Saylor at Bitcoin 2026: Bitcoin as Pure Collateral

Bitcoin 2026 Day Two ran long.

The Venetian Expo Hall was packed end to end with new vendors, several handing out custom Pokemon cards as prizes. Old friends from DAS turned up at the coffee line. Michael Saylor took the Nakamoto Stage to close out the day.

This was my first time watching him speak in person. The pitch wasn’t about Bitcoin price targets or corporate treasury adoption. It was about a financial product most of the room had never heard of two years ago, and a thesis that, if it plays out, could reshape how a meaningful slice of the global credit market gets built.

Here’s what he was actually saying, in plain English.

The Thesis in One Sentence

Strategy holds Bitcoin. Strategy issues a preferred stock called STRC that pays a monthly dividend. STRC behaves like a fixed-income product. Bitcoin behaves like the collateral underneath it.

Saylor’s bet is that the world’s $300 trillion credit market is a much bigger opportunity than the world’s roughly $2 trillion Bitcoin market, and that Strategy has built the first product to bridge the two.

That’s the whole pitch. Everything else is plumbing.

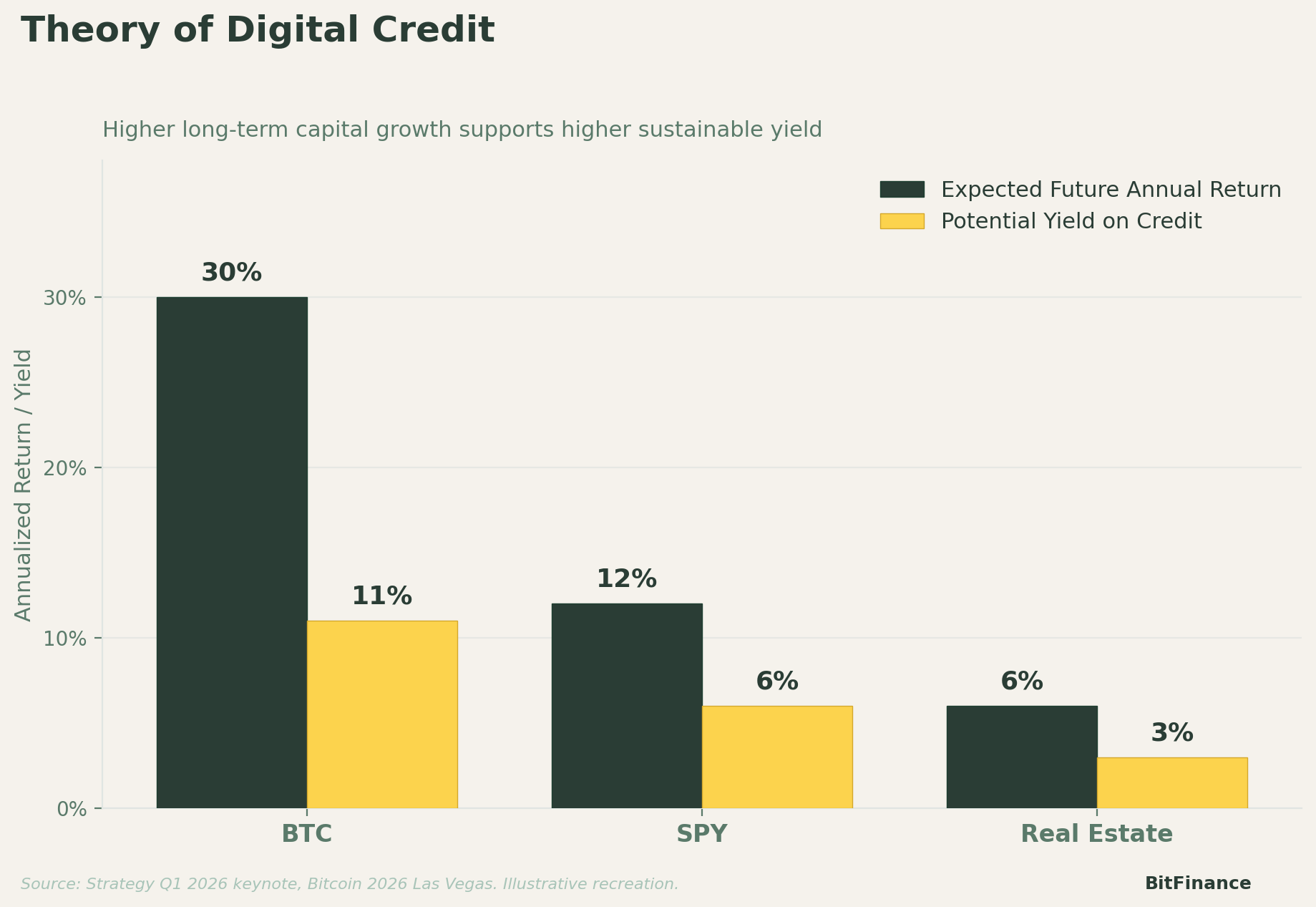

The case rests on a single relationship. Higher long-term capital growth supports higher sustainable yield on credit issued against it. If BTC compounds faster than equities or real estate, then credit backed by BTC can pay out more than credit backed by anything else.

Saylor’s framework: BTC’s higher expected return supports an 11% sustainable yield on credit, well above what SPY or real estate collateral can offer.

That ratio is the load-bearing assumption underneath every other claim in the keynote. If it holds, the rest of the architecture follows.

The Three-Layer Architecture

Saylor framed Strategy’s stack as three layers, which is the cleanest way I’ve heard him explain it.

Layer 1 is digital capital. That’s Bitcoin. The base asset. Volatile, scarce, appreciating over long horizons. Strategy holds it on the balance sheet.

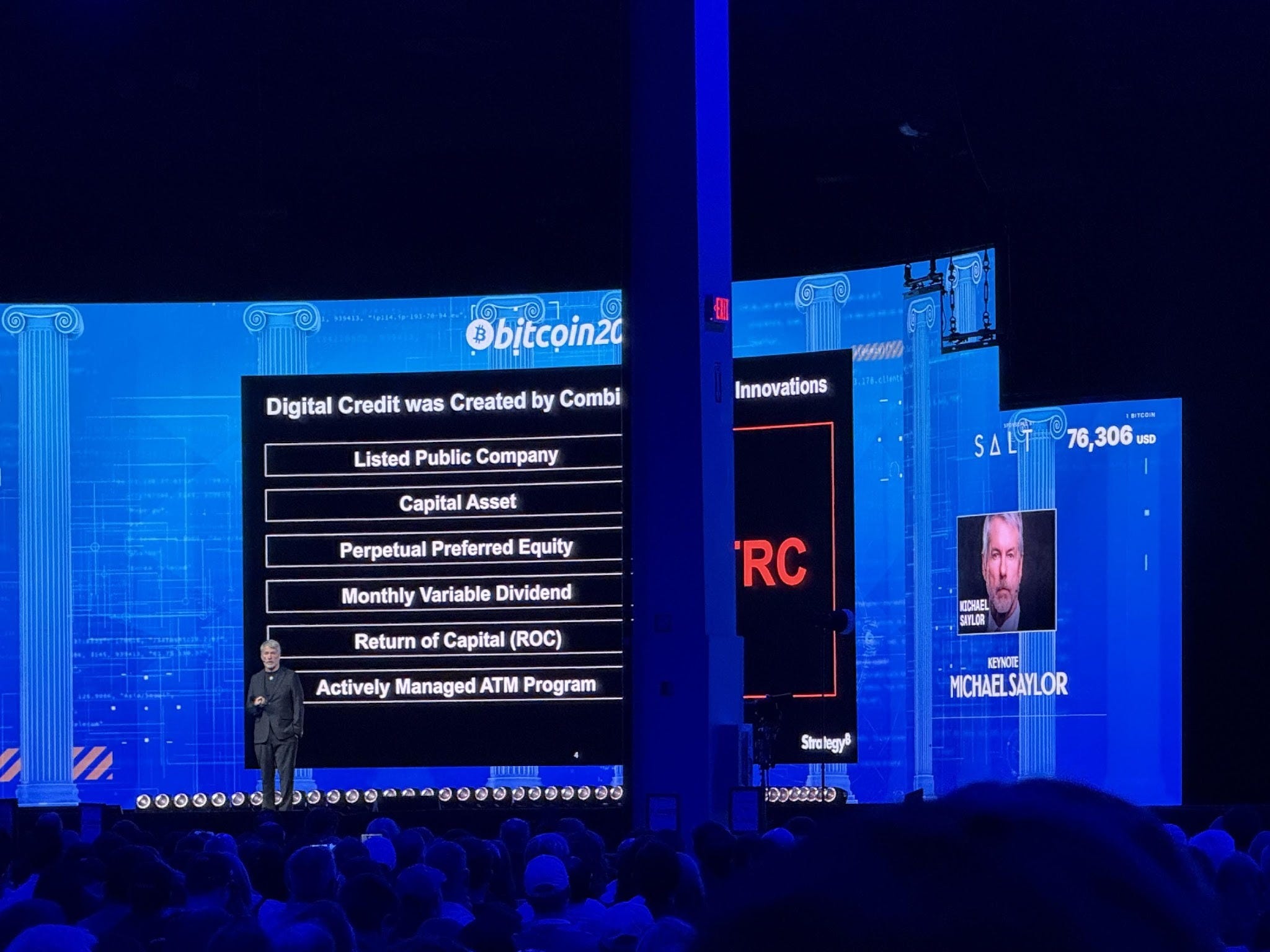

Layer 2 is digital credit. That’s STRC. A perpetual preferred stock that trades on Nasdaq, pays a monthly variable dividend (currently 11.50%), and absorbs Bitcoin’s volatility on behalf of investors who want yield instead of price exposure. Saylor described STRC as built from six innovations stacked together: listed public company structure, capital asset backing, perpetual preferred equity, monthly variable dividend, return-of-capital tax treatment, and an actively managed ATM program for issuance. Each piece by itself is ordinary. The combination, in his framing, is new.

Layer 3 is digital money. That’s the future state. Saylor wants STRC plumbed into ETFs, exchange-based yield accounts, and stablecoin issuers’ reserves so that a retail saver eventually gets exposure without having to know what STRC even is. BlackRock’s iShares Preferred & Income Securities ETF already holds roughly $210 million in STRC as its fourth-largest position. Strive and Tuttle Capital have filed for DGCR, the first dedicated digital credit ETF, currently awaiting SEC approval.

The Receipts

This is where the pitch went from abstract to concrete.

STRC reached roughly $8.5 billion in notional value in nine months. Saylor said that figure alone makes it larger than the entire existing universe of monthly-paying preferred securities combined.

He put annual growth at around 350%.

April inflows, annualized, point toward $38 billion a year. Strategy’s data shows STRC has financed the acquisition of approximately 77,000 BTC year-to-date in 2026, which Saylor claimed is roughly ten times the net inflow of all U.S. spot Bitcoin ETFs combined over the same period.

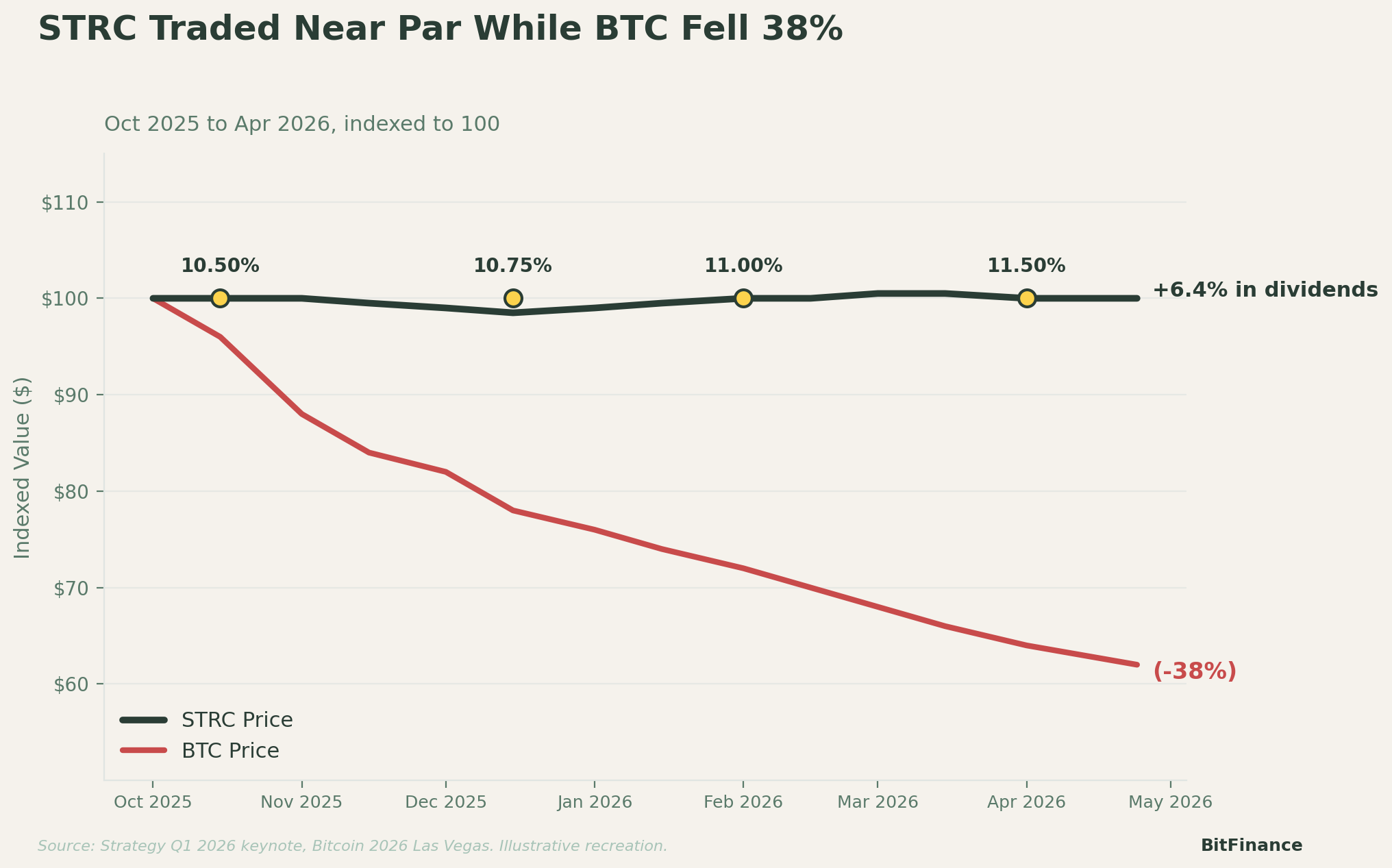

The chart on screen showed STRC trading near par from October 2025 through April 2026, paying a 6.4% cumulative dividend, while Bitcoin fell 38% over the same window. That single chart is the entire product pitch. If you wanted Bitcoin upside, you got hurt. If you wanted Bitcoin-backed yield with principal protection, you got paid.

Why Saylor Cares About Retail

One of the more interesting threads in the keynote was Saylor’s emphasis on accessibility. STRC trades on Nasdaq. Anyone with a brokerage account can buy it. Most comparable structured credit products are locked in private funds or restricted to qualified purchasers.

Saylor said roughly 80% of STRC holders are retail. 🤯

Corporate treasuries are starting to follow. Anchorage Digital, the first federally chartered U.S. crypto bank, has disclosed STRC holdings. Prevalon Energy announced a treasury allocation during the conference itself.

The contrast he drew with traditional private credit was sharp. Private credit, in his telling, is illiquid, opaque, and structured around what issuers want. Digital credit, by his definition, is liquid, transparent, and structured around what investors want. Whether you accept that framing or not, the distinction matters for anyone watching private credit wobble under $7B in Q4 2025 redemptions and rising default rates.

The Tax Wrinkle Most People Missed

STRC dividends receive return-of-capital treatment.

Plain English: investors can reinvest the cash flow without paying ordinary income tax on the full distribution. Returns compound over time the way Berkshire’s float compounds, just with a coupon instead of insurance premiums.

For a retail investor in a high tax bracket, that single feature might do more work than the headline yield.

What He’s Actually Solving

The deeper logic of the keynote is the accounting volatility problem.

Plenty of corporate treasurers want Bitcoin exposure. Boards don’t want the GAAP volatility that comes with holding it directly. GD Culture Group made the news this week reporting a $332 million unrealized loss on its $841.5 million BTC position and announcing plans to exit the entire stack to fund a buyback.

STRC is, structurally, an answer to that exact problem. Bitcoin economics without Bitcoin volatility on the balance sheet. Whether boards eventually accept it as a substitute remains the question.

What to Watch

Three things worth keeping in front of your dashboard.

The DGCR ETF approval is the next institutional unlock. If the SEC clears it, structured credit allocators get a regulated wrapper for digital credit exposure overnight.

The credibility of the dividend depends on the chart above holding. If BTC’s expected long-term return compresses toward equities, the spread between the 11% yield and the underlying asset class shrinks. That’s the single biggest dependency in the model.

The integration question is real. Saylor explicitly named Solana, Ethereum, Coinbase Base, Binance, Nasdaq, and the London Stock Exchange as venues where digital credit could eventually live. That’s a lot of rails for any single product to occupy.

Strategy isn’t a leveraged Bitcoin bet anymore. It’s a financial engineering platform with a Bitcoin balance sheet underneath. Whether Saylor’s $50 to $60 trillion target market materializes is unknowable from where we sit. Whether the company has built a genuinely new type of credit product is, at this point, a question with receipts.

Next up…XRP Vegas coming on Friday. Stay tuned!

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.