Michael Saylor’s "Never Sell" Bitcoin Strategy Just Got Edited

Picture a shopkeeper.

She’s sure the gold in her basement will keep climbing, and she doesn’t want to wait for it. So she offers her neighbor a deal: hand her $100, and she’ll pay him $11.50 a year, forever, in cash. She takes his money and buys more gold. As long as those paper slips keep changing hands at $100, she can sell new ones and keep buying.

The wheel turns.

That’s Strategy, and the “slip” is a preferred stock called STRC (with the ironic moniker, “Stretch”).

For most of a year it held near $100 while Bitcoin did whatever Bitcoin does. I walked through the design when Saylor laid it out at Bitcoin 2026, and it was clever, a way to bridge a small, volatile asset to the deep market for steady income.

The catch is the one I flagged a few weeks back:

Gold pays nothing, while the slips demand cash every month, about $1.76 billion a year across all of them.

So the wheel only turns while three things hold: the slips trade near $100, the gold keeps rising, and the neighbor keeps lending. This month the first one broke. STRC fell to about $74, an all-time low, a quarter below the price it was built to hold, and the financing engine seized.

Today Strategy answered. The answer is worth understanding in plain terms, because the company wrapped it in a lot of language.

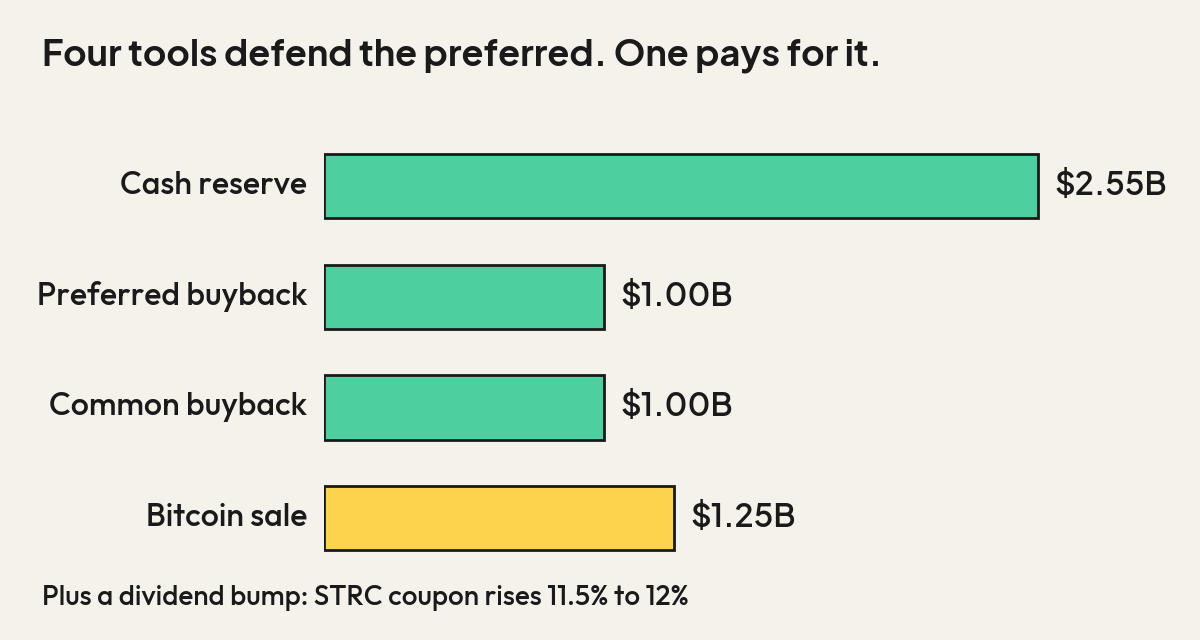

The rescue kit, in 5 parts

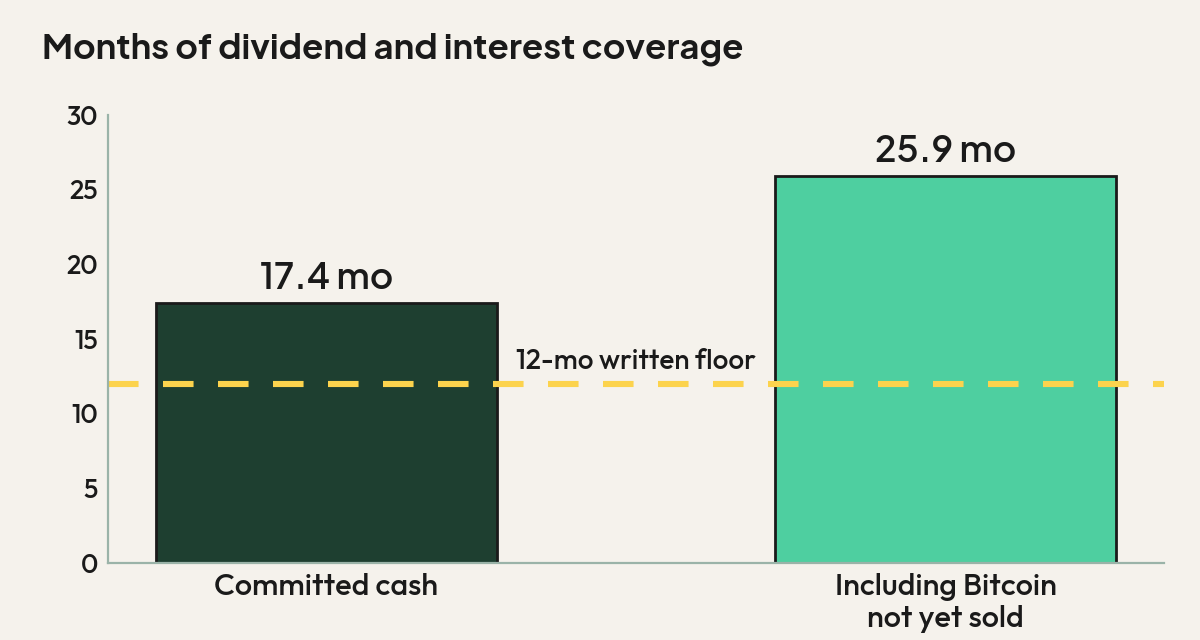

A reserve. Strategy set aside about $2.55 billion that can only go to the preferred holders and its lenders, roughly 17.4 months of those payments with a written 12-month floor. A few weeks ago that cushion was closer to six months. They’ve tripled it.

A preferred buyback. Up to $1 billion to buy STRC and its sister products on the open market. Buying back a $100 promise trading at $74 retires an expensive obligation at a discount. That part is sound.

A common buyback. Up to another $1 billion aimed at the common stock, MSTR.

A Bitcoin sale program. The part that changes the story. The board authorized selling BTC to fill the reserve, cover payments, and fund the buybacks, with up to $1.25 billion earmarked for the reserve alone and room for more.

BONUS: A higher dividend. The payment on STRC rises from 11.5% to 12%, a sweetener meant to coax the slips back toward $100.

Line them up and one picture forms.

Four of the five, the reserve, the dividend bump, and the two buybacks, exist to defend the slips. The fifth, selling Bitcoin, pays for the defense. The CFO said it plainly: “Bitcoin is capital.”

For a company built on hoarding Bitcoin and refusing to sell, that’s a different sentence than the one they used to repeat. 😬

You can read this two ways at once.

A company that issues when its securities are dear and buys them back when they’re cheap is acting like a capital-markets operator, and that flexibility is worth something. The same kit is also the clearest sign yet that the original design needed a backstop it wasn’t supposed to need.

Months of preferred dividend and interest coverage. The committed-cash figure is 17.4 months; the 25.9-month figure counts Bitcoin not yet sold. Source: Strategy, June 29, 2026.

How to read this, depending on who you are

In early June it was 32 coins, sold to make one payment, with Saylor framing the sale as proof he could. He finally sold.

Today it’s a named program with a dollar figure attached. The flywheel that only turned one way, raise money and buy, now turns both ways by policy. The CEO called it moving “from one-way capital issuance to active capital management,” which is fair, and also an admission that the one-way machine stopped working.

If you hold STRC, the near-term read is constructive, and the market didn’t just agree, it bought hard, sending the shares up about 12% on the day. A reserve, a higher payment, and a buyer standing under par all push the same way. Even so, STRC near $83 is still well below the $100 it’s meant to defend, and these dividends are declared by a board rather than guaranteed, so the structure still leans on Bitcoin not falling much further.

If you hold MSTR, the common stock, it’s more tangled. You now sit behind a larger, more expensive stack of promises. Part of that $2.55 billion reserve was filled by selling fresh shares, which means existing owners were diluted to protect the people standing ahead of them in line. The $1 billion buyback is a real sweetener, though it’s small against the size of the preferred stack. On top of that, the market is already skeptical: for the first time, Strategy’s combined value has slipped below the worth of the Bitcoin it holds. People are paying less for the wrapper than the contents are worth.

If you hold Bitcoin itself, which is most of us, this is the part I’d sit with. Strategy holds about 845,000 coins, near 4% of all the Bitcoin there will ever be, bought at an average around $75,700. With Bitcoin near $60,000, that pile is worth less than they paid. For most of Bitcoin’s life, its largest holders were buyers or, at worst, quiet. Strategy was the buyer everyone watched. As of today, by written policy, it’s also a programmed seller, with the selling tied to payment dates and moments of stress rather than to conviction. That’s new, and it’s the cleanest example I can point to of what I’d call the Saylor risk.

For the record, I’ll say it again:

Bitcoin doesn’t need Saylor.

It ran fine for 11 years before this company bought a coin.

What he added was a flood of money on the way up and, now, a mechanism that can turn into selling on the way down. When a single balance sheet holds 4% of the supply and has just told you it may sell into weakness to make its payments, that balance sheet becomes the largest single-company risk to the price that isn’t the market itself. Not a reason to panic. A reason to watch, closely, where their coins go.

Where this leaves us…

There’s a real case on the other side.

Several level-headed analysts read the STRC drop as a leverage cascade, forced margin selling rather than a verdict on the company. The reserve buys more than a year of time. Buying back a $100 promise at $74 is what a disciplined operator should do. The market also bought the package hard, up more than 12% intraday the day it landed.

The tailwind is real, provided it holds. A higher common stock pushes the company’s value back toward the worth of its Bitcoin, reopening share issuance on workable terms, and a firmer STRC eases the need to keep hiking the coupon or selling coins. The proviso is doing the work, though, since one strong session inside a hard month isn’t a trend.

What hasn’t changed is the shape of the thing. The business still doesn’t earn enough to cover its promises, so it covers them with capital markets, with Bitcoin’s price, and now with Bitcoin itself. A rescue kit is what you build when the product needed rescuing, and the tool with the longest reach points straight at the asset the whole story was meant to protect. I’m not betting on collapse, but I’m watching the coins, because for the first time the company has written down the conditions under which they leave.

So…are you a buyer of STRC? Or would you rather own Bitcoin?🧐

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.

Sources

Strategy Inc., “Digital Credit Capital Framework” related Form 8-K, June 29, 2026.

Strategy Inc. preferred dividend and interest schedule (STRC, STRK, STRF, STRD).

Nasdaq and Yahoo Finance, STRC and MSTR price history through June 2026.

Company disclosures on Bitcoin holdings (~845,000 BTC, avg. cost ~$75,700).