$18 Billion a Quarter Is Moving Into One App

The first time I bought crypto on Robinhood, I didn’t really own it. There was no wallet.

You couldn’t send your Bitcoin anywhere, because there was nowhere to send it from. What you held was an IOU from a trading app, a number on a screen backed by a promise.

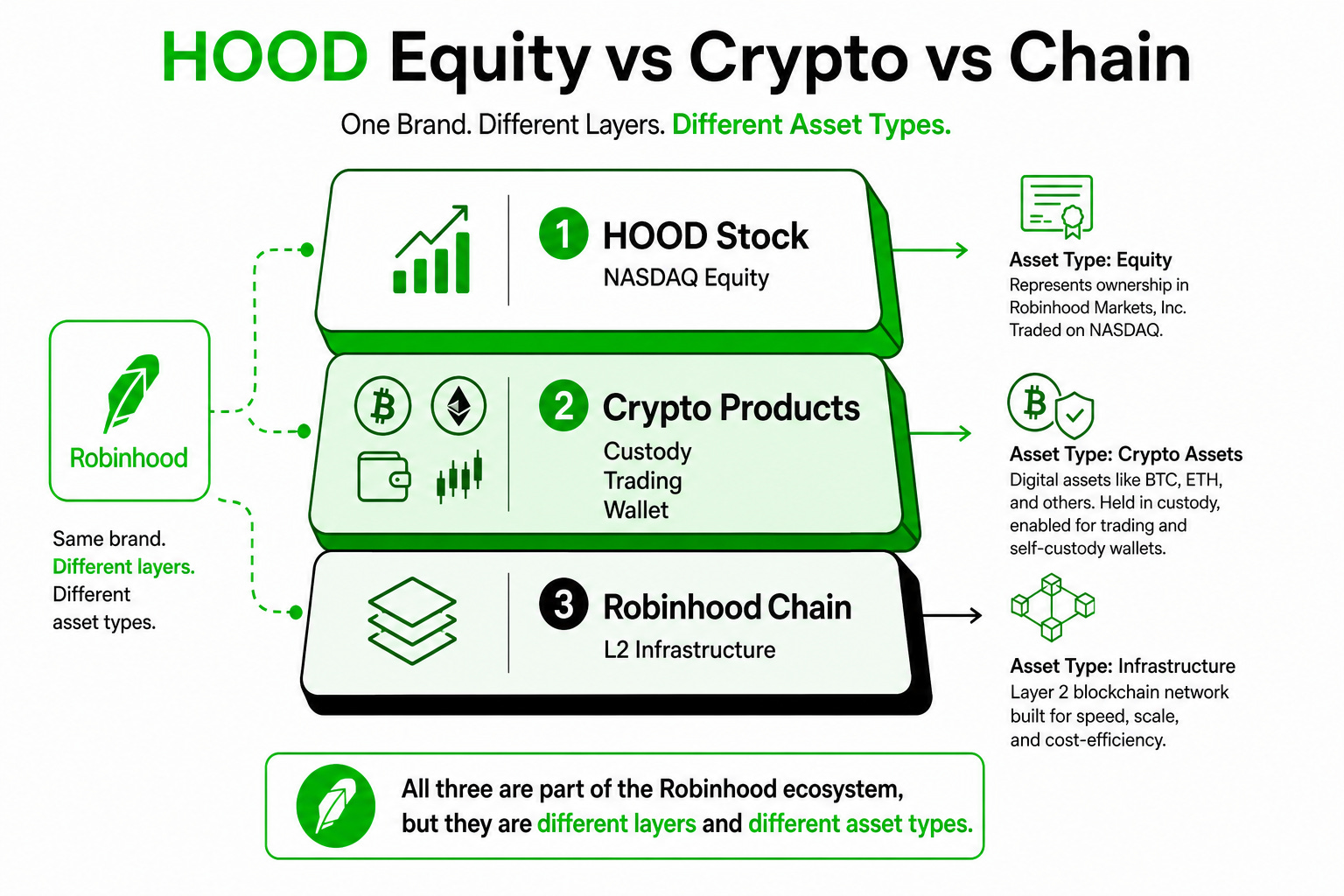

I bring that up because it’s the cleanest way to measure how far this company has traveled. On July 1, that same company launched the public mainnet of its own blockchain, with tokenized stocks trading in more than 120 countries and a lending product paying an estimated 7% on stablecoins. The trading app that once wouldn’t let you withdraw a coin now operates the settlement rails.

If you want a frame for what’s happening, look at Amazon around 2005.

At the time, most people still thought of it as a bookstore that had wandered into selling electronics. Then Prime arrived, a membership that made every additional product cheaper to use than the competition’s version, and the bookstore became the everything store.

Robinhood is running that same play, with Gold as its Prime. Hold that thought, because we’ll come back to it.

Try Naming Everything They Sell

Straight test: without looking, list every product Robinhood offers today. I follow this company closely and I still miss a few. That difficulty is the story, so let’s build the map.

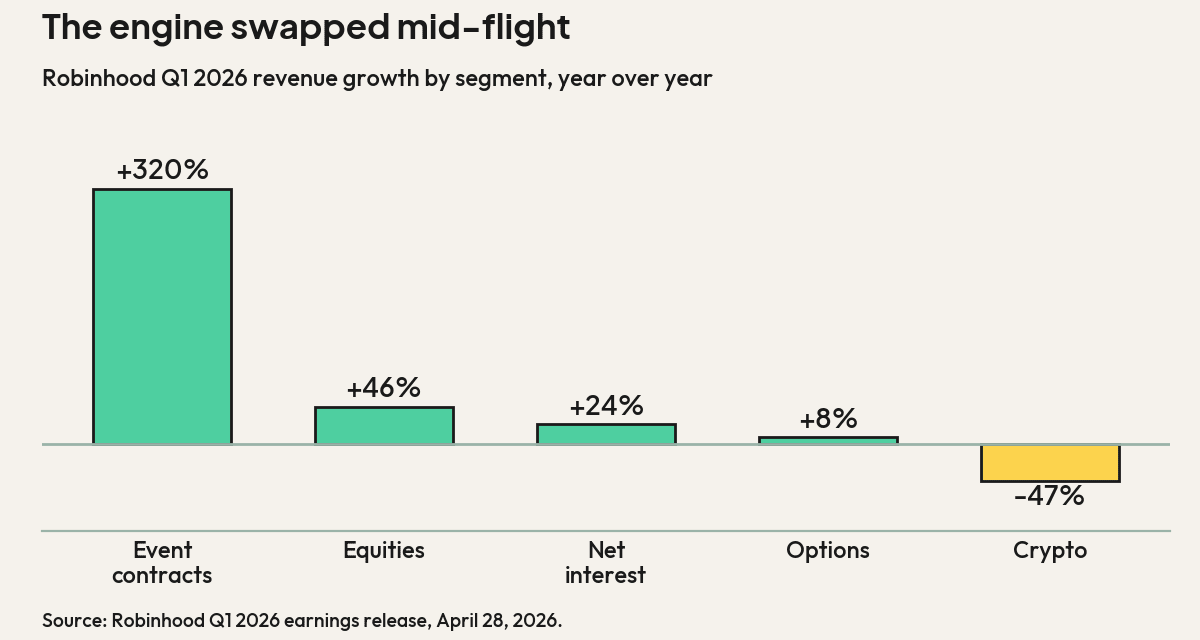

The brokerage. Still the core. Equities revenue grew 46% year over year in Q1, options revenue reached $260 million, and April was tracking as the highest-volume month of the year for both.

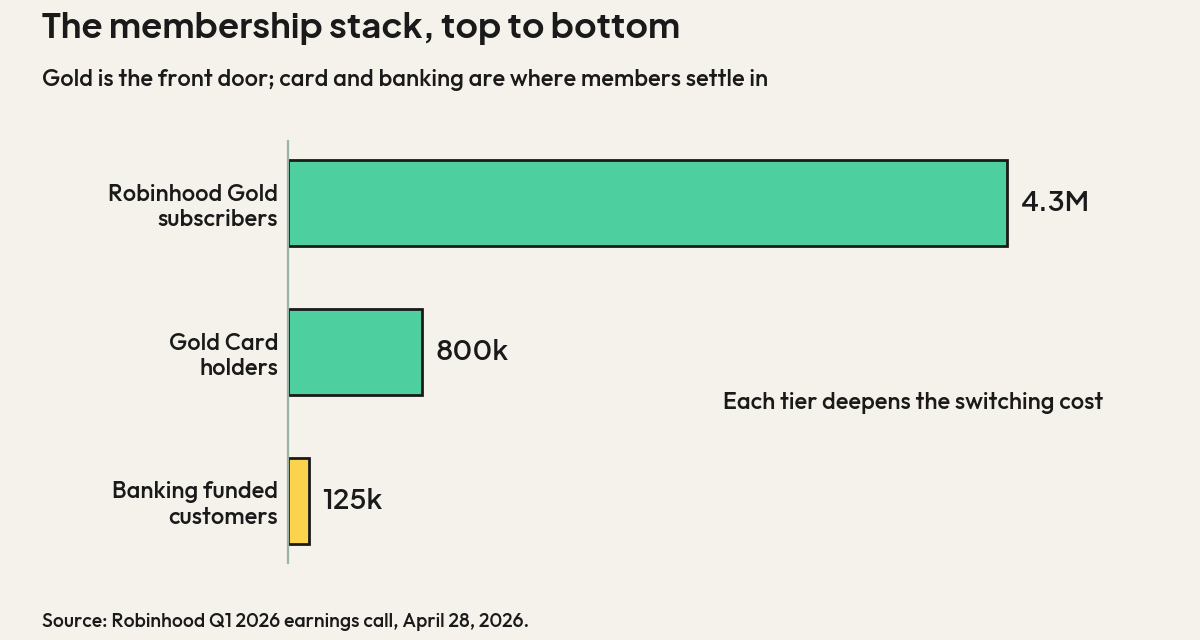

Gold. The membership layer. A record 4.3 million subscribers, up 36% year over year, with 40% of new customers now joining as Gold members. Perks include 3% IRA matching, high-yield cash, and lower rates across the ecosystem.

The Gold Card. More than 800,000 cardholders spending at a $15 billion annualized clip, with 3% cash back that lands in your brokerage account. Management says it’s on track to pass one million cards this year. A $695 Platinum Card now sits above it for the invite-only crowd.

Banking. Crossed $2 billion in deposits from more than 125,000 funded customers, with a 40% direct deposit attach rate. It grew five-fold in a single quarter.

Mortgages. A Gold perk through Sage Home Loans, a third-party lender, offering a rate roughly 0.75% below the national average plus a $500 closing credit. Robinhood isn’t the lender, but the mortgage now lives inside the membership.

Retirement. More than $30 billion in retirement assets, pulled in largely by that IRA match.

Prediction markets. The breakout. A record 8.8 billion event contracts traded in Q1, driving revenue in that category up 320% year over year to $147 million. Prediction markets out-earned crypto trading last quarter.

Robinhood Q1 2026 revenue growth by segment, year over year.

AI. Cortex Digests have reached nearly a million customers, Cortex Assistant is rolling out across the app, and agentic trading now lets users connect their own AI models to Robinhood’s data and execution tools, expanding from equities and options into crypto.

The chain. Robinhood Chain, a Layer 2 built on Arbitrum’s stack, went live July 1 with day-one liquidity from Uniswap and others, Chainlink as oracle infrastructure, stock tokens in 120-plus countries, and Robinhood Earn lending USDG at an estimated 7% through Morpho, insured through Lloyd’s of London.

The government contract. Robinhood is building the interface for Trump Accounts, the federal children’s savings program, a $100 million build contracted on a cost-plus basis with revenues expected to exceed costs.

Nine lanes, one app, roughly 28 million customers across 38 countries. Five years ago this was a stock-trading app with an IOU crypto product.

The hardest part of analyzing Robinhood in 2026 is keeping the list current.

The Options Classroom Nobody Copies

One piece of the ecosystem gets almost no coverage, and it might be my favorite.

Robinhood teaches options better than any app I’ve used, walking you through strategies, showing you profit and loss curves before you commit, and explaining assignment risk in plain language instead of burying it in a PDF.

Cynics will say the education exists to funnel users into the highest-margin trading product, and they’re partly right. Options generated $260 million last quarter, so the incentive is obvious. But the same logic applies to every brokerage on earth, and the others still make you learn options from YouTube.

Teaching the product well while profiting from it beats profiting from it while leaving customers confused.

There’s a bigger idea hiding in that classroom too.

The next generation of investors, the one inheriting wealth through the largest generational transfer in history, shows little appetite for handing assets to a traditional adviser. They want to be their own adviser, and they’ll choose the platform that makes self-direction feel safe.

Education is how Robinhood wins that choice.

The Advisor Network they launched for users who do want a human, and the Strategies robo product with fees capped for Gold members, cover the rest of the spectrum.

The Flywheel Has a Scoreboard

Product lists are cheap. The question is whether the pieces reinforce each other, and Robinhood publishes the number that answers it.

Management calls net deposits their North Star, and in Q1 customers brought in $18 billion, another quarter above a 20% annualized growth rate. Total platform assets reached $307 billion, up 39% year over year. Money is consolidating onto the platform faster than the market alone can explain.

Here’s why the Amazon Prime comparison holds:

Prime worked because each new benefit made the membership harder to cancel, even when any single benefit was replaceable.

Ever tried to leave your bank (*cough* bank of america *cough* ) and recognize how challenging and annoying it would be to have to re route all your auto payments, subscriptions etc? In economics these are known as “switching costs” and companies rely heavily on them to keep you as a customer.

Robinhood Gold works the same way.

The IRA match pulls in your retirement account. The card’s cash back lands in your brokerage. The banking product pays yield your bank won’t. The mortgage discount requires the membership.

Cancel Gold and you don’t lose one product, you unwind six. Switching costs like that never show up on a balance sheet, but they show up in a 16% attach rate and in deposits compounding at 20% a year.

Membership stack: Gold is the front door, and each tier deepens the switching cost.

What Coinbase and Webull Don’t Have

Every competitor in this comp set is vertical.

Coinbase and Kraken are crypto companies reaching toward equities. Webull is a trading app. Even the tokenization race makes the point: Kraken’s xStocks and Coinbase’s announced product both distribute tokens on infrastructure someone else controls, while Robinhood built the settlement layer itself.

Owning the chain means owning the toll road, and everyone else is renting.

Horizontal is harder to execute but harder to displace. A customer can leave Coinbase for Kraken in an afternoon because only one product moves. Leaving Robinhood means moving a brokerage account, an IRA with a vesting match, a credit card, direct deposit, and possibly a mortgage relationship. The moat isn’t any single product, since every single product is copyable.

The moat is the accumulated inconvenience of leaving.

Buffett Framework Question: Would Buffett call this a durable moat? He famously prizes businesses a competitor couldn’t hurt with unlimited capital. Any rival with money can copy a 3% card or an IRA match, and several are trying. What they can’t easily copy is nine products already stitched into one membership with $307 billion sitting inside it. The straight Buffett answer is that switching costs are a real moat but a younger, less proven one than a brand like Coke’s, and the durability test is whether net deposits keep compounding when the perks stop being subsidized.

A Fair Reading Owes the Skeptics Their Due

The bull case above is real, and so are the cracks, so let’s take them straight.

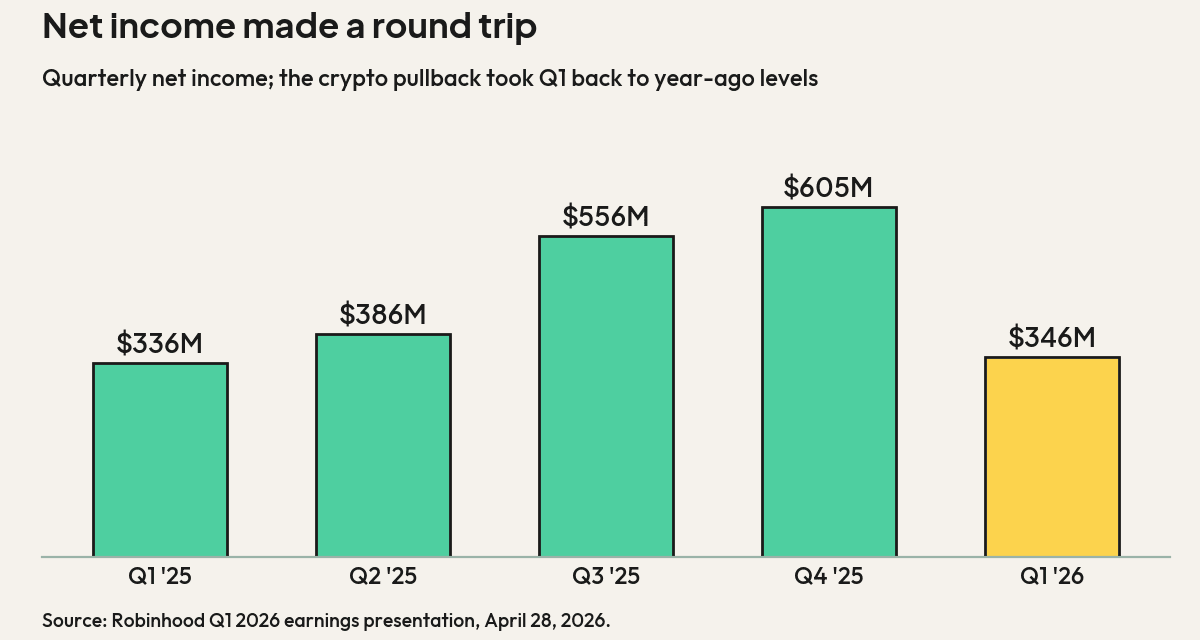

Q1 missed on both lines, with revenue of $1.07 billion against a $1.14 billion consensus and EPS a penny light, snapping four straight quarters of beats. The culprit was crypto, where revenue fell 47% year over year to $134 million as trading volumes dropped by nearly half. A company this exposed to trading activity inherits the market’s mood swings, and the five-quarter net income chart below looks like a round trip for a reason.

Quarterly net income: the crypto pullback took Q1 2026 back to year-ago levels.

The new Stock Tokens carry a structural caveat every buyer should understand: they’re tokenized debt securities, with no voting rights and no direct claim on the underlying shares, a structure the SEC’s January guidance flagged for heightened scrutiny.

Prediction markets, the fastest-growing revenue line, sit in a regulatory gray zone that several states are actively contesting. The Trump Accounts contract ties the brand to a politically charged program. The company also cut roughly 10% of its workforce weeks before the chain launch, which reads as discipline or as strain depending on your priors.

The deepest risk is the oldest one in business: focus.

Amazon survived doing everything because retail logistics compound into one capability. Whether brokerage, banking, blockchain infrastructure, AI agents, and a federal contract compound the same way is the open bet, and companies have died attempting less.

The Bookstore Phase Is Over

Amazon spent years being underestimated as a bookstore with a side hustle, right up until the membership flywheel made the everything store inevitable. Robinhood is somewhere in the middle of that same arc, past the point where “trading app” describes it, well short of the point where the bet is proven.

I’m bullish on the direction because the scoreboard number, deposits compounding above 20% while nine product lines feed one membership, is the same pattern that made Prime one of the great business models of the century. I hold that view knowing the revenue still swings with trading moods, the tokenization structure has a regulatory question mark on it, and execution across nine lanes at once has humbled better-resourced companies.

The IOU era ended. The everything-app era is an experiment running in public, and the deposit number will tell us how it’s going long before the headlines do.

Until next time fam!

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.

Sources

Robinhood Reports First Quarter 2026 Results (April 28, 2026)

Robinhood Newsroom: Robinhood Chain Mainnet, Stock Tokens, Agentic Trading (July 1, 2026)

CoinDesk: Robinhood rolls out public blockchain (July 1, 2026)

Forbes: Robinhood Launches Its Own Blockchain, New Stock Tokens and DeFi Products (July 1, 2026)

Robinhood Gold overview (Gold, Gold Card, Banking, Sage Home Loans mortgage perk)

Robinhood Newsroom: Take Flight (Platinum Card, family finance)