Buffett's Favorite Business Is Coming On-Chain

In 1967, Warren Buffett bought a small Omaha insurer called National Indemnity for $8.6 million. It turned out to be the most important purchase of his career, and the reason has nothing to do with insurance being exciting.

The reason is float.

Here’s the simplest way to understand it. Imagine a coffee shop that sells gift cards. Customers hand over cash today and redeem it for lattes over the next year or two. In the meantime, the shop holds a pile of money that technically belongs to its customers but sits in the shop’s bank account, available to use. Now imagine the shop is allowed to invest that pile while it waits.

That’s an insurance company.

It collects premiums today and pays claims later, sometimes years later. In between, it holds money it doesn’t own but gets to invest. Buffett has described float in his shareholder letters as money Berkshire holds but that doesn’t belong to it.

Berkshire’s float grew from $39 million in 1970 to $176 billion at the end of 2025.

Five decades of other people’s money, compounding for Berkshire’s benefit. Note the log scale; on a normal chart, the first four decades would be invisible.

Now the part that turns trivia into a lesson.

If an insurer underwrites with discipline, meaning the premiums it collects exceed the claims it pays plus expenses, the float costs less than nothing. Berkshire got paid to hold other people’s money, then compounded it for half a century. That engine, more than any single stock pick, built the capital stack under Berkshire Hathaway.

Buffett’s edge wasn’t just picking investments. It was owning the machine that funded them.

You’ve likely only sat on one side of this trade

Think about every insurance transaction in your life.

Car, renters, health, phone screen. You were the buyer every single time. Buying insurance means paying someone to absorb your worst-case scenario, and it’s usually money well spent.

Selling insurance is the other seat at the table, the one where premiums flow toward you. That seat has been roped off for a century: Berkshire, Lloyd’s of London syndicates, giant reinsurers, and more recently catastrophe bond funds with institutional minimums.

The economics were real, since reinsurance alone is roughly a $750 billion global market, but the door was closed to individuals.

Quick vocabulary stop, because one term does a lot of work here: Reinsurance is insurance for insurance companies.

When a Florida insurer worries that one monster hurricane could bankrupt it, it buys its own policy from a reinsurer, passing along part of the risk and part of the premium. Reinsurers sit at the top of the risk food chain, which is exactly where Buffett went when he bought General Re in 1998.

Tokenization is now opening that roped-off seat. What follows is a map of the ecosystem, offered for education rather than endorsement.

Four doors into the seller’s seat

Let’s look at a few examples in the digital asset space who have been operating in the insurance/reinsurance business to see how the logistics play out:

Re runs Cover Re, a fully collateralized Cayman reinsurer with $409 million in premiums written since inception. Its two tokens are a teaching diagram: reUSD sits senior and principal-protected, while reUSDe sits junior and absorbs real underwriting results. Losses hit the reinsurer’s own equity first, then reUSDe, then reUSD.

Think of it as standing in line for losses. The further back you stand, the safer you are and the less you get paid. Wall Street calls these positions tranches and dresses them in Latin, but the line is the whole concept. Two footnotes: reUSD is open to non-U.S. investors only, and the RE governance token launching separately carries voting rights rather than insurance economics, which makes it a different bet entirely.

Nayms, now OnRe, runs a Bermuda-regulated marketplace whose signature early product was the tokenized industry loss warranty, a contract that pays on the industry’s total bill from a storm rather than one company’s paperwork. Its Florida windstorm version triggered only if two separate storms each caused $10 billion in damage, with USDC collateral locked in an audited Ethereum contract. As OnRe, its ONyc token now stacks reinsurance premiums on top of stablecoin yield for low-double-digit base returns, with partners including Solana, Ethena, and Coinbase Prime. Bermuda’s regulator is building a formal framework for tokenized insurance assets, which is why the serious players keep domiciling there.

Oxbridge Re is a Nasdaq-listed Cayman reinsurer whose SurancePlus tokens are SEC 506(c) private placements open to U.S. accredited investors with $5,000 minimums. They fund reinsurance for Gulf Coast property insurers, which is a polite way of saying you’re selling hurricane insurance. (Interesting 3-month chart here…)

Nexus Mutual covers a peril that didn’t exist twenty years ago: smart contract failure. Its NXM token breaks the usual crypto mold, since only KYC’d members can hold it, its value tracks the mutual’s actual capital pool, and staking it into coverage pools is how you take underwriting risk. Owning NXM is closer to being a Lloyd’s name than holding a governance token; it’s membership in the risk pool, losses included. This is the most crypto-native door of the four, and the one where a DeFi-literate reader may genuinely know more than the traditional underwriter.

The warning has a name, and it’s Milton

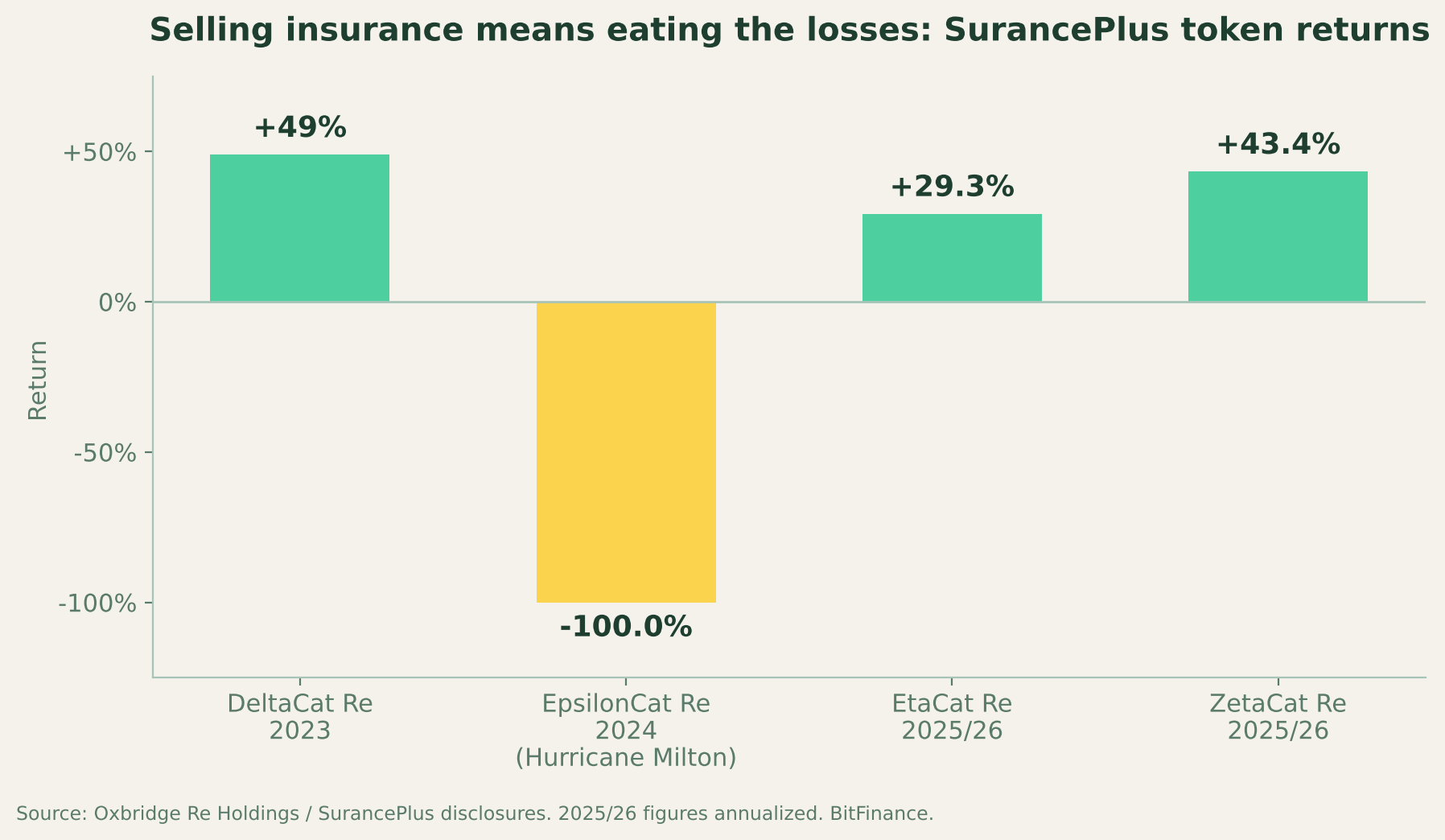

Oxbridge’s track record is the most useful education in this entire article, precisely because it includes a disaster.

Its 2023 token, DeltaCat Re, returned 49%. Its 2024 token, EpsilonCat Re, took a full limit loss when Hurricane Milton hit, wiping out $2.3 million of the $2.88 million investors put in. 😬

The 2025/26 vintages then delivered 29.3% and 43.4% annualized.

Win, total loss, win. The gold bar is the tuition. This sequence is what selling insurance means, compressed into three years.

The premium is compensation for the years the hurricane comes.

Berkshire’s insurance operations succeed because of underwriting discipline sustained across decades, and anyone taking the seller’s seat inherits the same requirement in miniature. Some newer tokenized offerings now target triple-digit returns “assuming no underwriting losses.” Read that qualifier twice. Returns that high are the market telling you total loss is a live scenario rather than a footnote.

Circle of competence applies with full force. If you understand smart contract risk, Nexus Mutual’s coverage book may be genuinely legible to you. If you can’t explain what a Gulf Coast excess-of-loss treaty pays out on, you’re not underwriting. You’re guessing with extra steps.

If you can’t explain what you’re insuring, you’re not selling insurance. You’re selling lottery tickets to yourself.

Buffett Framework Question

Would Buffett buy the float or the token? The float, every time. He’d want the underwriting economics, the collateral quality, and the claims history, and he’d have no use for a token whose value depends on someone else wanting it later. Notice which token passes that test: NXM works precisely because it’s a claim on a capital pool and its underwriting results, rather than an emblem. The lesson travels well: in tokenized insurance, own the economics, not the emblem.

The straight assessment

Selling insurance rewarded Berkshire because bad things usually don’t happen, and disciplined sellers get paid in all the years they don’t. That logic is now available in fractional, on-chain form, which is a genuine expansion of what individual investors can access.

The discipline doesn’t come included, though. These products carry real total-loss risk, uneven regulatory footing across jurisdictions, smart contract risk layered on top of underwriting risk, and in several cases accreditation or residency gates. Buffett spent sixty years proving the model works with patient capital and ruthless underwriting standards.

The tools are newly democratic. The standards never were.

Until next time fam!

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.

Sources

Berkshire Hathaway shareholder letters, insurance float figures, 1970 to 2024.

Insurance Business Magazine, “Resilience Foundation prepares launch of RE Governance Token,” May 27, 2026.

Re Protocol documentation, docs.re.xyz, “Introduction to the Re Protocol.”

RWA.xyz, reUSD asset profile (investor eligibility and market data).

Artemis.bm, “Oxbridge Re unveils new tokenized reinsurance sidecar securities with 20% and 42% return targets,” February 11, 2026.

Insurance Business Magazine, “Oxbridge Re swings to Q1 profit on tokenized reinsurance pivot,” May 12, 2026.

Oxbridge Re Holdings press release, “SurancePlus Exceeds Return Targets, Delivering 29.3% and 43.4% Annualized Returns,” June 17, 2026.

Reinsurance News, “Oxbridge Re’s SurancePlus to launch tokenised reinsurance securities on Solana with HCI Group’s Fortex Re program,” June 2026.

Captive.com, “A New Tokenized Reinsurance Blockchain Arrangement Launches” (Nayms tokenized industry loss warranties).

DeFi Coverage, “How Tokenized Reinsurance Protocols Bring Real-World Insurance Yields to DeFi Users” (OnRe, Ethena partnership), October 2025.

Insurance Business Magazine, “Blockchain reinsurance platform Re boosts capacity for 2026 renewals” (Bermuda regulatory framework), November 2025.

Nexus Mutual documentation, NXM tokenomics and membership requirements.