The Company That Tokenized Itself

It’s 2032.

Your brokerage account is a wallet.

Your index fund settles in four seconds on a Saturday morning.

Your dividends stream into your account continuously instead of arriving 4x/ year

The private credit fund that used to require a $5 million minimum and a fax machine now trades in $100 pieces, and when you sell, the money arrives before your coffee cools.

Every piece of that future needs something unglamorous underneath it: a regulated company keeping the official record of who owns what.

Somebody has to be the scorekeeper.

Last Thursday, the leading candidate for that job went public.

Brief PSA: Why This Matters to You

In case you haven’t been reading my earlier letters on this (I covered the landscape in Tokenization’s Missing Buyers), tokenization comes down to 3 core ideas:

A better ownership record. Take something you can own, a fund share, a Treasury bill, a slice of a building, and record who owns it on a blockchain instead of in a private database. Same asset, better ledger.

The better ledger changes the experience. Trades settle in seconds instead of days, markets don’t close on weekends, and ownership can split into pieces as small as you like.

Small pieces open locked doors. Investments that used to demand millions and a stack of paperwork, like private credit and private equity funds, can be issued in $100 slices to anyone the compliance software approves.

That last point is the one to watch for your own portfolio.

Individual investors have been locked out of private markets for generations, and that’s tens of trillions of dollars across private equity, credit, real estate, and infrastructure, where a large share of institutional wealth compounding happens.

If even a few percent of it migrates on-chain, the pipes carrying it will matter as much as the assets flowing through them, and pipes are exactly what Securitize sells.

The Dog Food Moment

Securitize listed on the New York Stock Exchange under the ticker SECZ, raising roughly $400 million through a merger with Cantor Equity Partners II at a valuation around $1.25 billion.

Then it did something no public company had done before: on the same day its shares began trading, it issued tokenized versions of that same common stock on Solana and Avalanche.

By the close, investors held roughly $295 million in tokenized SECZ equity.

Day one of tokenized SECZ against Wall Street’s forecasts for the category. The gap is either the opportunity or the problem, depending on your read.

These aren’t synthetic wrappers or offshore IOUs. The tokenized shares carry the same voting rights and dividend entitlements as the exchange-traded stock, administered by the company’s own regulated transfer agent.

There’s an old expression in software: eat your own dog food. Securitize asked the market to believe tokenized equity is real, then converted a quarter billion dollars of its own cap table to prove it.

The company that builds tokenization rails just put itself on the rails.

That’s the story.

Now let’s open the hood the way a value investor reads any newly public company, and keep the checklist, because it works on the next debut too:

what does the business sell,

where does the revenue come from,

what do the bulls and bears each need to believe, and

how do the scenarios weigh out.

A note on method first: SECZ has been trading for a handful of sessions, and early SPAC price action is noise rather than signal. Small floats swing hard while the market decides what multiple to assign. We don’t judge a two-week-old company by its chart, so everything below is about the business fundamentals.

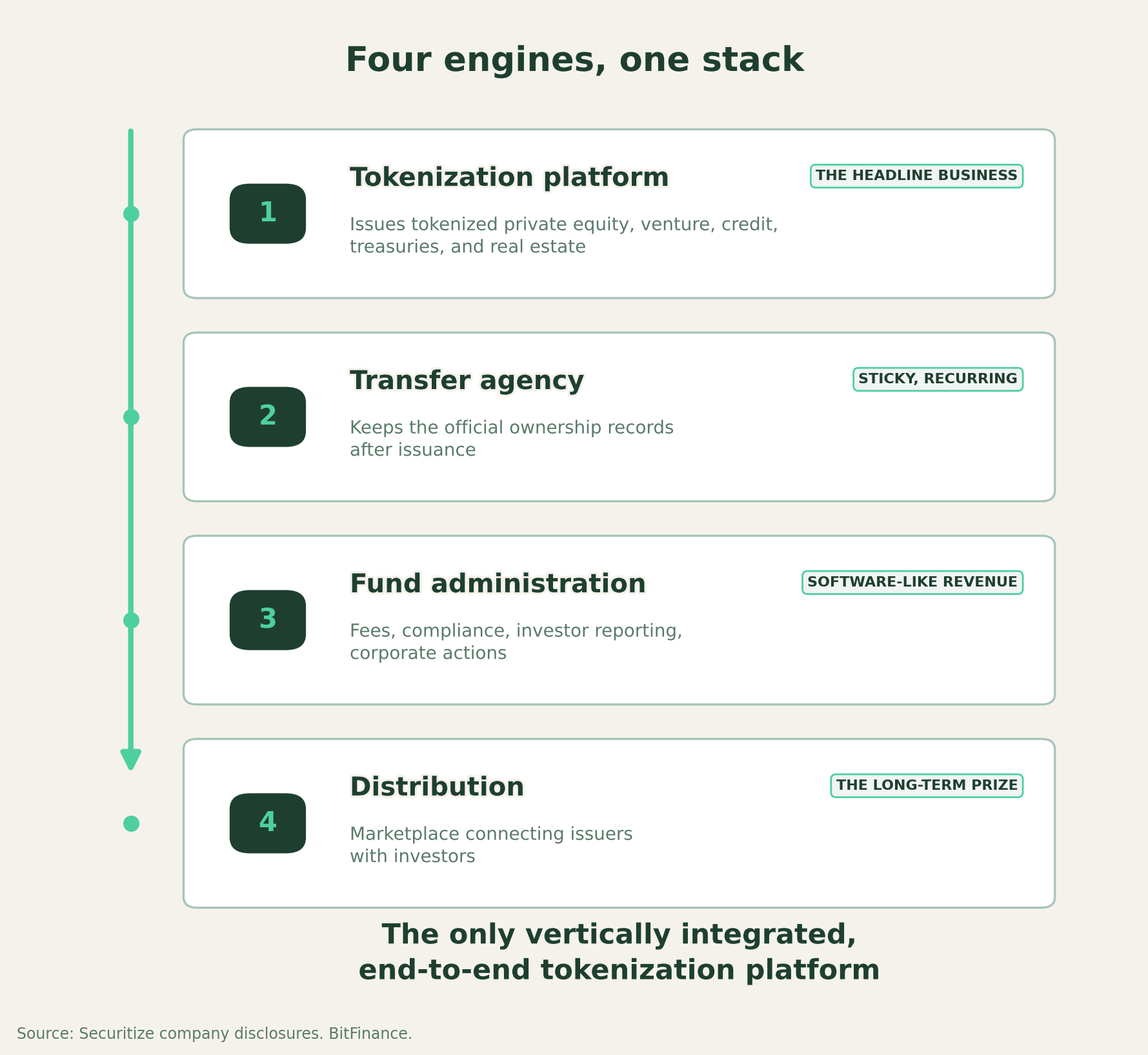

What Securitize Sells: 4 Businesses in One

The first thing to understand is that Securitize isn’t really a crypto company. It’s capital markets infrastructure that happens to use blockchain as its database. Four engines drive it:

1. The tokenization platform. The headline business: issuing tokenized private equity, venture funds, credit funds, treasuries, and real estate. Think of it as the Stripe of tokenized securities, the plumbing other firms build on.

2. The transfer agency. The underrated one. Being the transfer agent means Securitize stays involved after issuance, maintaining the official ownership records. The revenue recurs, the switching costs are high, and the relationships hold for the life of the fund.

3. Fund administration. One of the fastest growing pieces: administration fees, compliance, investor reporting, corporate actions. This looks far more like recurring software revenue than crypto trading revenue.

4. Distribution. A marketplace connecting issuers with investors. If private credit, private equity, and alternative assets all trade digitally one day, this could become the most valuable piece of all.

Notice what’s missing from that list: any dependence on crypto prices going up. That’s the point.

Straight Facts & Figures

The most recent quarter was the strongest in company history:

Revenue: $19.5 million, up 39% year over year, roughly $78 million annualized.

Assets under administration: $3.4 billion, with $1.9 billion in transaction volume.

Adjusted EBITDA: positive, at roughly $0.8 million.

Net income: negative $7.9 million; that number deserves context rather than alarm.

The losses aren’t a sign of a failing core business. They’re deliberate spending on engineering, compliance, institutional sales, and the costs of going public, while management keeps the company slightly above water on an adjusted basis. You can argue with the strategy, but it’s a choice, not a symptom.

The more important detail is where the revenue comes from.

It’s increasingly earned by servicing assets rather than riding speculation. The difference matters enormously: “crypto went up, therefore revenue increased” is a business you rent. “Assets keep existing, therefore we keep earning fees” is a business you can own.

Fee income from assets that keep existing is the closest thing crypto has to Buffett-grade revenue.

What the Bulls See 🐂

BlackRock validation. The success of tokenized funds like BlackRock’s BUIDL transformed institutional credibility for the whole category, and Securitize is one of the primary infrastructure providers behind it. Apollo, KKR, Hamilton Lane, and VanEck issue through the same rails. When the most conservative money on Earth picks a vendor, that’s due diligence you get to borrow.

Distribution deals with the incumbents. Intercontinental Exchange, the NYSE’s parent, partnered with Securitize in March to build tokenized equity infrastructure. Computershare, transfer agent to 58% of the S&P 500, signed on in April. The scorekeepers of the old system are wiring themselves into the new one, through this company.

A war chest. Roughly $400 million raised, earmarked for acquisitions to expand the platform.

An enormous addressable market. Global private markets, spanning private equity, credit, real estate, and infrastructure, run to tens of trillions of dollars. If even a few percent migrate on-chain, the market Securitize services expands dramatically. Citi projects tokenized assets could reach $5.5 trillion by 2030.

What the Bears See 🐻

A fair examination requires the other side of the ledger, and the concerns here are real:

Adoption could be slower than everyone thinks. This is the big one. Everybody agrees tokenization is useful, but few institutions want to rebuild their workflows. Banks move slowly, asset managers move slowly, law firms move slower still. Infrastructure adoption almost always takes longer than the conference panels promise.

The value chain isn’t settled. The competitor list keeps growing: Franklin Templeton, Figure, Tokeny, Centrifuge, Fireblocks, plus the uncomfortable fact that clients like BlackRock and Apollo could build competing capabilities themselves. Some want issuance, some want custody, some want settlement. Nobody knows yet where the profits pool.

Margins haven’t followed revenue. Growth is impressive, but expenses are rising nearly as fast. At some point public investors demand operating leverage, and if it doesn’t show up, the multiple compresses.

Regulatory churn. More regulation is good for a compliance-first company. Constantly changing regulation is not, since every new jurisdiction adds cost.

The valuation asks for the future. At roughly $78 million in annualized revenue against a $1.25 billion market cap, you’re paying around 16 times forward revenue. Infrastructure companies often trade on future network effects rather than present earnings, but the question is stark: does revenue become $80 million or $800 million? The multiple only works in one of those worlds.

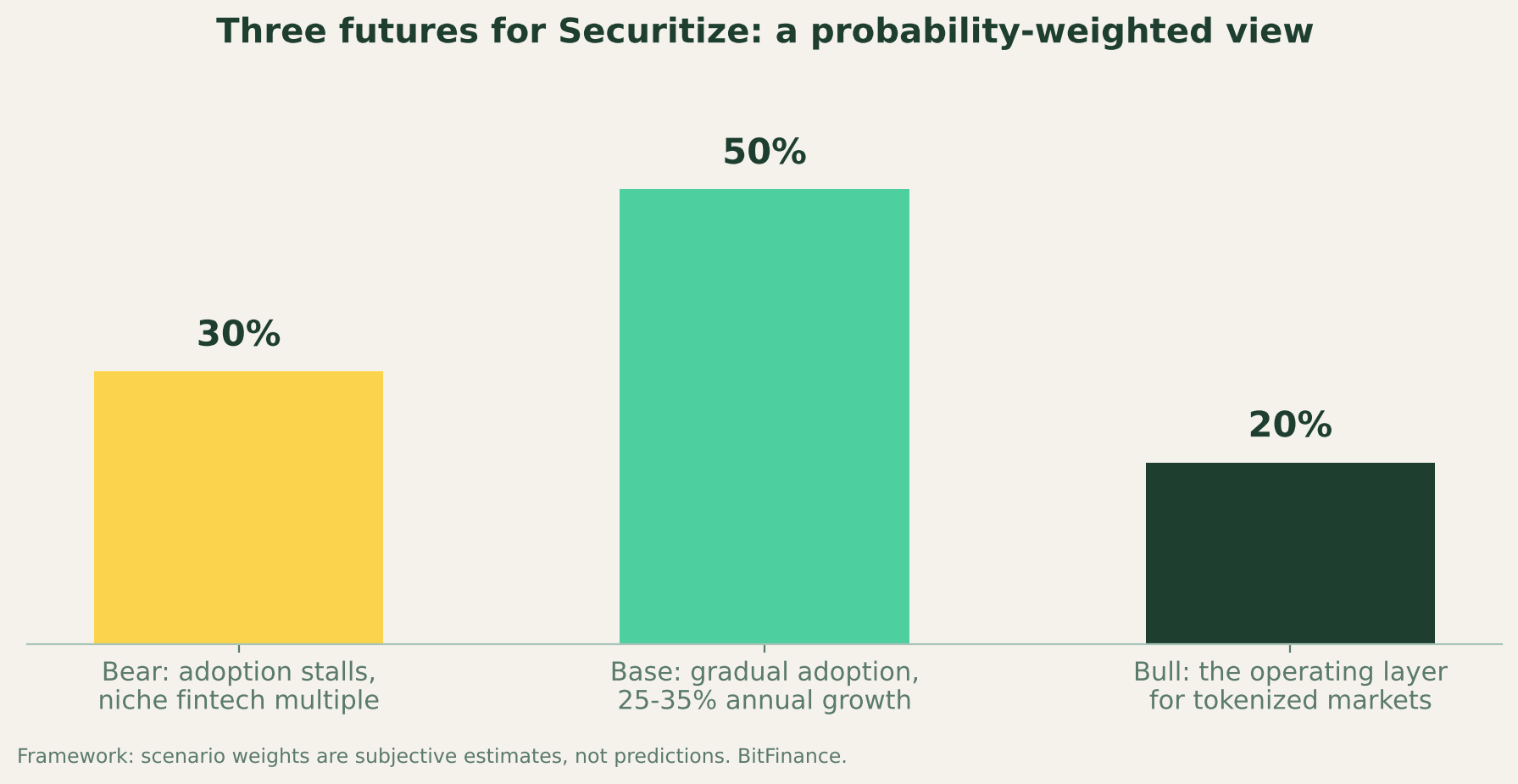

3 Futures

Rather than a price target, here’s how I’d frame it to an investment committee, expressed as scenarios with rough weights:

Bear (30%) Adoption stalls. Revenue growth slows into the teens, margins stay weak, and SECZ trades like a niche fintech servicing alternative funds at a materially lower multiple.

Base (50%) Tokenization becomes mainstream gradually: private credit first, treasuries second, institutional funds third, real estate later, public equities last. Securitize compounds revenue 25 to 35% annually, reaches sustained profitability, and settles in as durable infrastructure. It wouldn’t be explosive, but it would be very good.

Bull (20%) Securitize becomes the dominant operating layer for tokenized securities, the Bloomberg Terminal of the category, with every issuer, custodian, transfer, and compliance event flowing through its rails. In that world, today’s valuation eventually looks inexpensive.

A probability-weighted way to hold the thesis. The base case carries the weight, and the base case is patience.

Where the Market May Be Wrong…

The market keeps calling this business “tokenization,” and I think that label undersells it.

The real product is capital markets operating software: programmable ownership, instant settlement, automated compliance, lower operational costs, broader investor access. Blockchain is merely the database underneath.

Through that lens, Securitize isn’t competing with Coinbase for crypto traders, but with legacy transfer agents, fund administrators, and DTCC-era middleware for the operating budget of global capital markets.

One of those markets is cyclical and crowded. The other is enormous, sleepy, and running on decades-old plumbing.

I wrote earlier this year that tokenization has a buyer problem: rails without riders.

That thesis stands, and SECZ is now the public scoreboard for it. Two separate bets are being resolved here, and it pays to keep them separate. Tokenization almost certainly wins over the long run, because it genuinely improves settlement, compliance, and cost for private markets. Whether Securitize is the primary winner is the harder question, and it turns on execution, high-margin recurring revenue, and holding off incumbents who move slowly but arrive with scale.

The candid close: this is a young public company at a demanding valuation in a market that hasn’t fully arrived. It’s also the only pure-play claim on a category that BlackRock, the NYSE’s parent, and the transfer agent for most of the S&P 500 are all betting on with real money.

Starting next quarter, the debate finally runs on audited numbers instead of projections. For a sector that’s lived on promises, that alone is awesome progress to see.

Quick Shout Out: To all my friends and colleagues currently working under the Securitize banner - keep up the awesome work! Excited to see where this adventure goes and for what y’all are continuing to build. 👊🏼

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.

Sources

CoinDesk, “Securitize heads to NYSE debut after investors approve SPAC merger; CEPT gains 20%,” June 29, 2026.

CoinDesk, “Securitize (SECZ) takes $295M of its own tokenized stock to Solana, Avalanche amid NYSE debut,” July 2, 2026.

CoinDesk, “Securitize eyes acquisitions with $400 million war chest after going public, CEO says,” July 2026.

Securitize quarterly financial disclosures: revenue, assets under administration, adjusted EBITDA, and net income figures.

Securitize company announcements: ICE strategic alliance (March 2026); Computershare partnership (April 2026).

Citi tokenized asset market projections, as reported by CoinDesk, June 2026.