BlackRock’s new Bitcoin Income ETF Sells the Only Days That Matter

Strip Bitcoin’s 10 best days out of each year,

and a +90% asset turns into a -25% one.

That single line is most of what you need to know, because BlackRock just launched a fund whose design, in effect, sells those days.

Studying for the Series 7 has me living inside options theory lately, which I enjoy as a self-professed finance nerd. That’s what pulled me into the mechanics of BITA, BlackRock’s new Bitcoin Premium Income ETF, which started trading on June 16.

I've helped build and run hedge funds designed to put idle crypto to work generating income - funded by hundreds of millions in member contributions in kind - and we steered clear of the covered-call approach every time for some very important reasons.

What follows is why.

How a fund like this actually works

Bitcoin pays no dividend and throws off no cash.

A holder sitting on a large position naturally wants it to produce something, and with more than a trillion dollars of Bitcoin sitting idle, the pitch writes itself: keep your coins, collect a yield.

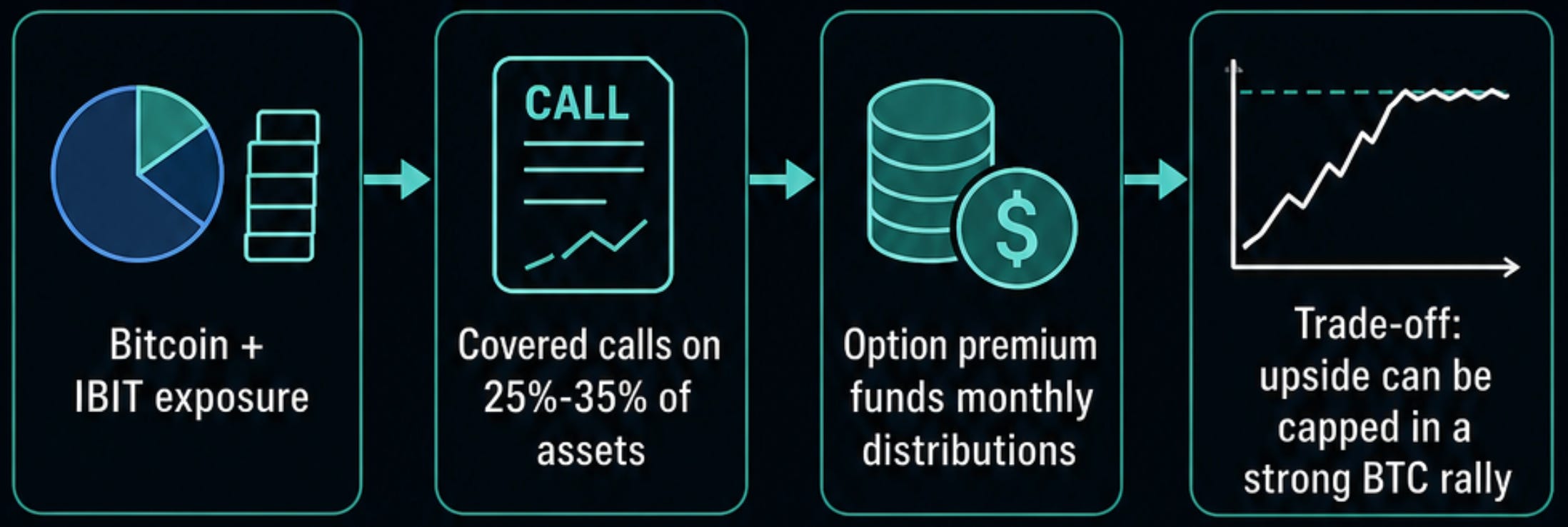

BITA answers that wish. It owns Bitcoin, mostly through spot and BlackRock’s own IBIT fund, and it targets a 15 to 25% annual yield while claiming to preserve about 70% of Bitcoin’s upside.

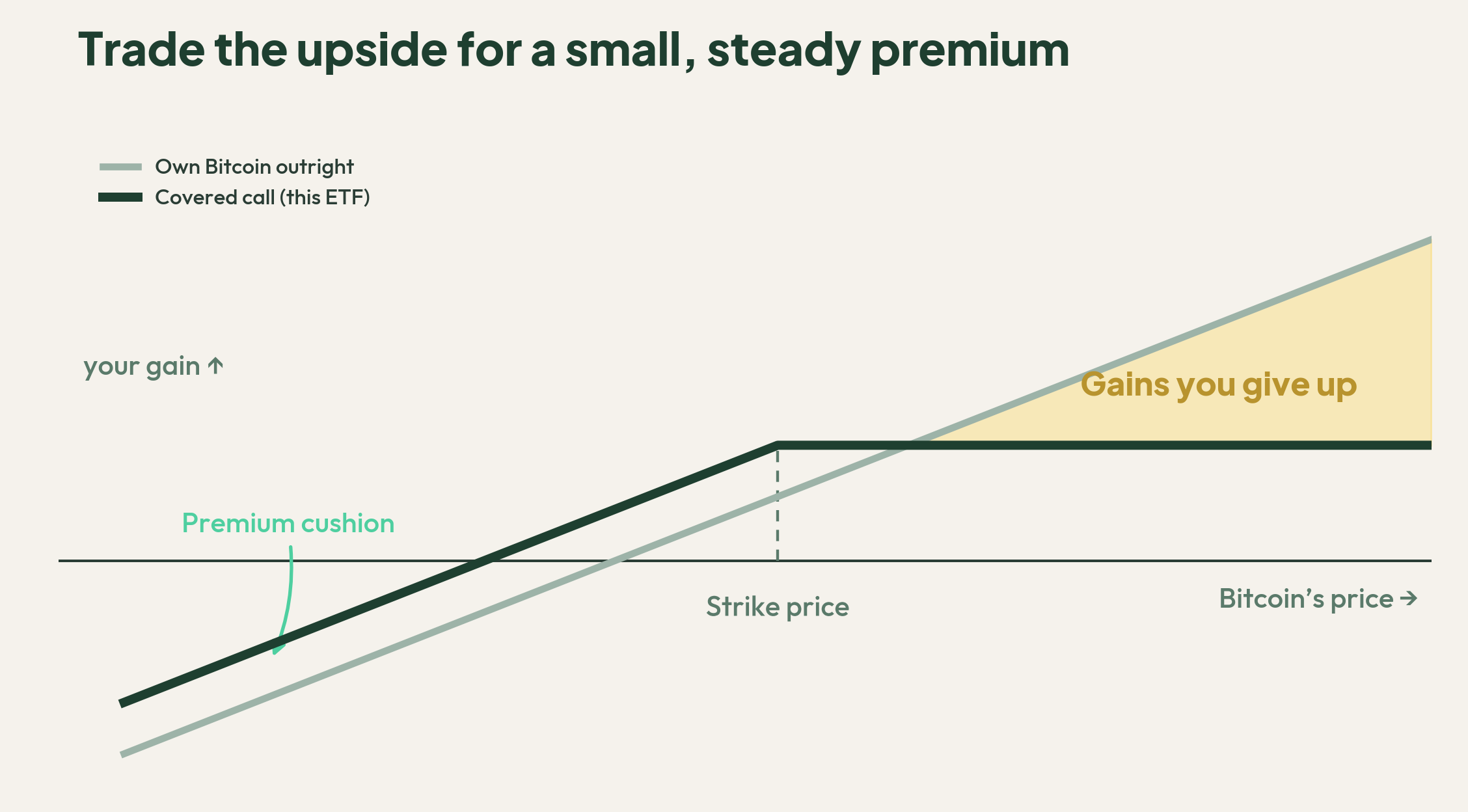

It produces that yield by selling covered calls, and the mechanics are where the trouble hides. A call option is a ticket you sell to another investor. The ticket gives them the right to buy your Bitcoin at a fixed price, called the strike, for a set window of time.

They pay you cash up front for it.

That cash is the premium, and the premium is the “income.”

Herein lies the rub.

Imagine you own a house and you sell your neighbor a ticket that lets them buy it at $500,000 anytime this year, and they hand you $5,000 today for the privilege. Great, now you have a house and $5,000 with two scenarios:

If the market stays calm, you keep the house and the cash. (income! woot!)

If a boom hits and the house is suddenly worth $700,000, your neighbor cashes the ticket, buys at $500,000, and pockets the difference. You collected $5,000 and watched $200,000 walk out the door. 😬

A covered call on Bitcoin is that trade, run every month. You collect steady premiums, and in exchange you agree to hand over the large gains whenever they arrive.

On a quiet asset, that can be a fair bargain.

On Bitcoin, it runs straight into a math problem.

The days that decide the year

Bitcoin doesn’t deliver its returns evenly. It delivers them in rare, violent bursts.

Over the past six years, a buy-and-hold returned a median of about 90% a year. Take away just the ten best trading days in each of those years, and that median flips to roughly negative 25%, with two of the six up years turning into losses.

The whole result lives in a handful of sessions, and those sessions tend to cluster around catalysts you only recognize in the rear-view mirror.

A covered call’s entire function is to cap the up days.

Run it on Bitcoin and you are short the exact days that produce the return, on the one asset most dependent on them. The “keep 70% of upside” promise sounds reasonable until you remember the upside isn’t smooth. If the slice you surrender lands on the few days that carry the year, you haven’t given up 30% of a steady climb, you’ve given up a piece of the rare bursts that are the entire reason to hold the asset.

The averaged-sounding number hides where the loss actually falls.

Selling volatility on a schedule

There’s a subtler problem in the timing.

Selling a call is selling volatility. When you sell that ticket, you’re betting the asset won’t move much, and if it moves hard, you lose more than the premium you collected. Bitcoin moves hard. The price of that bet swings too, expensive in some months and cheap in others.

BITA writes its calls on 25 to 35% of the fund every month no matter what.

BlackRock’s own head of ETFs described the income as something the fund generates “irrespective of market conditions,” which is the problem stated out loud.

Volatility is usually cheapest right after a sharp correction, once the panic drains out and the option market underprices what Bitcoin is about to do, and that’s also the moment a rebound is most likely. A calendar overwrite sells into that window anyway, collecting a thin premium precisely when it caps the most recovery.

A disciplined version of this strategy would sell only when volatility is rich and the trend is genuinely capped, maybe a quarter of the months, rather than every month on autopilot.

The first ones already failed

We don’t have to theorize, because the first generation ran the experiment. YBTC, the original Bitcoin covered-call ETF, returned about negative 28% over the past year and trailed plain IBIT in both price and total return, even through the down stretches where the overlay was supposed to cushion the fall.

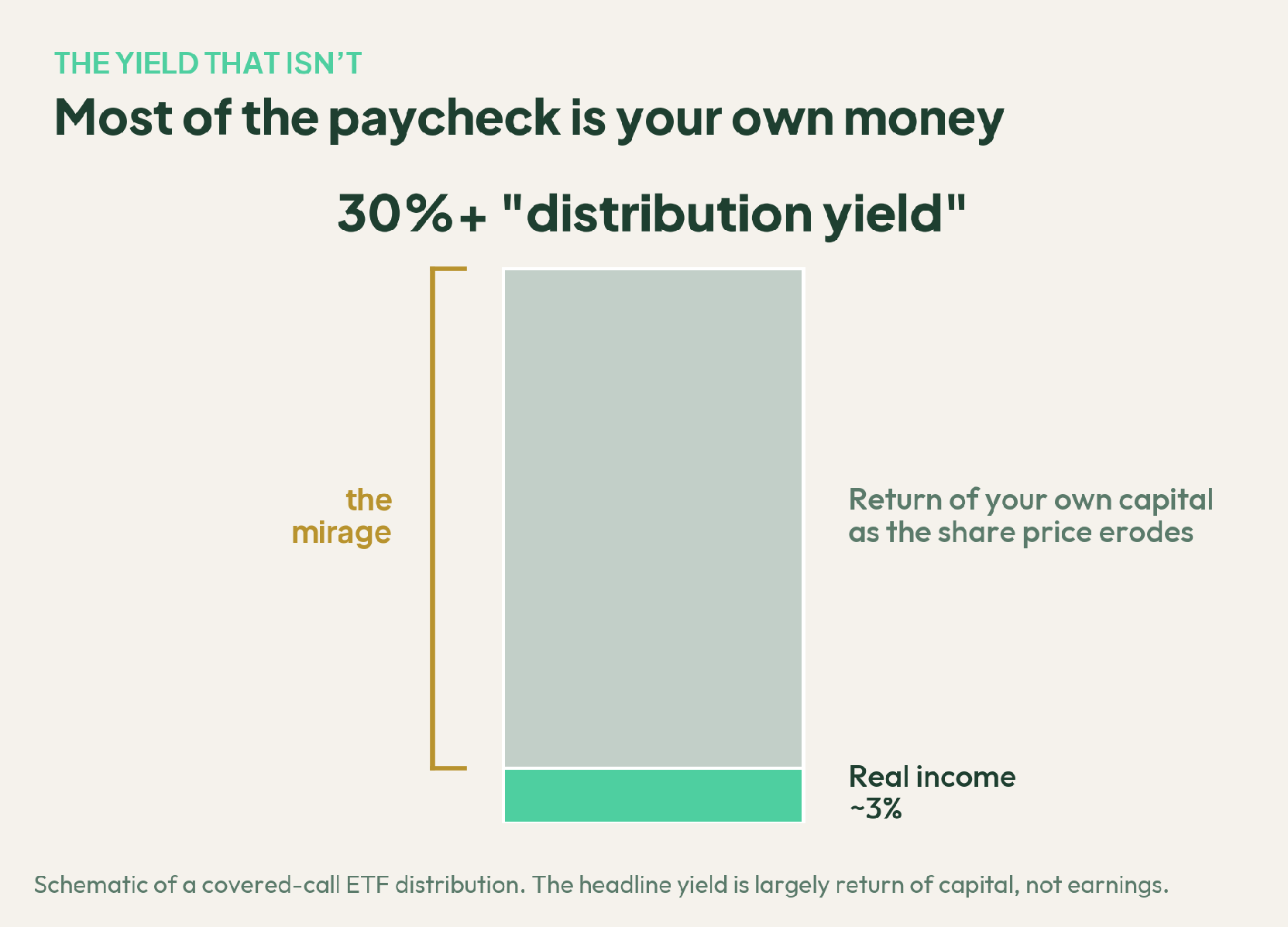

The headline yields are the tell.

A fund can advertise a distribution rate north of 30% while much of that payout is return of capital, your own money handed back to you as the share price erodes underneath it. Strip that out and the real yield can sit near 3%. The paycheck looks generous until you notice part of it is your own deposit.

Then there’s the bill.

BITA charges 0.65% a year against 0.25% for holding IBIT outright, and the distributions are taxable in the year you receive them, while holding Bitcoin lets the position compound untouched until you choose to sell. You pay more in fees to earn less in total return, and you get taxed sooner on the smaller result.

Buffett Framework Question: “Would I sell my best ten days a year for a premium I might not collect?” Put that way, the answer for a long-horizon Bitcoin holder is clear. The premium is small and certain, the upside you hand over is large and concentrated, and that’s the wrong side of the asymmetry you bought Bitcoin to own.

When the trade makes sense

None of this makes covered calls useless.

On broad stock indexes and blue chips, covered-call writing is a respected, decades-old approach, and for good reason. Those returns are steadier and more predictable, the gains don’t hide in a handful of unrepeatable days, and trading the occasional capped month for steady premium is a fair exchange.

Buy-write indexes have run on that logic for years. In a flat or grinding market the overlay smooths returns, the cash is real, and an investor who needs spendable income today might reasonably accept slower long-run growth to get it.

The strategy isn’t broken, but its match with this particular asset is.

Bitcoin’s value case rests on the right tail, and a covered call is a machine for selling the right tail.

When I’ve weighed income options for members in the funds I’ve helped run, the conclusion kept landing in the same place. Income from a volatile, right-tailed asset has to be dynamic, sized and timed to volatility instead of run on a fixed monthly calendar, or it bleeds away the thing that made the asset worth holding.

For most people the cleaner path is plain spot exposure and patience, with any options overlay used as a tactical tool rather than a permanent setting.

Expect these products to multiply regardless.

People want their Bitcoin to pay them, and that wish is understandable. Issuers are happy to manufacture a yield number that markets well, even when total return suffers for it, and Goldman Sachs already has a near-identical fund lined up for July. The demand isn’t going anywhere, and the math underneath won’t change to meet it.

The income is real. The question is what you’re funding it with, and on Bitcoin the answer is usually your own best days.

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.

Sources:

BITA fund mechanics — 0.65% fee, monthly covered calls on 25–35% of holdings, 15–25% target yield, ~70% upside capture, June 16 Nasdaq launch

Bitcoin return concentration — +90% median annual return falling to ~−25% without each year’s ten best days (2020–2025) David Eng analysis, reported by CCN

YBTC returns and distributions — ~22% annualized before taxes / ~9% after taxes since January 2024 inception, −3.45% for 2025, return-of-capital distribution mechanics

Fee comparison and Goldman filing — IBIT 0.25%, YBTC 0.95%, BTCI 0.99%; Goldman Sachs comparable product filing. CoinMarketCap