2.0,” August 2025.