I Don’t Usually Talk About Specific Tokens. These Two Earned a Spot in My Portfolio.

If you’ve been reading BitFinance for any length of time, you know I don’t spend a lot of ink on specific tokens. I write about frameworks, infrastructure, and the structural trends reshaping how capital moves through digital asset markets. I’ve always believed that process matters more than picks.

But sometimes the process leads you to a pick. And sometimes you owe it to your readers to be transparent about where your own capital is going and why.

I have been systematically adding two positions to my portfolio in this bear market. What I saw this week at the Digital asset Summit confirmed my convictions as the conversations I had with institutional builders reinforced the thesis for both. They represent about 10 to 15% of my overall portfolio. That’s deliberate. I’ll explain the sizing later.

The two tokens are Hyperliquid (HYPE) and Morpho (MORPHO).

They’re not in the same business, and I’m not framing this as a comparison. They serve different functions in a portfolio, and that’s precisely why they belong together.

One is a growth position.

The other is an infrastructure position.

Together, they give me diversified exposure to what I believe are two of the most durable revenue-generating protocols in digital assets.

Here’s the case for each, with honest assessments of the risks.

The usual disclaimer applies: this is educational, not investment advice.

Do your own research and use your own judgment before making any moves.

Buffett Framework Question:

“Does the business make money independent of the token price?” That’s the first filter. Both HYPE and MORPHO pass it. Most altcoins don’t. That’s why most altcoins don’t belong in a serious portfolio.

Why These Two, and Why Now

The altcoin market in 2026 is brutal. Most tokens are down 50% or more from their highs. Narratives have cooled. Retail interest has faded. And yet, buried under the noise, there’s a handful of protocols that are generating more revenue than ever.

That divergence is the opportunity. When the market prices everything like a memecoin, you can buy businesses at speculation prices. It won’t last forever, and I’m not calling a bottom. But I am saying that the fundamental picture for these two protocols has never been stronger, and the prices reflect a market that isn’t paying attention to fundamentals.

The filter I use is straightforward: real revenue from real usage, growing adoption driven by institutional integrations, a token that captures some portion of that value, and a competitive moat I can understand well enough to hold through volatility. Both HYPE and MORPHO clear that bar. Very few other altcoins do.

And they clear it in complementary ways. That’s what makes them work as a pair, not because they’re similar, but because they’re different.

Hyperliquid (HYPE): The Growth Position

By the numbers:

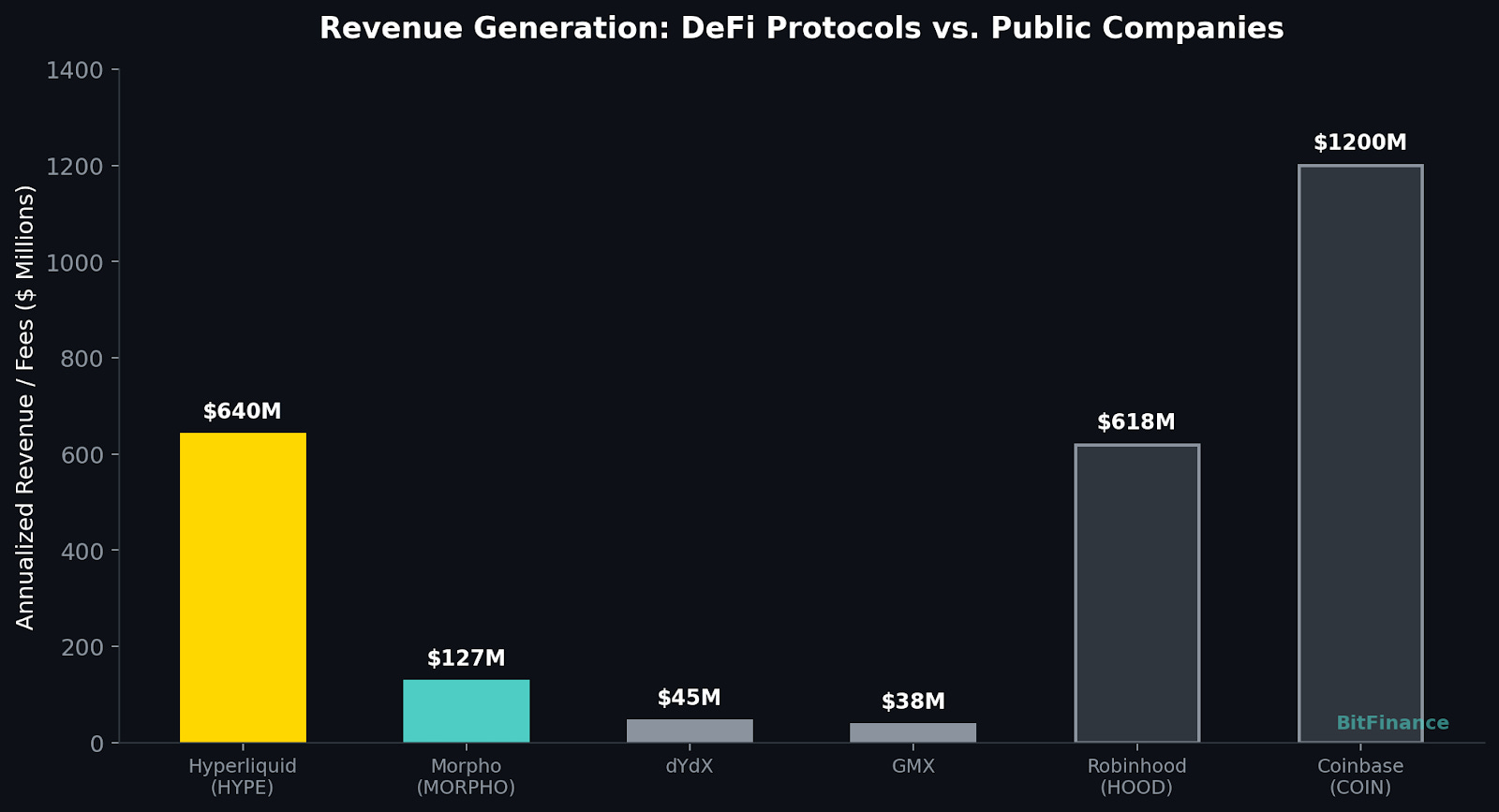

~$640M annualized fee run rate (Mar 2026). Up from ~$86M monthly in 2025.

70%+ of DeFi perpetuals market share.

$2.6T notional volume in March, surpassing Coinbase.

97% of all protocol fees flow to daily automatic HYPE buybacks (~$5M+/day)

Grayscale, Bitwise, and VanEck have all filed for spot HYPE ETFs.

TradFi assets (oil, gold, S&P 500 perps) now account for 30%+ of trading volume.

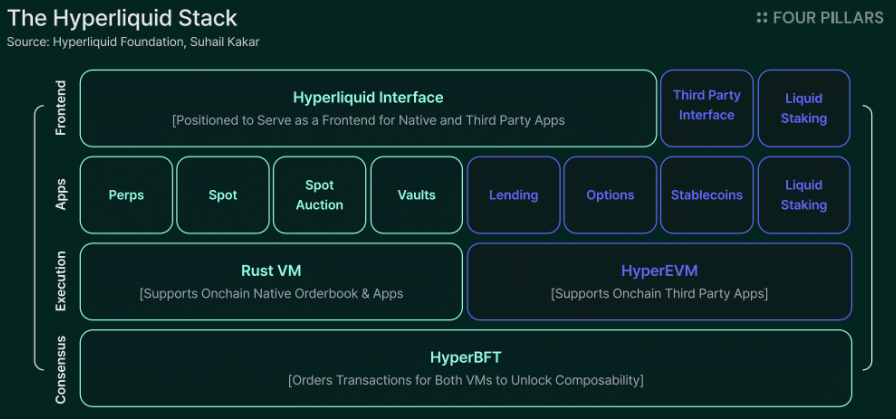

Hyperliquid is a custom-built Layer 1 blockchain designed for derivatives trading. It runs a fully onchain order book, handles over $8 billion in daily trading volume, and has quietly become the largest derivatives venue in crypto. Think of it as a decentralized CME that never closes, trades everything from Bitcoin to crude oil, and sends 97% of its revenue directly back to token holders.

The token IS the revenue model. 97% of every fee dollar the protocol earns ($640M annualized) is used to buy HYPE on the open market. Every day. Automatically. You’re not hoping the team decides to share revenue someday. The buyback is coded into the protocol. At current run rates, Hyperliquid repurchases roughly 7% of its own market cap annually. That’s not a narrative. That’s a cash register.

HYPE is the gas that runs the chain. Every trade, every smart contract, every new market that launches on HyperEVM requires HYPE to execute. As the platform expands into oil, gold, equities, and whatever comes next, demand for HYPE as fuel grows independently of the buyback. Two separate demand engines, one token.

That last part is the thesis. Every trade on Hyperliquid generates fees. Makers pay 0.01%, takers pay 0.035%. And 97% of those fees flow directly to the Assistance Fund, which uses them to buy HYPE tokens on the open market. Every single day. Automatically. No governance vote, no quarterly committee meeting, no human discretion. The protocol earns, the protocol buys.

At current volumes, the buyback runs north of $5 million daily. That’s roughly 7% of market cap annually being used to repurchase the token. For context, Ethereum’s EIP-1559 burn runs about 1.5%. BNB is around 1.2%. HYPE’s mechanism is four to five times more aggressive than either.

The growth vector is what makes this a growth position specifically. HIP-3, a permissionless market creation system, opened Hyperliquid to non-crypto assets. During the Iran conflict, crude oil perpetuals hit $1.7 billion in daily volume. JPMorgan wrote a research note about it. The S&P 500 perpetual hit $100 million in its first day. TradFi assets now represent over 30% of total volume. Every new market generates new fee revenue, which flows into buybacks regardless of whether the underlying is crypto. The addressable market just expanded from “crypto derivatives” to “all derivatives, 24/7.”

Three firms have filed for spot HYPE ETFs: Grayscale, Bitwise, and VanEck. Arthur Hayes publicly set a $150 price target. Whether those numbers are right or not, the institutional attention is a signal that serious people are paying attention to the economics.

The risks I’m watching:

Token supply is the biggest concern. Only about 33% of total supply is circulating. Core Contributors vest at roughly 1.2 million tokens per month over 24 months. The “Future Emissions and Community Rewards” bucket holds 38.9% of total supply with no defined release schedule. That’s a meaningful overhang that the buyback mechanism partially, but not fully, offsets.

Volume dependence is the structural risk. The flywheel is reflexive in both directions. More volume means more buybacks, more price support, more attention. Less volume means all of those in reverse. If the derivatives market contracts meaningfully, the thesis weakens. This is a business that needs traders to keep trading.

Security incidents have happened. The Jelly exploit raised questions about risk management. For an exchange handling billions in daily volume, operational security is existential, and the protocol’s track record isn’t spotless.

Regulatory risk is real but uncertain. A decentralized perps exchange offering commodities and equity exposure to anyone with a wallet sits in uncharted regulatory territory. If the CFTC decides permissionless oil perps need registration, the growth thesis changes.

Buffett Framework Question:

“Would I be comfortable if this token dropped 50% tomorrow and I couldn’t sell for a year?” For HYPE, my answer is yes, because the protocol would still be generating hundreds of millions in fees and buying the token every day. That’s the bar for a position I’m willing to hold through volatility.

Morpho (MORPHO): The Infrastructure Position

By the numbers:

~$127M annualized protocol fees. Curator fees grew 600% in 2025 ($2M to $13M annualized).

$5.8B TVL. 1.4 million users. Second-largest DeFi lending protocol.

Coinbase crypto-backed loans powered by Morpho: $960M active loans, $1.7B collateral.

Apollo Global Management ($940B AUM) acquiring up to 9% of MORPHO supply over 48 months.

Ethereum Foundation deployed $19M into Morpho vaults in March 2026.

Also integrated by Kraken, Gemini, Bitpanda, Ledger, Trust Wallet, Safe, and World.

If HYPE is the growth play, Morpho is the picks-and-shovels play. It’s the lending infrastructure that the biggest names in crypto and TradFi are building on top of, often without their end users ever knowing it exists.

The token governs the toll booth. Every Coinbase crypto loan, every Kraken DeFi Earn deposit, every dollar Apollo routes into onchain credit flows through Morpho’s immutable contracts. The MORPHO token controls the parameters of that infrastructure: fee structures, treasury deployment, protocol upgrades. As more capital flows through the toll booth, what the token governs becomes more valuable. You’re buying governance power over $5.8 billion in infrastructure that institutions are actively building on top of.

The GENIUS Act made Morpho structurally necessary. Stablecoin issuers can’t pay yield directly to holders. That means trillions in stablecoins need somewhere to earn. Vaults built on Morpho are the destination. The token doesn’t just govern today’s $127M in fees. It governs the protocol positioned to capture yield demand from an entire asset class that didn’t exist at this scale two years ago.

When someone takes out a crypto-backed loan on Coinbase, Morpho powers the transaction. When Kraken’s DeFi Earn product routes deposits into onchain yield, those deposits land in Morpho vaults. When Ledger or Trust Wallet offers an “earn” feature, it’s often Morpho underneath. The protocol has 1.4 million users, and most of them have never heard of Morpho. That’s the business model: be the invisible infrastructure layer that every fintech plugs into.

This is why I call it an infrastructure position. You’re not betting on Morpho winning the lending market the way you’d bet on one exchange beating another. You’re betting that onchain lending becomes core financial plumbing, and that Morpho’s modular architecture and network of integrations make it the default protocol that everyone builds on. It’s the AWS thesis applied to DeFi.

The GENIUS Act creates a structural tailwind that most people haven’t connected yet. The law bars stablecoin issuers from paying yield directly to holders. That means trillions in stablecoins coming onchain will need to find yield somewhere. Vaults built on Morpho are the natural destination. The protocol is positioned to be the savings account layer for the entire stablecoin economy.

Apollo’s commitment is worth emphasizing. A $940 billion traditional asset manager acquiring 9% of a DeFi protocol’s token supply over four years isn’t an experiment. It’s a strategic infrastructure bet. Apollo intends to leverage Morpho’s modular markets for real-world asset lending, connecting their private credit expertise with onchain distribution. The Ethereum Foundation’s repeated deposits add credibility from the technical side. When both Wall Street and the blockchain’s governing body are deploying capital into the same protocol, that’s a signal.

Morpho V2, launching in 2026, brings market-driven rates, fixed-rate/fixed-term lending, and compliance gating. These are features designed specifically for institutional users who need the lending experience to feel familiar. It’s the protocol growing into its institutional ambitions.

The risks I’m watching:

Value accrual to the token is the primary concern. Unlike HYPE’s direct buyback, MORPHO’s revenue path to the token is indirect. Fees flow to curators (who take performance fees) and to the DAO treasury (governed by token holders). There’s no automatic buyback mechanism. You’re investing in governance power over a growing ecosystem, not direct revenue participation. That’s a weaker short-term price catalyst, though the long-term thesis is sound if the ecosystem keeps growing.

The unlock schedule is complex. The DAO holds 35.4% of all tokens and can deploy them via governance vote. Strategic partners, founders, and contributors hold additional locked allocations vesting through 2029. About 36% is currently circulating. The saving grace is Apollo’s systematic buying, which creates structured demand that can absorb selling pressure.

Curator concentration is an emerging risk. Research shows that a small set of curators manages a disproportionate share of TVL and exhibits clustered tail co-movement. The vault ecosystem is more concentrated than it looks, and problems at one major curator could ripple across the system.

Smart contract risk is always present. Morpho has tier-1 audits and a $2.5M bug bounty, but billions in TVL make it a target. The protocol is immutable and non-custodial, which means there’s no centralized “break glass” option if something goes wrong at the base layer.

Buffett Framework Question:

“Is this business more valuable in five years than it is today?” For Morpho, I believe the answer is yes. The stablecoin economy is growing. The vault infrastructure is being adopted by every major exchange. The regulatory environment is becoming more favorable. Those are structural tailwinds, not narrative momentum. That’s what makes it a position I’m comfortable sizing as a longer-duration hold.

Why They Belong Together

I’m holding both because they’re complementary, not redundant. They sit in different parts of the digital asset stack and carry different risk profiles.

HYPE is correlated to trading activity and an active user base is exactly what you want to be looking out for. When markets are active, the protocol earns more, buys more tokens, and the flywheel accelerates. It performs best in environments where people are trading. That’s a growth-oriented position with higher upside and higher volatility.

MORPHO is correlated to capital deployment. When stablecoins need yield, when exchanges need lending infrastructure, when institutions need onchain credit markets, Morpho benefits. It performs best in environments where capital is looking for a home. That’s a more durable position with steadier adoption drivers but less explosive upside.

")

Active trading environments and capital deployment environments don’t always overlap perfectly. A bear market for token prices can still be a growth environment for lending infrastructure (because capital still needs yield). A volatile trading environment drives HYPE’s revenue even when broader sentiment is negative. Holding both means I’m exposed to digital asset infrastructure growth regardless of which specific narrative is driving the market at any given moment.

That’s diversification within the altcoin bucket. Not diversification by owning ten different tokens you don’t understand. Diversification by owning two businesses with different revenue drivers, different risk profiles, and different catalysts.

Portfolio Sizing: How Much and Why

I use a three-bucket framework for digital asset allocation.

Bucket 1 is Bitcoin: store of value, foundation layer, the largest allocation.

Bucket 2 is stablecoins + yield: dry powder, vault deposits, steady income.

Bucket 3 is infrastructure and venture-style bets: revenue-generating protocols where I have high conviction in the business model.

HYPE and MORPHO collectively sit at about 10 to 15% of my overall portfolio. That’s Bucket 3. The rest is Bitcoin, stablecoins, and traditional assets. That balance is the whole point.

I’m saying this because sizing matters more than conviction. I’ve seen too many people put 50% of their portfolio into their best idea and then panic-sell when it draws down 40%, which in crypto happens regularly. The position has to be large enough to matter if you’re right and small enough to survive if you’re wrong. For me, 10 to 15% is that number.

If HYPE goes to zero, I take a hit but I’m fine. If MORPHO goes to zero, same. If both double, the portfolio benefits meaningfully. That asymmetry only works at the right size. It doesn’t work at 50%.

Moving right along…

This Week In 2 Mins

I’ve Been Building with AI Tools for 3 Months; Here Are My Biggest Mistakes

(March 24)

Five lessons from building an autonomous trading system that apply to anyone using AI professionally. Stack fewer tools, not more.

Let the AI tell you when to stop and go learn the domain yourself. Stress test everything before you trust it. Build in public because the accountability and feedback loops are worth more than the polish. And the biggest mistake of all was waiting to start.

The Biggest Crypto Conference in America Had One Problem. Nobody Talked About Crypto (March 27)

I spent three days at the Digital Asset Summit in New York.

Across 20+ meetings with custodians, infrastructure providers, and policy advocates, nobody was talking about altcoins or speculation. The institutional conversation has consolidated around three pillars:

Bitcoin as store of value

Stablecoins as settlement infrastructure

Tokenization as the mechanism for bringing traditional assets onchain.

The regulatory window is real but time-limited. Visa joined the Canton Network. Franklin Templeton partnered with Ondo. Fidelity presented blockchain as a plumbing upgrade, not a technology bet. If you’re still framing digital assets as a bet on token prices, you’re having last cycle’s conversation.

WINNERS 🏆

Gold. Rebounded sharply mid-week after its worst selloff since 2013, climbing from $4,098 back above $4,490. Geopolitical uncertainty and safe-haven flows continue to drive demand despite elevated real yields. Still down from the January all-time high of $5,595, but the recovery from Tuesday’s lows was one of the sharpest single-day moves in recent memory.

Oil / Energy Producers. Brent crude pushed above $105 mid-week as the Iran conflict and Strait of Hormuz disruption kept supply fears elevated. Macquarie revised WTI forecasts to $83/barrel average for 2026, up from $58. Energy stocks and shipping names benefited from the supply squeeze, with tanker rates and marine insurance premiums both climbing.

Clear Secure (YOU). Up 20%+ over two weeks as TSA lines lengthened during the partial government shutdown. App downloads tripled year-over-year in March. DA Davidson raised its price target to $65, citing the World Cup tailwind for air travel later this year. A textbook example of a company benefiting from someone else’s problem.

Kraft Heinz / Consumer Defensives. Unlikely leaders in a fear-driven market. Kraft Heinz topped the Nasdaq 100 on multiple days this week as investors rotated into defensive names. When a food company is leading a tech index, the risk-off signal is loud.

LOSERS 📉

Bitcoin. Fell from ~$71K to ~$66K over the course of the week, a roughly 7% decline. Fear & Greed Index hit 11, its lowest reading of 2026. Now down ~48% from the late 2025 peak of $126K. Six consecutive months of negative or flat returns, the longest streak since 2022. Whale accumulation is happening, but price action hasn’t followed yet.

Micron Technology (MU). Down 22% in six sessions after reporting blowout earnings, then guiding to capex far above expectations. Alphabet’s TurboQuant AI compression algorithm announcement added pressure on memory names. BTIG noted this was Micron’s steepest post-high decline since 1999. When good earnings get sold, pay attention.

Altcoins Broadly. Ethereum dropped ~7.5% on the week to $1,985. Solana, Cardano, and most alts tracked lower. Bitcoin dominance held near 58%, confirming that capital is consolidating into BTC while everything else bleeds. Trust Wallet Token and Worldcoin were among the worst individual performers, down 11% and 12% respectively.

Nutrien (NTR). Despite surging fertilizer prices from the Iran conflict, UBS downgraded to sell, arguing the 46% rally over the past year already priced in the supply disruption. A reminder that being right on the macro thesis doesn’t help if the trade is already crowded.

ON DECK: 3 THINGS TO WATCH NEXT WEEK

FTX $2.2B Creditor Distribution (March 31) — The fourth major payout from the FTX Recovery Trust hits Monday. Total repayments now approach $10B. The question for markets: does this cash re-enter crypto (former users buying back in) or exit permanently? At extreme fear sentiment levels, even a partial re-deployment into BTC could move the needle. Watch spot ETF inflow data in the days following.

Trump’s Iran Deadline Extension (April 6) — Trump extended his deadline for Iran to reopen the Strait of Hormuz to April 6, saying negotiations are “going very well.” If that deadline passes without resolution, the threatened strike on Iran’s energy infrastructure comes back on the table. Oil, gold, defense stocks, and risk assets broadly will key off every headline. This is the single biggest macro variable right now.

Q1 Quarter-End Rebalancing — Institutional fund managers will be adjusting equity and alternative asset allocations ahead of the March 31 quarter-end. After a brutal Q1 for both equities and crypto, rebalancing flows could create unusual volume in both directions. Monthly options expiry adds another layer of positioning risk. Don’t mistake mechanical flows for conviction.

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.