Coinbase Made an AI Your Fiduciary. Read the Fine Print.

On Tuesday, Coinbase shipped 21 products in a single event.

Bitcoin-backed mortgages accepted by Fannie Mae.

Tokenized stocks.

Options on crypto and equities.

Pre-IPO futures on companies like SpaceX.

A merger of its U.S. and international exchanges.

Most of it is volume, the kind of release calendar built to look like momentum.

But one product launch hit me like a lightning bolt: Coinbase registered an AI agent with the SEC, the CFTC, and the NFA as an investment adviser.

It’s not a chatbot that floats ideas and tells you to do your own research, but a registered adviser that reads your full account history, runs around the clock, and tells you what to buy and what to sell.

I hold a Series 65. That license exists for a reason. Giving investment advice for compensation is supposed to carry a legal standard of care, attached to a person a regulator can examine, sanction, and hold responsible.

Coinbase just attached that standard to software. Read it one way, it’s a real shift in how retail investors get advice. Read it another, it’s a lawsuit that hasn’t been filed yet.

My read is that it’s both, and the gap between those two readings is the story.

What It Does

Coinbase Advisor is live now for U.S. Coinbase One subscribers.

It has your full portfolio context.

It designs tax-loss harvesting strategies.

It turns breaking news into multi-asset trade recommendations.

It issues explicit buy and sell calls instead of vague suggestions.

Coinbase’s head of consumer products drew the contrast with ordinary chatbots on purpose, describing it as financial advice that will tell you what to sell and what to buy.

For a self-directed investor who was never going to open a relationship with a human adviser, this is a step up from the robo tier. The tax-loss harvesting alone carries dollar value. Around-the-clock analysis across a full account is something most retail investors have never had.

So far it sounds like a win…then you read the disclosures.

The Catch is in the Disclaimers

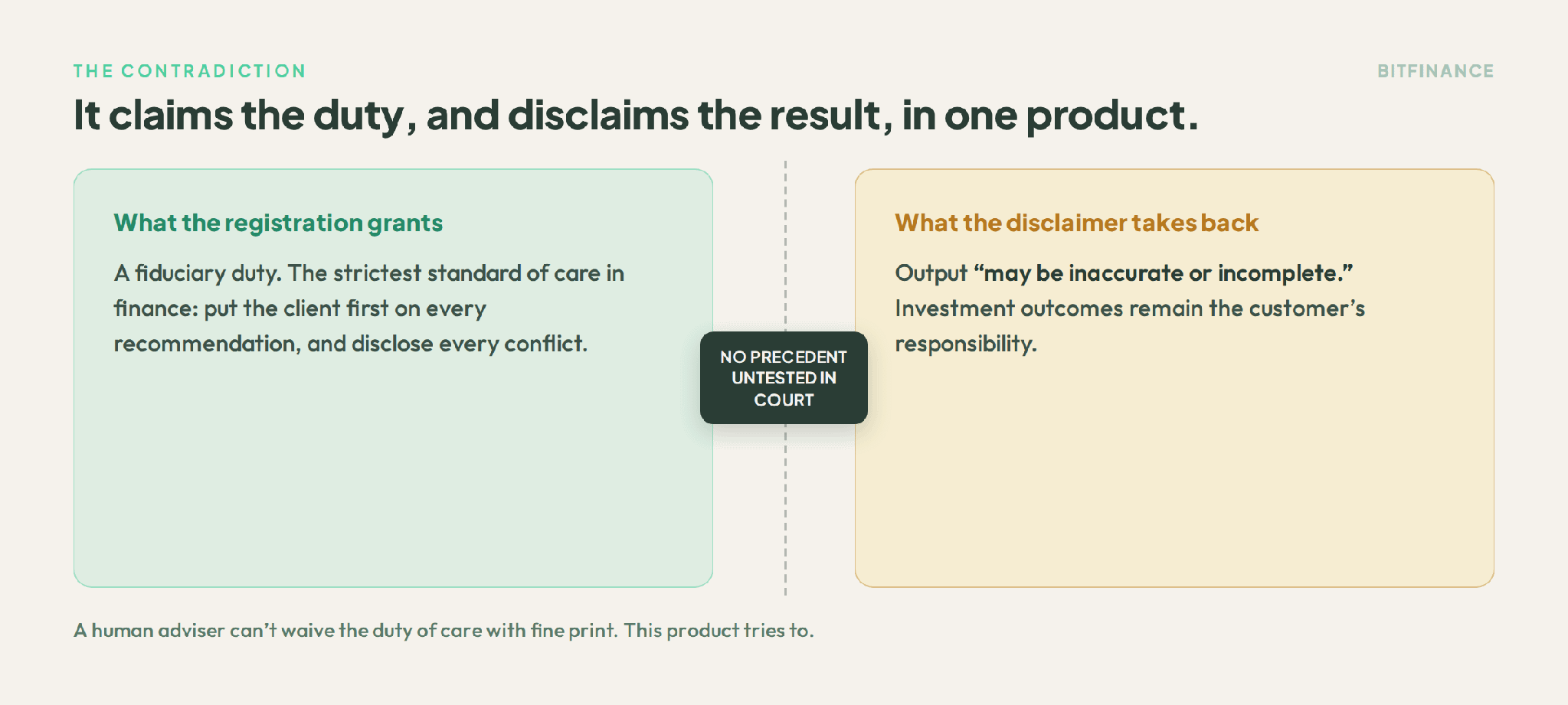

A Registered Investment Adviser is a fiduciary.

Under the Investment Advisers Act of 1940, any fiduciary has to put your interests ahead of its own, disclose its conflicts, and apply a duty of care to every recommendation.

That standard sits above the suitability bar brokers work under, and you can’t waive it with fine print. A human adviser who told clients “my advice might be wrong and you eat all the losses” would be answering to regulators by lunch.

Coinbase’s own disclosures say the advisor’s output “may be inaccurate or incomplete,” and that the outcomes are your responsibility. The platform claims the fiduciary standard and disclaims the result of meeting it, in the same product.

That combination has NO precedent in securities law, and NO court has tested it for an AI-driven adviser. (I’m getting the popcorn ready for the pending lawsuits.🍿)

The approval step doesn’t close the gap. The agent needs your sign-off before it trades, but that’s a confirmation click, not an independent judgment about whether the advice met a fiduciary standard in your situation.

FINRA’s 2026 oversight report named autonomous AI agents running without a human in the loop as a top investor risk, warning that a misaligned reward function could push an agent toward decisions that work against the investor. 😬

The volume changes the stakes too.

By one estimate from Citizens, an AI agent can trade 10 to 20 times more actively than a typical retail investor does on their own. A single confirmation click ends up governing a system that may touch your account far more often than you ever would.

Critics at rival firms put it plainer: the investor carries the risk and is the one on the hook when the agent gets it wrong.

This is the same problem I wrote about after the Aave disaster a few months back. The technology can perform exactly as designed and you can still be left with no one to call. Then the missing party was a custodian or an insurer. Here it’s the adviser itself, present in name and registration, absent in accountability.

Buffett Framework Question

“If this advice blows up my account tomorrow, who is legally on the hook, and can a fiduciary disclaim the outcome of its own advice?”

If the answer is a confirmation screen and a paragraph of fine print, the registration is real but the recourse is theoretical, and your position sizing should reflect the difference.

Who This is For

Strip away the headline and the answer gets clearer. This is built for the Coinbase One user who is already self-directed and doesn’t have an adviser. It’s a smarter robo, a better version of tools that customer already uses. It isn’t a substitute for the relationship a household with real complexity keeps with a human planner who coordinates taxes across accounts, handles estate questions, and talks them out of selling the bottom in a panic.

If you already pay an adviser worth paying, this doesn’t replace that person. If you don’t, it’s a real step up from trading on gut and group chats, as long as you understand that the accountability you’d assume comes with the word fiduciary is the one thing the disclaimer takes back.

Two Roads at One Fork

The timing is what makes this sharp. Two weeks ago, Robinhood faced the same decision and went the other way.

At its SYNERGY26 event, Robinhood rolled out an Advisor Network that matches its retail users with vetted human RIAs, plus Cortex for Advisors, an AI tool that writes portfolio digests, surfaces tax insights, and preps human advisers for client meetings.

The tell is what Robinhood’s own executives said: regulatory constraints still keep AI from directly managing client assets, so they built AI to make the human adviser faster and routed complex clients to a person.

Same month, same retail-first ambition, opposite bets.

Coinbase made the AI the fiduciary.

Robinhood made the AI serve the fiduciary and kept a human on the hook.

One of these firms is reading the regulatory road differently than the other, and within a year or two we’ll know which one read it right.

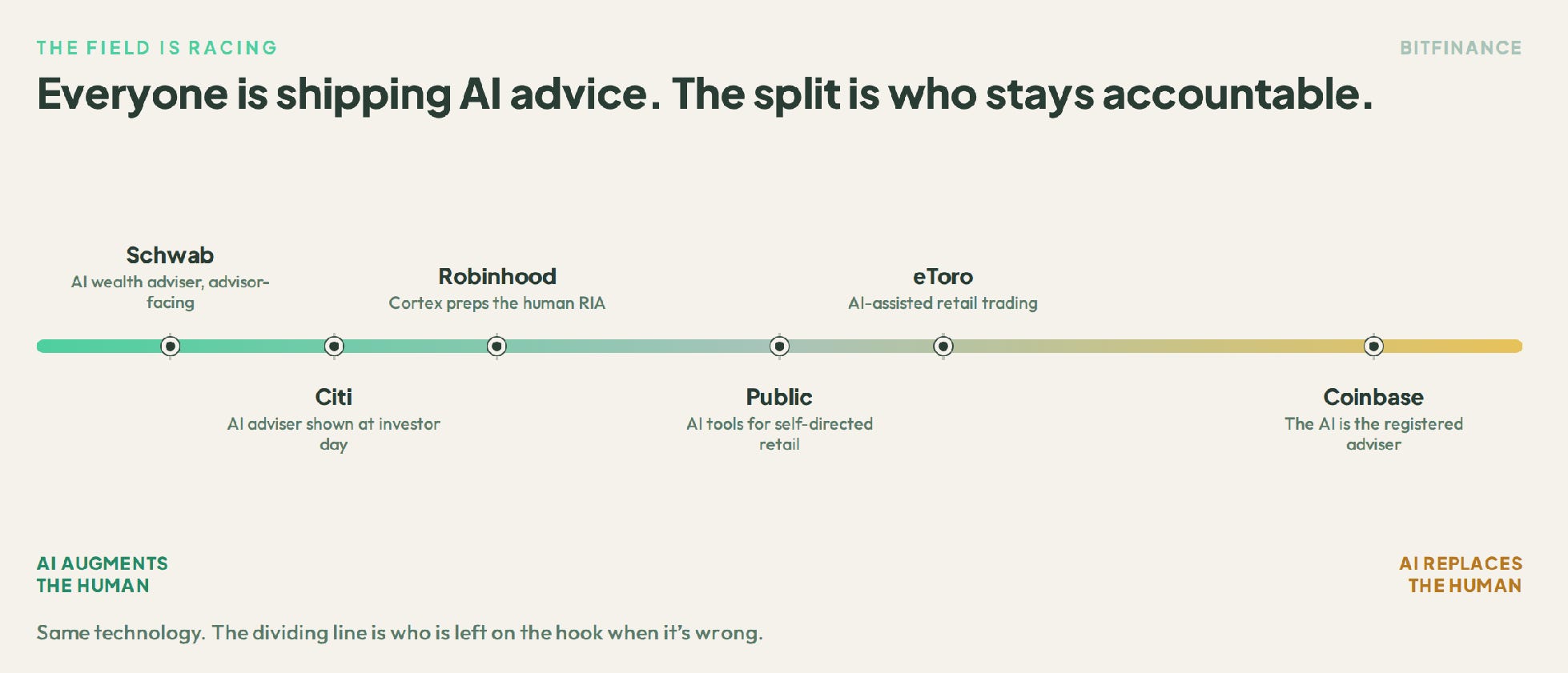

Coinbase and Robinhood aren’t the only two on the field.

Schwab and Citi both showed AI-powered wealth advisers at recent investor days, and eToro and Public have pushed AI trading tools to retail.

Line them all up and they sort along one axis: AI that augments a human at one end, AI that replaces one at the other. Coinbase planted its flag at the far end.

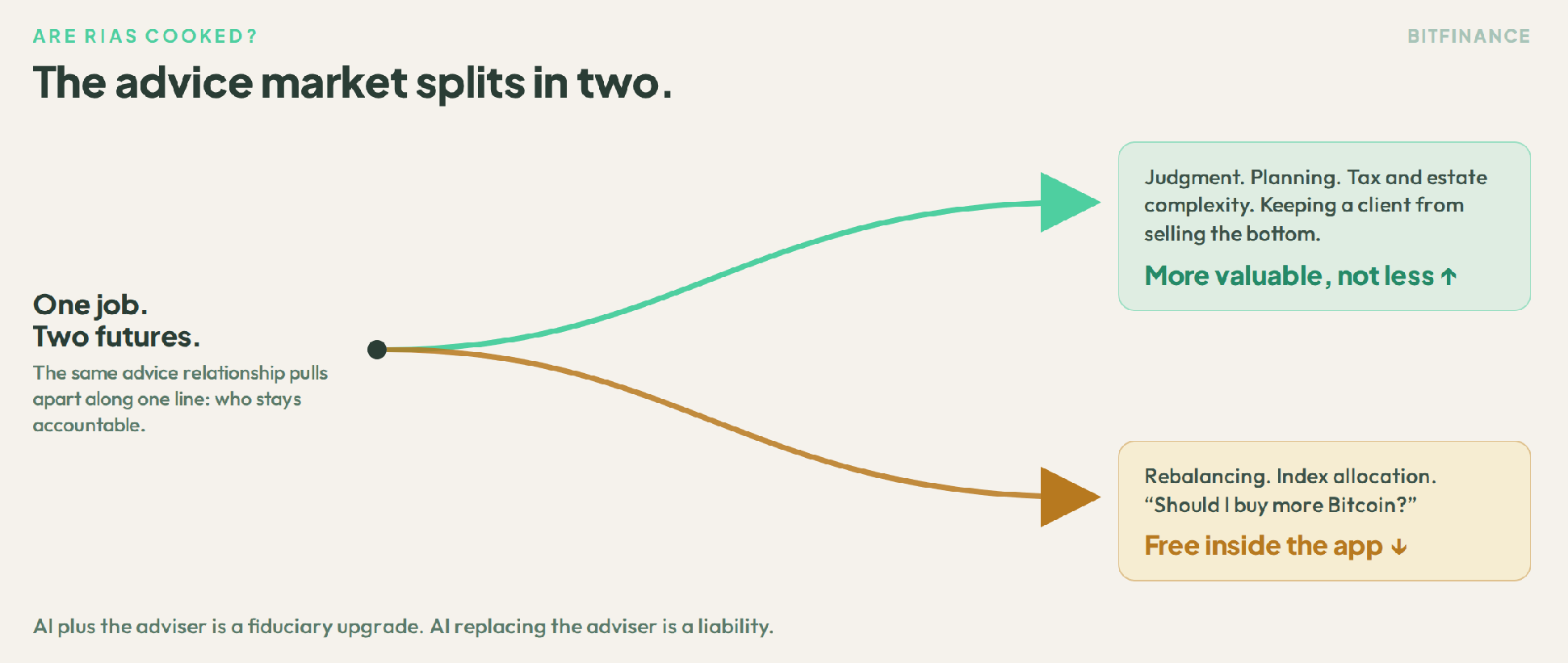

Are RIAs Cooked?

Short version: the commodity tier is, the judgment tier isn’t, and the gap between them is about to widen.

If your value to a client is rebalancing a portfolio and answering “should I buy more Bitcoin,” that work is now free inside an app, and it’s competent. An adviser charging one percent for index allocation and a quarterly check-in should feel the floor moving.

If, however, your value is judgment, planning, tax and estate complexity, and being the person who keeps a client from doing something stupid in a drawdown, you got more valuable, not less.

There’s now a confident machine telling millions of retail investors what to trade, with no one accountable for the result. The market for a human who is accountable doesn’t shrink in that world. It grows.

I walked an AI pavilion at FutureProof Miami earlier this year and left with one framing that holds up here. AI plus the adviser is a fiduciary upgrade. AI replacing the adviser is a liability. Coinbase just ran the second experiment in public, with a disclaimer attached that makes the point for me.

This is also why credentialing keeps mattering in a way the alarmist version of this story misses. A license is a person a regulator can hold responsible, a fiduciary who can’t disclaim the duty of care. Coinbase Advisor carries the registration and offloads the outcome. Those aren’t the same product, and the difference is the part that outlasts the hype cycle. The data backs the point. In CoinShares’ survey of financial advisers, 62 percent said recommending Bitcoin didn’t square with their fiduciary duty. The fiduciary question was already the hard part of this conversation, and automating the advice doesn’t soften it. It sharpens it.

The Other Half of the Stack

Coinbase didn’t only ship the advice layer. It also formalized Coinbase for Agents, which lets outside agents like ChatGPT and Claude act inside your account within limits you set, and settles their machine-to-machine payments over x402.

If that protocol sounds familiar, it should. x402 is the rail I covered in the first issue of the Agentic Finance series, the HTTP 402 revival that lets software pay software in stablecoins for fractions of a cent.

Put the two launches side by side and the shape is clear.

Coinbase Advisor is the brain that decides.

Coinbase for Agents and x402 are the hands and the wallet that act and pay.

That’s less a product than an attempt to own the whole agentic-finance stack, advice through settlement, inside one app.

The payments half is further along than most people realize. The x402 rail has already cleared more than 119 million transactions on Base and another 35 million on Solana, running near $600 million annualized as of March.

Where I Could Be Wrong

The bear case on my own take is simple.

Maybe the disclaimer holds up fine, the SEC signals it’s comfortable, and a registered AI adviser becomes the default retail tier within two years, the way robo-advisers normalized a decade ago. In that world I’m overweighting a legal tension the market just prices through.

It could cut the other way too. The first real loss that reaches a regulator or a judge could define AI fiduciary duty narrowly and fast, and freeze the category before it scales. I don’t know which happens. I know the unresolved question now sits inside a product that millions of people can use, and that’s usually how these things get settled, one painful case at a time.

This genie isn’t going back in the lamp, and it shouldn’t. Agents will keep turning up across our financial lives, each one promising to make something easier, and plenty of them will. The question that follows every one of them is the one Coinbase just stopped letting us avoid: when the easy answer is wrong, who’s still on the hook?

The Watchlist

COIN. The pure-play on the bet that crypto rails become the connective tissue of agentic finance. Watch adoption and the disclosure language, not just the stock.

HOOD. The human-in-the-loop counter-bet. If advised assets and the Advisor Network grow fast, the conservative read on regulation was the right one.

The first AI-adviser liability case. Whenever it lands, it sets the terms for the whole category. Worth watching closer than any single product launch.

SEC guidance on AI fiduciary duty. Any signal on whether a registered AI adviser can disclaim outcomes moves the entire field at once.

x402 and Coinbase for Agents adoption. The payments layer is the leading indicator here. Watch transaction volume and which platforms wire in.

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.