Most Crypto Tokens are Uninvestable by Design

I keep having the same conversation: The price is low, the project has partnerships, so the person across from me has decided the token is a generational buy.

“It could go up ten times from here, so even a small position makes sense.”

I want to take that apart, because the equation rests on two mirages and a moat that was never there.

Set Bitcoin and Ethereum aside first. They captured market share and network effects that are real and hard to copy, and they’re not what this is about. This is about everything underneath them, the long list of smart-contract platforms and infrastructure tokens that trade on narrative and partnership announcements. For that group, the case for owning the token is weaker than almost anyone holding one wants to admit.

There’s no moat in decentralization

Start with what makes any asset worth owning.

A business holds value because it can defend its profits.

Pricing power, switching costs, exclusivity, a brand, a network competitors can’t replicate.

Warren Buffett calls it a moat, and the whole job of an investor is finding one and buying it at a fair price.

Decentralization is the deliberate removal of the moat.

That’s not a criticism, it’s the entire pitch to users. The code is open source, so anyone can fork it. The network is permissionless, so no one can be charged rent or shut out. No company owns it, so no company can extract value from it. Those properties are why people find decentralization appealing, and they’re the same properties that make the token impossible to value. Capital wants control. Decentralization is the surrender of control. You can’t build a durable claim on something designed so that nobody can hold a durable claim on it.

That’s the root of everything below. No moat means no defensible value, and no defensible value means there’s nothing for the token to capture.

Buffett Framework Question: “Where is the moat?” For most crypto tokens, the answer is that the protocol was built so there wouldn’t be one. That’s a feature for the people using it and a problem for the people holding it.

Mirage #1: It’s cheap; therefore “value”!

A low price feels like safety. It usually measures the past instead.

When a stock falls, its cash flow puts a floor under it. Earnings, book value, a dividend yield that rises until buyers step in. A decentralized token has no claim on cash flow, only an emission schedule that prints more supply on a timer. Nothing sits underneath the price.

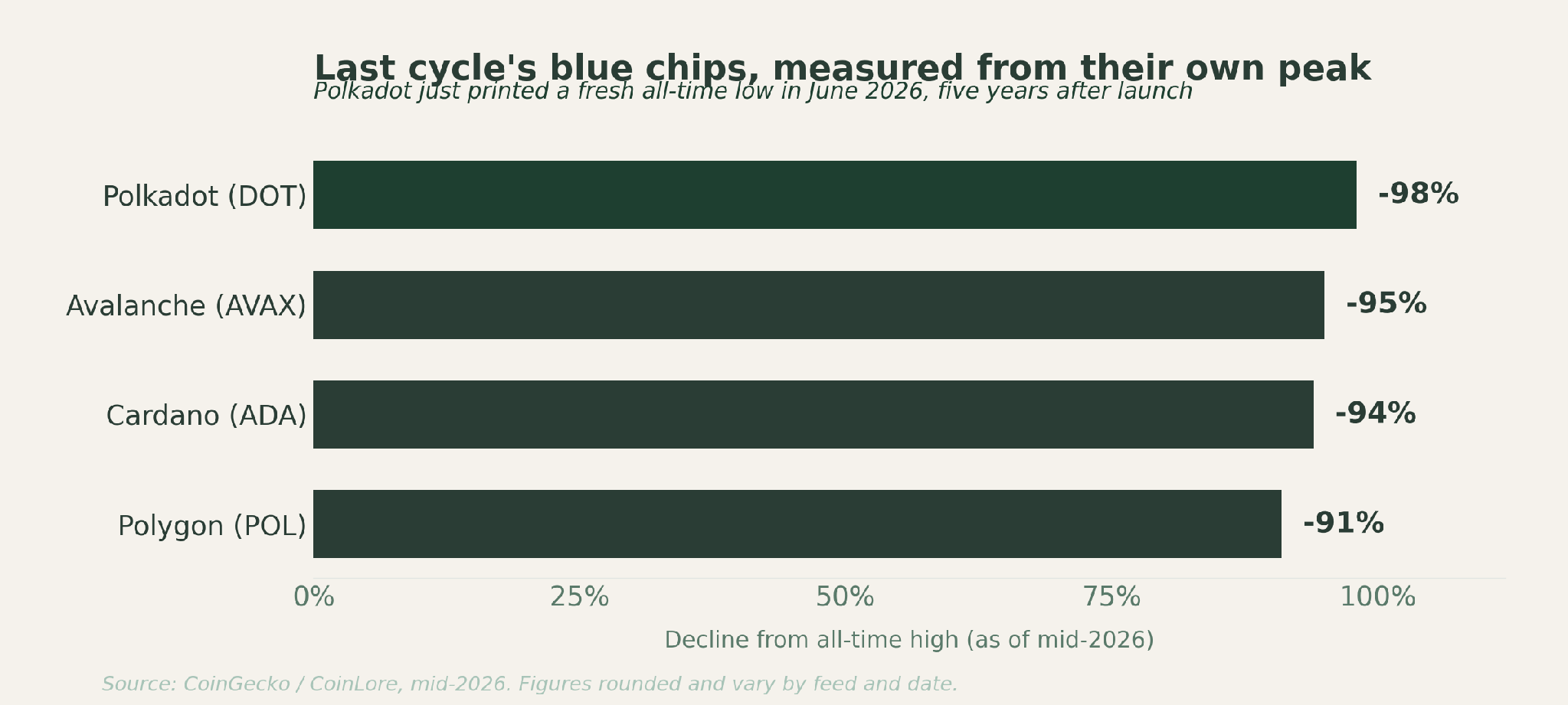

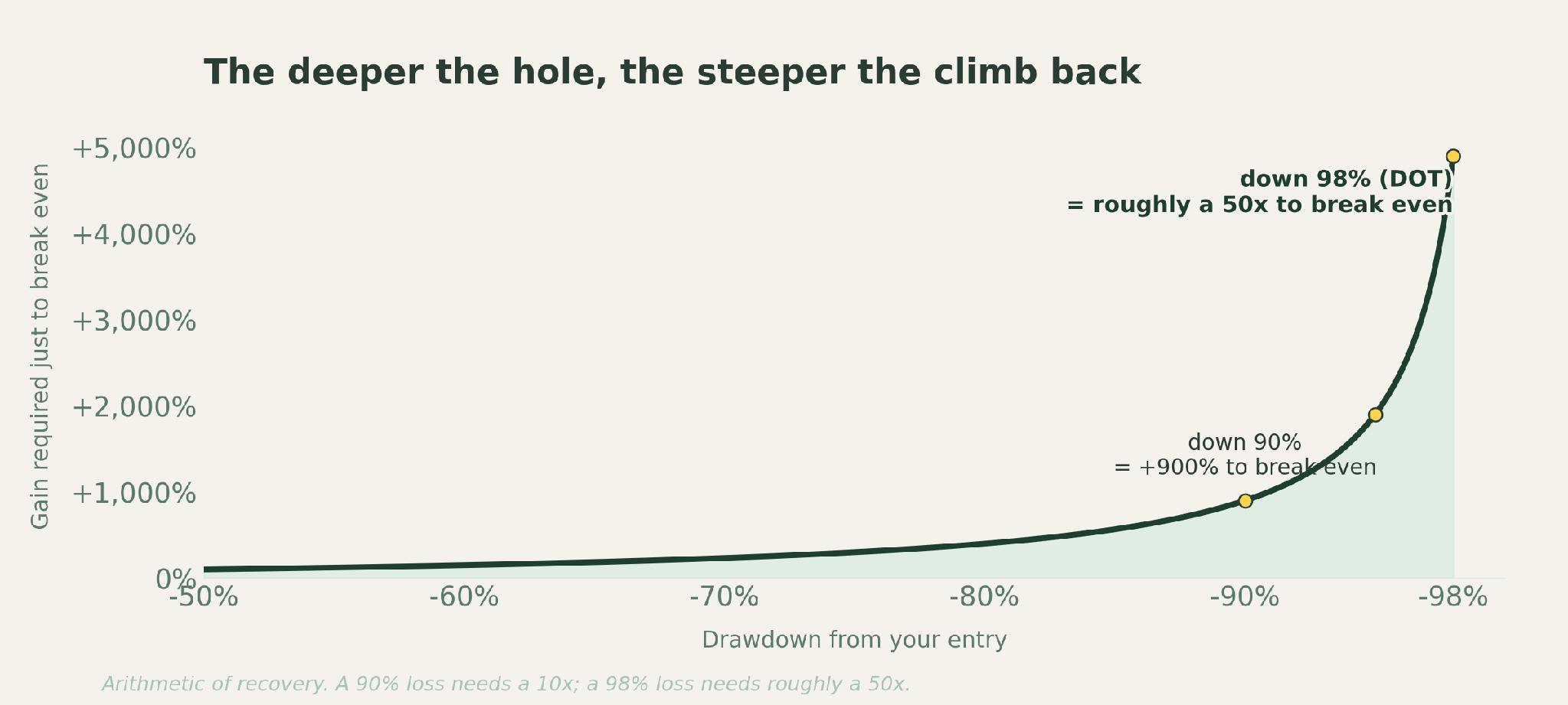

So when a token is down 98%, that’s not a bottom, it’s a number.

It can fall another 50%, another 75%, another 100% and on and on and on because there is no structural floor in crypto for assets like these.

Polkadot makes the point. It’s down about 98% from its 2021 high and printed a fresh all-time low this month, five years into its life.

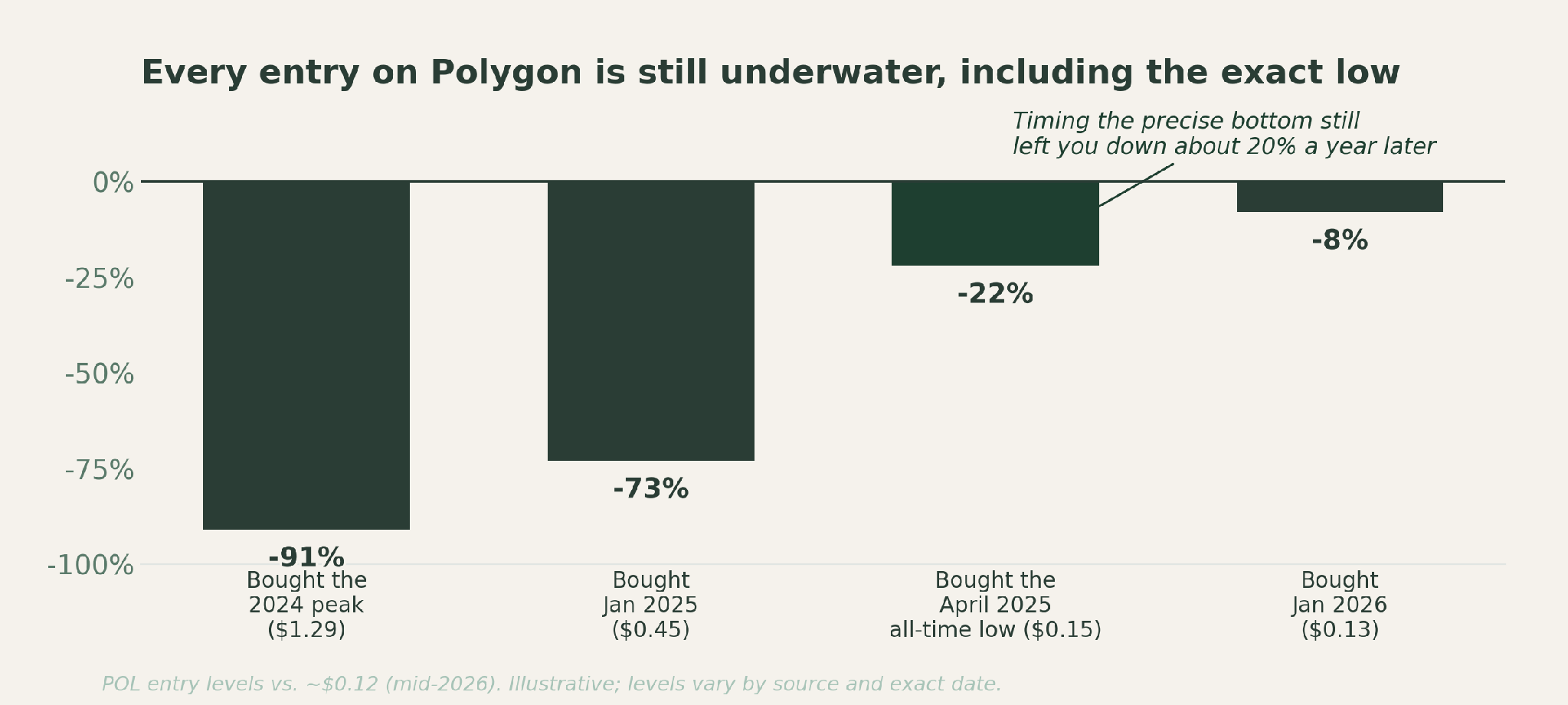

The people who think they’re safe because they timed it well are often the clearest warning. Look at Polygon through four buyers.

The one who bought the 2024 peak is down about 91%.

The one who bought the exact April 2025 all-time low, the buyer everyone wishes they were, is still down about 20% a year later. Even buying the precise bottom didn’t make them whole.

The big irony is that these projects can’t really die. A company that fails goes bankrupt, and its creditors and shareholders get a claim on the cash and hard assets left behind, a real recovery value. A decentralized token has no such moment: it can’t be liquidated or wound down, so as long as a handful of holders and validators remain, it drifts lower forever, with no terminal event and nothing left to divide.

Cheap is doing none of the work people think it’s doing.

Mirage #2: It Has Partnerships!

A partnership means a company is using the technology. It does not mean value reaches the token, and the clearest evidence is that these deals have been in place for years and have done nothing for the price.

Take the one people point to:

California digitized 42 million vehicle titles on Avalanche.

The state runs it as a sovereign, permissioned chain with its own validators.

Since the Etna upgrade, a chain like that pays the Avalanche protocol a flat fee of roughly 1.33 AVAX per validator each month, fixed no matter how much activity flows through.

At today’s price that’s around nine dollars per validator a month, so the protocol’s entire take from the California DMV lands somewhere in the hundreds to about a thousand dollars a year.

Now follow that money to the token holder, because it doesn’t arrive.

Every fee on Avalanche is burned rather than paid out, so there’s no dividend and no buyback to receive. The protocol also mints new AVAX as staking rewards faster than fees burn it, which kept the token inflationary at around 3% in late 2025. The holder absorbs dilution while the network grows.

For scale, Avalanche’s single busiest fee day on record, about $521,000, came from an October 2025 liquidation cascade rather than from any enterprise use, and the whole network collected roughly 132,000 AVAX in fees for the quarter.

A state title registry doesn’t move numbers like that, and even if it did, the money gets burned, not distributed.

Set that against the comparison the bull is implicitly making. Visa earned about $40 billion last year and returned roughly $22.8 billion to its shareholders. Owning Visa is owning the toll booth, with a legal claim on the tolls. Owning AVAX while California runs titles on Avalanche is owning a token that collects a few dollars a month in validator fees and then destroys them.

The technology got adopted. The holder got a headline.

Avalanche says it plainly in its own case study. When JPMorgan’s Onyx unit, Apollo, and WisdomTree ran a tokenization trial on a permissioned Avalanche subnet, the case study notes the subnet’s economics are not dependent on any crypto token.

That’s the company confirming the gap between using the rails and owning the coin.

The pattern repeats across the names people cite:

JPMorgan. Its own ledger runs on Quorum, a private fork of Ethereum with no public token at all. The largest US bank built serious blockchain infrastructure, and there’s nothing for an investor to buy.

IBM and Hyperledger. They powered the first wave of enterprise blockchain, Maersk’s TradeLens and Walmart’s Food Trust, on permissioned, tokenless systems. TradeLens shut down in 2023.

VeChain. Built for enterprise supply chains with partners like DNV, BMW, and Walmart’s China operation. VET trades near a penny, down about 96% from its 2021 high.

Stellar. Real institutional flows, from MoneyGram settlement to a Franklin Templeton tokenized fund. XLM still sits around 75% below its 2018 high.

Adoption is a property of the network. Value accrual is a property of a claim, and these tokens don’t carry one.

The 10X argument runs backwards

The most sophisticated version of the bull case isn’t a prediction, it’s an asymmetry. The token can go up ten times, so a small bet is rational even when it usually fails.

Two things break that.

First, the catalyst people name for the 10x is the partnerships, and the partnerships have sat in place for years without moving the token. The upside thesis is disconnected from its own evidence. Whatever would drive a re-rating hasn’t shown up, and it isn’t the thing being pointed to.

Second, the downside is as open as the upside. The asymmetry people imagine is capped downside with uncapped upside. For a token with no floor, the downside is uncapped too. Down 98% can become down 99%, and down 99% can become zero.

A bet where both ends are open isn’t the asymmetry that makes a generational buy. It’s a coin flip dressed up as one.

Capitalism takes the technology and leaves the token

Now let’s tie it together.

Private companies don’t want decentralization. They want efficiency they control.

To accomplish this, they take the open-source rails and run them on permissioned instances built for their own benefit; not the network’s.

Visa, Mastercard, and JPMorgan don’t need a public token to settle faster or tokenize a fund. They need the technology, and the technology is free to take. The moment something valuable can be captured, a company captures it privately, behind its own walls, where the gains accrue to the company rather than to a floating coin. There’s no money in being decentralized, because decentralization is the one structure that guarantees the value can’t be fenced off and kept.

This is why I can be bullish on tokenization and bearish on these tokens at the same time. The shift to programmable rails is real and large. It runs on infrastructure institutions govern, and it doesn’t need the 2021 narrative tokens to get there.

One thing could change all of this thinking…

I’ll give the other side its strongest card.

IF (and this is a big “IF”) legislation like the CLARITY Act creates a clean path for a token to register as a security, that token could be required to pass real profit back to holders through a dividend or a mandated buyback.

A claim like that is exactly the moat these tokens lack, and it would change the analysis. It’s a possible future, not the present one, and most tokens won’t qualify or won’t pursue it.

Until that’s law and durable, the support under the price is the next buyer’s optimism.

Where this leaves you

The equation that starts these conversations, low price plus partnerships equals generational buy, is built on two mirages and a moat that was never there. Cheap measures the past. Partnerships measure usage, not ownership. The structure underneath all of it, decentralization, is the deliberate absence of the thing that lets an asset hold value.

Most crypto tokens are uninvestable by design; invest accordingly.

The phrase to sit with is “by design.” Nobody has to break these tokens for them to keep falling. They were built without a way to capture value, on purpose, and a 98% discount on something with no claim and no moat is not a discount.

It’s a lower price on the way to a lower one.

Securities legislation is the live risk to this view. A token that wins a clean path to pay holders gets the claim it lacks today. The same is true if a network sustains fee burns above emissions for years rather than weeks, which would start to resemble a buyback, or if one of these projects develops genuine network effects that hold up without paid incentives.

I’m watching all three, and I’ll change my mind when the data does.

Until next time…trade carefully out there friends and keep an eye out for strong, structural moats.

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.

Sources and notes

Drawdowns from all-time high (DOT about 98%, AVAX about 95%, ADA about 94%, POL about 91%) and Polkadot’s fresh all-time low near $0.89 on June 6, 2026: CoinGecko and CoinLore, as of mid-June 2026.

Polygon entry levels and the roughly $0.12 reference price: CoinGecko and CoinMarketCap historical data; the April 2025 all-time low near $0.15. Levels vary by feed and exact date.

Avalanche L1 validator fee of about 1.33 AVAX per validator per month, fixed regardless of transaction volume: Avalanche Builder Hub and the Etna / ACP-77 documentation (Avalanche9000, activated December 2024).

All Avalanche fees are burned; the network ran roughly 3.0% annualized inflation in Q4 2025; the busiest single fee day was about $520,715 on October 10, 2025; quarterly fees totaled about 132,016 AVAX: Messari, State of Avalanche Q4 2025 (January 2026).

The JPMorgan Onyx, Apollo, and WisdomTree tokenization proof-of-concept on a permissioned Avalanche Evergreen subnet, and the statement that the subnet’s economics are not dependent on any crypto token: Avalanche case study, “In Focus: Onyx by J.P. Morgan” (avax.network). Onyx’s own ledger is built on Consensys Quorum.

Visa’s roughly $40 billion in annual net revenue and about $22.8 billion returned to shareholders: Visa fiscal year 2025 results.

VeChain near $0.011 with an approximately billion-dollar market cap, down about 96% from its 2021 high; enterprise partners include DNV, BMW, and Walmart’s China operation: CoinGecko and Coinbase, mid-2026.

Stellar near $0.22, roughly 75% below its 2018 high; institutional use includes MoneyGram and Franklin Templeton’s tokenized money market fund: market data and company disclosures, mid-2026.

Maersk’s TradeLens, built on IBM and Hyperledger Fabric, shut down in 2023; Walmart’s Food Trust runs on the same permissioned, tokenless stack: public reporting.