Saylor Finally Sold. Here’s the Part Nobody’s Pricing In.

If you hold Bitcoin, you probably saw the headlines this week. Michael Saylor’s company, MicroStrategy (aka “Strategy”), sold Bitcoin for the first time in 4 years.

Just 32 coins, about $2.5 million, sold to make a payment it had promised investors.

Around the same time, a product the company built to always be worth $100 quietly slipped to about $95, and Bitcoin itself kept sliding, down below $64,000. None of those numbers is big. Put them together, though, and they’re worth talking through, because the story underneath is simpler than the headlines make it sound.

What actually happened

A while back, Strategy started selling an interesting product that was relatively new to the crypto world. Think of it like a high-yield savings certificate.

You hand over $100, and the company promises to pay you $11.50 a year, forever, in cash. That’s it.

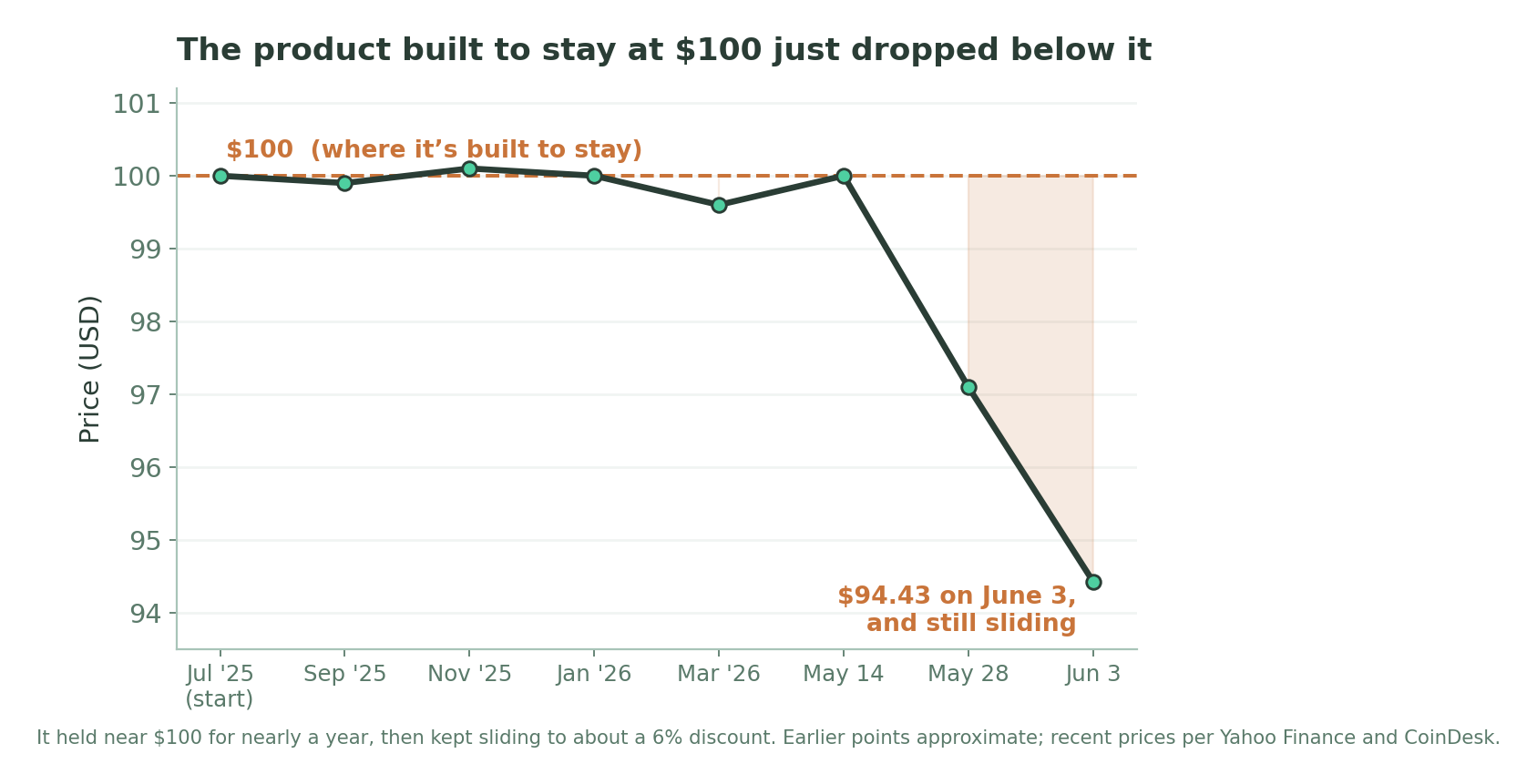

People liked it, the company raised billions, and it turned that money into Bitcoin. One rule makes the whole thing work: that certificate has to keep trading at around $100.

While it does, Strategy can keep selling fresh batches and keep buying Bitcoin. The moment it slips below $100, selling more becomes like offering $100 gift cards for $95, where you lose a little on every one.

For most of a year, that certificate sat right at $100.

This week it didn’t.

It hasn’t climbed back to $100 since May 14, and it kept sliding, closing near $94 on June 3. As I write this, almost none of it is changing hands above $100, which is the level Strategy needs in order to sell fresh batches. The engine it uses to raise money and buy Bitcoin has, for now, switched off.

Now the part that matters more than the price.

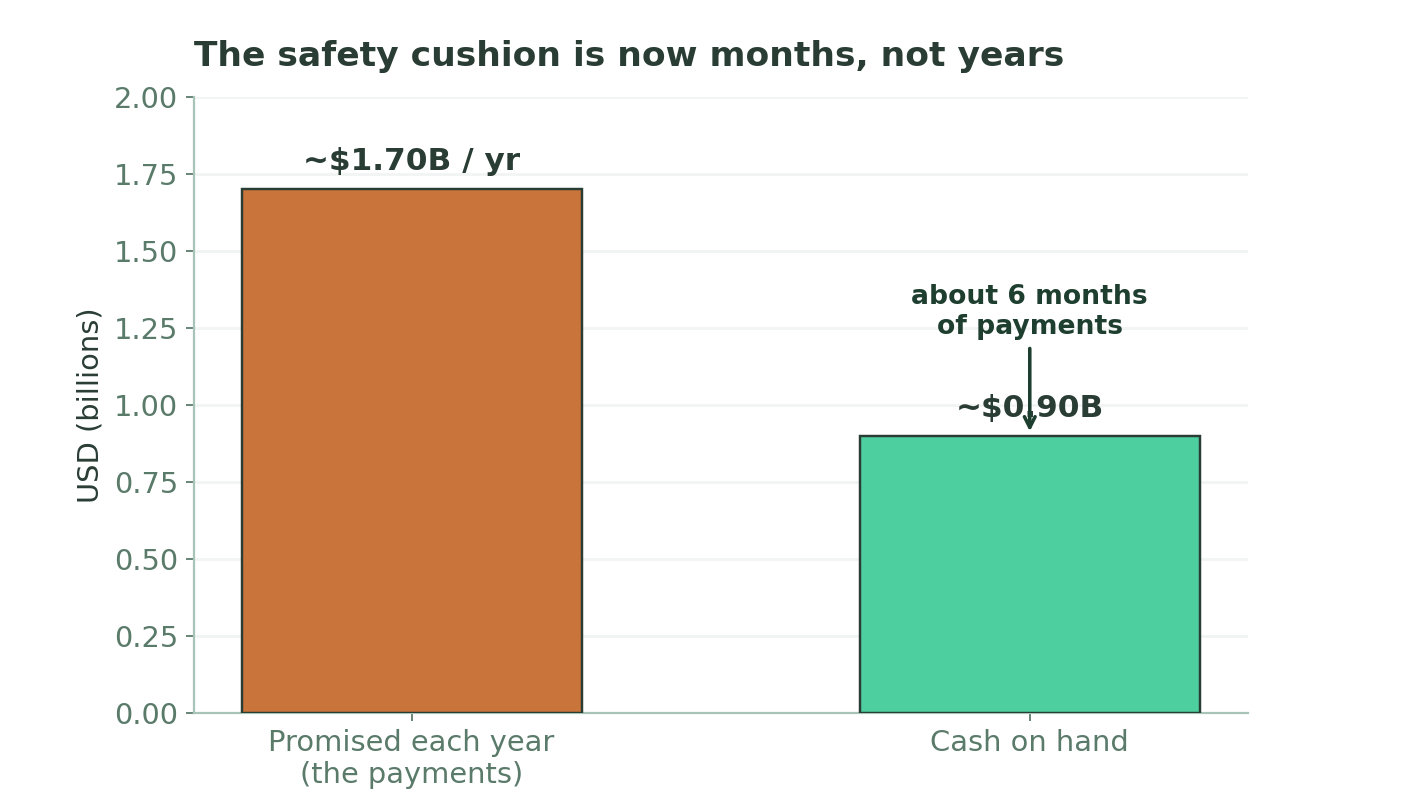

Those promised payments add up to about $1.7 billion a year. The 32 coins Strategy sold covered maybe half a month of that. Meanwhile the company’s cash, the rainy-day account it draws on to make those payments, sits at around $900 million, roughly six months’ worth. A year ago that cushion was measured in years. Today it’s measured in months per CoinDesk.

One more thing has happened since the sale.

Bitcoin has kept falling, down toward $63,000 as I write this, which is below the roughly $75,700 the company paid on average. Their entire pile is now worth less than they paid for it, at least on paper. That doesn’t force anything on its own, but it’s the backdrop against which every one of those monthly payments still has to be made.

Why 32 coins spooked everyone

The coins themselves are nothing. Saylor said outright he’d probably sell a little to make a payment, just to prove he could, and he still buys far more than he sells. The worry isn’t the size, but what it hinted at.

One analyst put it well back in January: Saylor can buy twenty thousand coins in a week and nobody blinks, but the day he sells even a couple hundred, the market panics.

This week was a small taste of exactly that. Another analyst this week called it the first real crack in the structure.

The treadmill nobody mentions

Here is the heart of it, and it’s something I wish more of us thought about before buying anything built on top of Bitcoin.

Bitcoin doesn’t pay you anything to hold it. It’s like a gold bar or a great painting, it just sits there and, we hope, becomes worth more.

That’s fine if you bought it with your own money and you can wait. It becomes a problem if you’ve promised someone $1.7 billion a year in cash, because a gold bar doesn’t write checks. You either keep bringing in new money, or you start selling the bar.

Saylor admitted as much. By his own math, Bitcoin has to climb about 2.3% every year just to cover those payments without selling stock. Picture a treadmill set to a slight incline. You have to keep walking just to stay in place. If Bitcoin runs hot, that’s easy. If it stalls or drops, the belt keeps moving under your feet.

BUFFETT FRAMEWORK QUESTION: Would you buy the whole thing?

Forget the share price and ask whether you’d want to own the entire company. You’d own a pile of Bitcoin that pays you nothing, plus a stack of promises to hand out about $1.7 billion in cash every year, backed by a bank account with maybe six months in it. It only works if the Bitcoin keeps climbing faster than the promises pile up.

Buffett built Berkshire on the opposite setup, where the money came in first and the assets paid their own way. It’s worth knowing which of those two you’re actually holding.

The same machine can spin backward

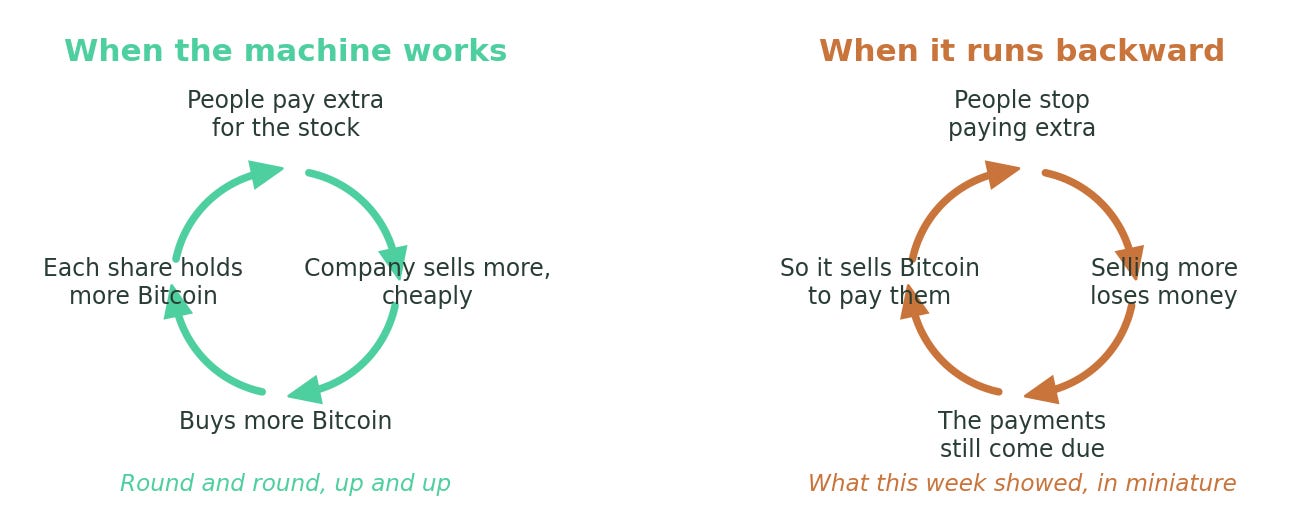

For years this was a beautiful machine, and I don’t say that to knock it. People trusted it so much they’d pay more for a share of Strategy than the Bitcoin inside was even worth. The company used that goodwill to sell more, buy more Bitcoin, and pack a little more Bitcoin behind every share, which made people trust it even more. Round and round, up and up.

The trouble is that the same wheel can spin backward.

Once people stop paying extra, and once that $100 certificate slips below $100, selling more stops being clever and starts losing money. The payments, though, don’t stop. They come every month no matter what. When the easy money dries up, the only thing left to sell is the Bitcoin itself. That’s what this week showed, in miniature.

Those 32 coins went to making a payment rather than buying more. There’s a competitor now too, Strive, paying 13% on a similar product that’s holding its value better, which makes Strategy’s 11.5% look thin right when it can least afford to sweeten the deal.

The Key Takeaway

Here is what I most want you to walk away with.

Saylor is not Bitcoin, and Bitcoin does not need Saylor. Full stop.

Bitcoin ran fine for eleven years before this company bought a single coin, and more people own it today, through funds, countries, exchanges, and regular folks, than ever before.

Strategy holds about 4% of all the Bitcoin there will ever be. That’s big enough to push the price around, and small enough that Bitcoin wouldn’t miss a beat if the company vanished tomorrow. What Saylor did was bring a flood of money and attention, and he also changed the story, turning Bitcoin from quiet, neutral money into the engine room of one company’s financial machine.

Some longtime holders love him for the bridge he built, while others feel he’s bent their asset to serve his balance sheet. Both can be true. The catch is that when adoption rides on one big, heavily borrowed-against player, it carries a way to fail that simply holding Bitcoin yourself does not.

Where I could be wrong, and whether it’s over

Now the fair side, because I won’t sell you a panic.

Six months of cash isn’t zero. The company has bought far more than it’s sold for years, even if it’s paused new buying since the middle of May, and that certificate has bounced back toward $100 before, usually around its payment dates. Plenty of smart people looked at this week and shrugged, and on the narrow facts they have a point.

What I’m describing is a bad-case story, not a prediction, and it needs three things to line up at once: Bitcoin flat or falling, the certificate stuck below $100, and that cash cushion running thin. What changed this week isn’t the odds, but that we finally watched the machine run in reverse with our own eyes.

So, is it really over? No, not this, and not now. A small sale to make a payment is not the death of Bitcoin, and anyone shouting that it is, is mostly selling you their own fear. The smarter move is to know what to keep an eye on.

That $100 certificate. If it keeps trading below $100, that’s the clearest warning light. There’s even a holder vote on June 8 about paying those dividends more often, a sign of how much keeping that level matters.

The company’s cash. Six months is the number that turns a worry into a real problem if it keeps shrinking.

How often, and how much, they sell. One payment’s worth of Bitcoin is noise. A habit is not.

The competition. Paying 11.5% while a rival pays 13% is a standoff that can’t last.

None of those is flashing red today, though a couple are amber. The company and the coin were never the same thing, even with 4% of all Bitcoin sitting on one balance sheet, and Bitcoin’s strength was never going to come from a single buyer.

The real risk worth watching is that its biggest holder turns out to be its most fragile one. Watch it with clear eyes, not fear, and don’t let anyone tell you those 32 coins were the whole story. They were the preview.

Until next time - trade safely fam!

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.