The 100-Year-Old Receipt That Will Put Bitcoin in Your Brokerage Account

There’s a hundred-year-old piece of Wall Street plumbing that could do something no Bitcoin ETF can. It can hand you a direct claim on real Bitcoin, hold it in the same account as your stocks, let your adviser manage it, never ask you to touch a wallet, and yet be able to redeem back for Bitcoin when you are ready.

It wasn’t built for crypto. It was invented in 1927 so Americans could own foreign companies they had no clean way to buy, and for the better part of a century it has quietly moved trillions of dollars of assets around the world. Now a team is pointing that same machinery at Bitcoin, and the result is a way to own the asset inside the accounts you already have, without the wallet, the fees, or the layers in between.

It sounds boring. That’s exactly why it might work.

The problem you already feel

If you want Bitcoin, you have plenty of options, and none of them quite gives you what you want: to hold Bitcoin the way you hold everything else, in your brokerage account, next to your stocks, where your adviser can manage it and you are not lying awake worried about a lost seed phrase.

Today, putting Bitcoin to work means picking a wrapper, and each one asks you to give something up.

A spot ETF like IBIT: simple to buy, but you own fund shares rather than Bitcoin (the fund owns your Bitcoin), and you pay a fee, as the ETF manager sells that Bitcoin behind each fund share every day you hold it.

A covered-call fund like BlackRock’s new BITA: it pays you monthly income, but caps how much of Bitcoin’s rise you actually keep.

An equity proxy like Strategy: leveraged exposure through a single stock, with dilution and corporate risk stacked on top.

Self-custody: you truly own the coins, and you also own the wallet, the keys, and every way to lose them.

Each one slips a layer between you and the asset. You end up holding a fund’s claim, a company’s stock, or a set of keys you have to guard alone. None of it is fraud. The thing you can buy easily is rarely the asset itself, more often a derivative wearing its costume.

What a depositary receipt does

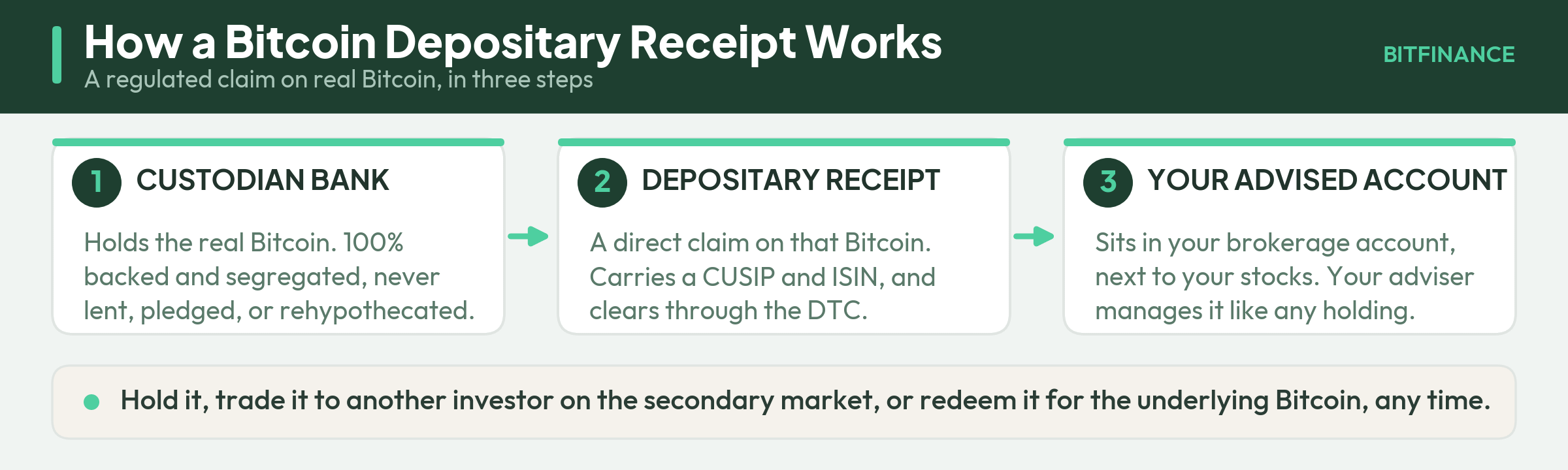

Picture a coat check. You hand over your coat, the attendant gives you a small numbered ticket, and the coat goes in the back. The ticket is light, easy to carry, and easy to hand to someone else. It isn’t a photo of your coat or a rental of a similar one, but a direct claim you can turn in for the real thing whenever you want – not an IOU.

A depositary receipt is that ticket, built for a security. You can hold it, hand it to another investor on the secondary market, or turn it in and take delivery of the underlying asset.

The tool dates to 1927, when J.P. Morgan issued the first one so Americans could own shares of a foreign company without the shares ever leaving their home country. A US bank bought the real foreign stock, held it abroad, and issued a receipt that traded in New York like any other share. You bought the receipt in your normal brokerage account and owned a direct claim on the real stock sitting overseas. Today more than 6,500 institutions use depositary receipts to hold over a trillion dollars of assets this way. It’s old, well-worn plumbing.

Now point that same century-old machinery at Bitcoin.

A Bitcoin IPO without the IPO

A Bitcoin depositary receipt works the same way. A regulated custodian holds the actual Bitcoin, and you hold a receipt that is a direct claim on a set amount of it, one to one, fully backed. Bitcoin makes the model cleaner than a real coat check, because every coin is interchangeable, so you never need your exact units back, just the amount your receipt represents. The receipt carries a Ticker, CUSIP and an ISIN, the same identifiers your stocks use, and it clears through the Depository Trust Company, the pipe that settles almost every share trade in the country. It can sit in a brokerage account, get margined, and move between accounts, and the Bitcoin never touches your personal wallet.

Read that list again, because it quietly solves the whole problem. No fund fee eroding your position. No company issuing shares behind you. No covered call capping your upside. No seed phrase. You hold a claim on real Bitcoin, structured like an ordinary security on the menu.

That’s the closest thing to a true Bitcoin IPO. Not a fund that owns Bitcoin. Not a company that owns Bitcoin. A regulated, brokerage-native receipt that is Bitcoin, one to one, held for your benefit.

BUFFETT FRAMEWORK QUESTION

When you buy a Bitcoin product, what do you own? With most wrappers, the plain answer is a claim on a fund, a share of a company, or a contract on a price. With a depositary receipt, the answer is a direct, fully backed claim on a set amount of Bitcoin held in custody for you. Buffett’s whole discipline is knowing exactly what sits under your position. A receipt gives you a clean answer. A derivative gives you a paragraph.

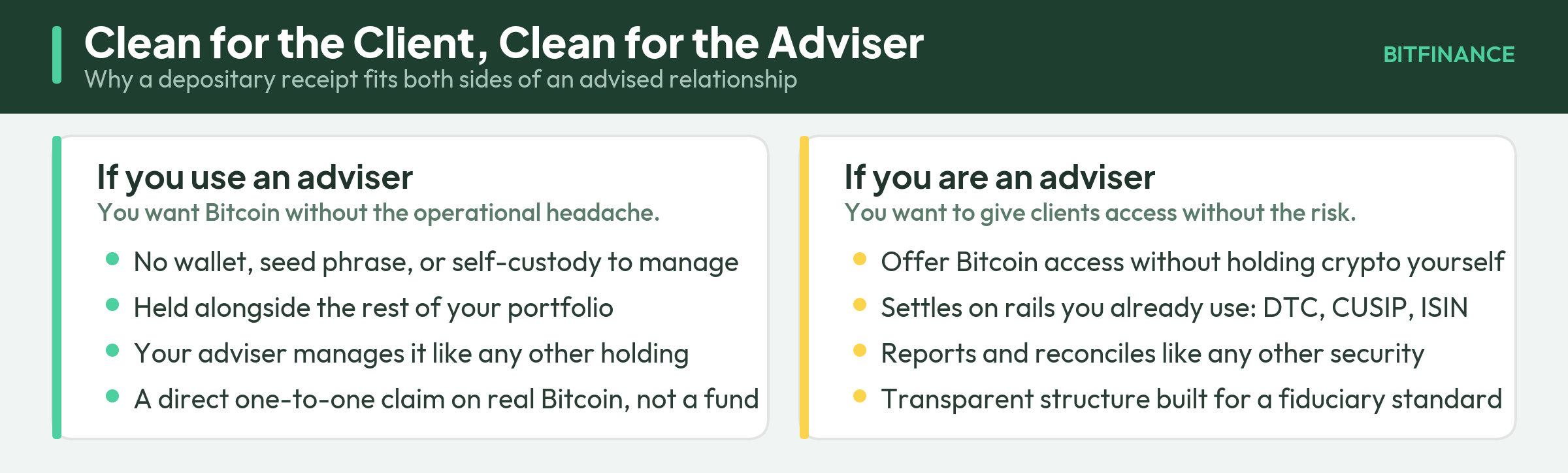

Why this matters if you work with an adviser

This is where the receipt earns its keep, and it’s the part the ETF conversation usually skips.

Say you use a financial adviser. You want Bitcoin in the mix, but you don’t want to become your own bank, manage keys, or explain a hardware wallet to your spouse. With a depositary receipt, you don’t have to. The Bitcoin sits with a regulated custodian, your adviser holds the receipt in the same account as everything else, and it shows up on your statement like any other line item. You get the ownership and skip the operational risk.

Now flip it around. Say you are the adviser. Clients are asking for Bitcoin, and you would like to say yes, but you don’t want to touch crypto custody, take on key-management liability, or bolt an unfamiliar platform onto your practice. A receipt lets you offer access on the rails you already run. It settles through the DTC, carries a Ticker, CUSIP and an ISIN, and reconciles like any security your back office already handles. You give clients the asset without becoming a crypto company.

That two-sided fit, clean for the investor and clean for the adviser, is what turns this from a curiosity into a real on-ramp. It moves Bitcoin into ordinary advised accounts without asking anyone to change how they already work.

This is already being built

None of this is theoretical. One group well down the road is Receipts Depositary Corporation, a Houston firm started in 2022 by former Citi depositary receipt specialists. They issued the first Bitcoin depositary receipt in 2024, built on the same century-old ADR structure: cleared through the DTC, custodied at a federally chartered, OCC-regulated bank, 100% backed, with the underlying Bitcoin barred from being lent, pledged, or rehypothecated. They have since added receipts for Ethereum, Solana, and XRP, and this week they closed a $7 million oversubscribed round led by LiveOak Ventures, with OTC Markets Group, GTS, and others joining, to widen the product to more investors and asset classes. I’m pointing to them to show the category has real builders and real capital behind it, not as a recommendation.

Who it’s really for

This is the part that usually gets lost. The first Bitcoin receipts went to qualified institutional buyers, the banks and funds that have leaned on this structure for a century. That’s not the ceiling, but the proof that the plumbing works.

The whole design points the other direction, toward you. A receipt only beats a wrapper because it can sit in an ordinary advised account, owned by an ordinary investor and managed by an ordinary adviser. A Bitcoin IPO without the IPO matters only if regular people can hold it in the accounts they already have. That retail and advised version is the destination this is built for, and it’s closer than the average headline lets on.

The objective view

A better structure doesn’t win on merit alone. ETFs have distribution, marketing budgets, and a multi-year head start, and a receipt still has to earn its way onto brokerage and adviser platforms before it reaches your statement. That takes time, and none of it is guaranteed.

The appeal, though, is straightforward. A direct, fully backed claim on Bitcoin, cleared through the same pipes as your stocks, custodied by a regulated bank, with no wallet to lose and no fund skimming the position or owning that Bitcoin. For an investor who wants Bitcoin without the headaches, and for an adviser who wants to offer it without becoming a crypto custodian, that is a clean answer to a messy problem.

The tool is a century old, the use is brand new, and the gap between the two is closing faster than it looks.

I’m excited to see where we go from here! Moving on…

This Week in 2 Minutes

Most Crypto Tokens Are Uninvestable by Design (June 16)

The setup I keep hearing is low price plus partnerships equals generational buy. It rests on two mirages and a moat that was never there.

Decentralization removes the moat on purpose, so no cash flow sits under the price and a 98% drawdown is just a number, not a floor. Partnerships prove the tech gets used, not that value reaches the token: California put 42 million car titles on Avalanche, and the fees get burned while the holder gets a headline.

Capitalism takes the open-source rails, runs them privately, and leaves the coin behind. Bitcoin and Ethereum have real network effects; most of the rest are uninvestable by design.

Coinbase Made an AI Your Fiduciary. Read the Fine Print. (June 18)

Coinbase registered an AI agent with the SEC, CFTC, and NFA as an investment adviser. It reads your full account, runs around the clock, and issues explicit buy and sell calls, then the same disclosures say its output may be wrong and the losses are yours.

A registered adviser is a fiduciary that can’t disclaim its duty of care, so claiming the standard and waiving the outcome in one product has no precedent in securities law. Two weeks earlier, Robinhood made the opposite bet: AI to make human advisers faster, with a person kept on the hook.

The commodity advice tier just went free, and the judgment tier, along with the licensed human accountable for it, got more valuable.

This Week’s Winners…🏆

Everyone who buys gas, flies, or ships things. The surprise US-Iran peace framework reopened the Strait of Hormuz and sent oil tumbling at the start of the week, which is basically a stimulus check routed through the pump. Airlines, freight, and the broad consumer all caught the updraft, and this quietly does more for household budgets than any policy headline this year.

The hawks, savers, and the dollar. Kevin Warsh held rates at his first meeting as chair and the meeting pointed to a possible hike in late 2026. Warsh spent years arguing the Fed was too soft, and he just proved he meant it, which keeps fat yields on cash and hands the dollar a credibility bid most people are sleeping on.

The old economy, briefly cool again. The Dow notched a record midweek, and Caterpillar (+3.4%) and Disney (+3.1%) led it higher Thursday. Cheap energy plus a de-risked map is rocket fuel for the unglamorous industrial and cyclical names that the AI darlings made everyone forget.

…and Losers 📉

Bondholders. The “hike on the table for late 2026” line pushed yields up as the Fed held but signaled a hawkish tilt, and anyone who loaded up on duration betting on cuts got a cold shower. The new chair has been warning about loose policy for a decade, so this is a posture, not a one-off.

Small caps. The Russell 2000 lagged and slid about 0.9% midweek while the big indexes flirted with records. Small caps run on cheap money to survive, and Warsh just told them the oxygen might get thinner.

Energy producers. The flip side of the consumer’s gift: crude cratered on the Iran deal, and the drillers and majors handed the gains right back. The same barrel that feels great at the pump is a gut-punch on an energy company’s income statement.

The “safe” blue chips. Even on Thursday’s green day, IBM fell about 4.8%, Johnson & Johnson 2.5%, and JPMorgan 2.5%. When the tape flips risk-on, the defensive and financial names are exactly what gets sold to fund the chase.

What to Watch (June 22)👀

May PCE, Thursday: Warsh’s first inflation test. The Fed’s preferred inflation gauge lands Thursday alongside the final Q1 GDP read, the first print since the hawkish hold. A hot number and the new chair looks prophetic; a soft one and the bond market finally exhales.

Micron, Wednesday: the AI cycle’s reality check. Micron has run nearly fourfold this year on AI memory demand, with revenue expected to surge year over year. If the AI trade is ever going to crack, the memory names usually flash the warning light first, so the guide matters more than the headline.

FedEx, Tuesday: the world economy’s pulse. FedEx reports Tuesday, and boxes moving is GDP you can actually count. Its outlook is a faster read on global trade and the consumer than any government statistic, so watch the guidance, not just the quarter.

Bank stress tests, Wednesday: license to pay. The Fed’s stress-test results come Wednesday and set how much capital the big banks can return through buybacks and dividends. With financials already lagging, a clean pass tends to unleash a wave of announcements that could wake the group up.

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.