$1.75 Trillion Is About to Reprice Six Industries

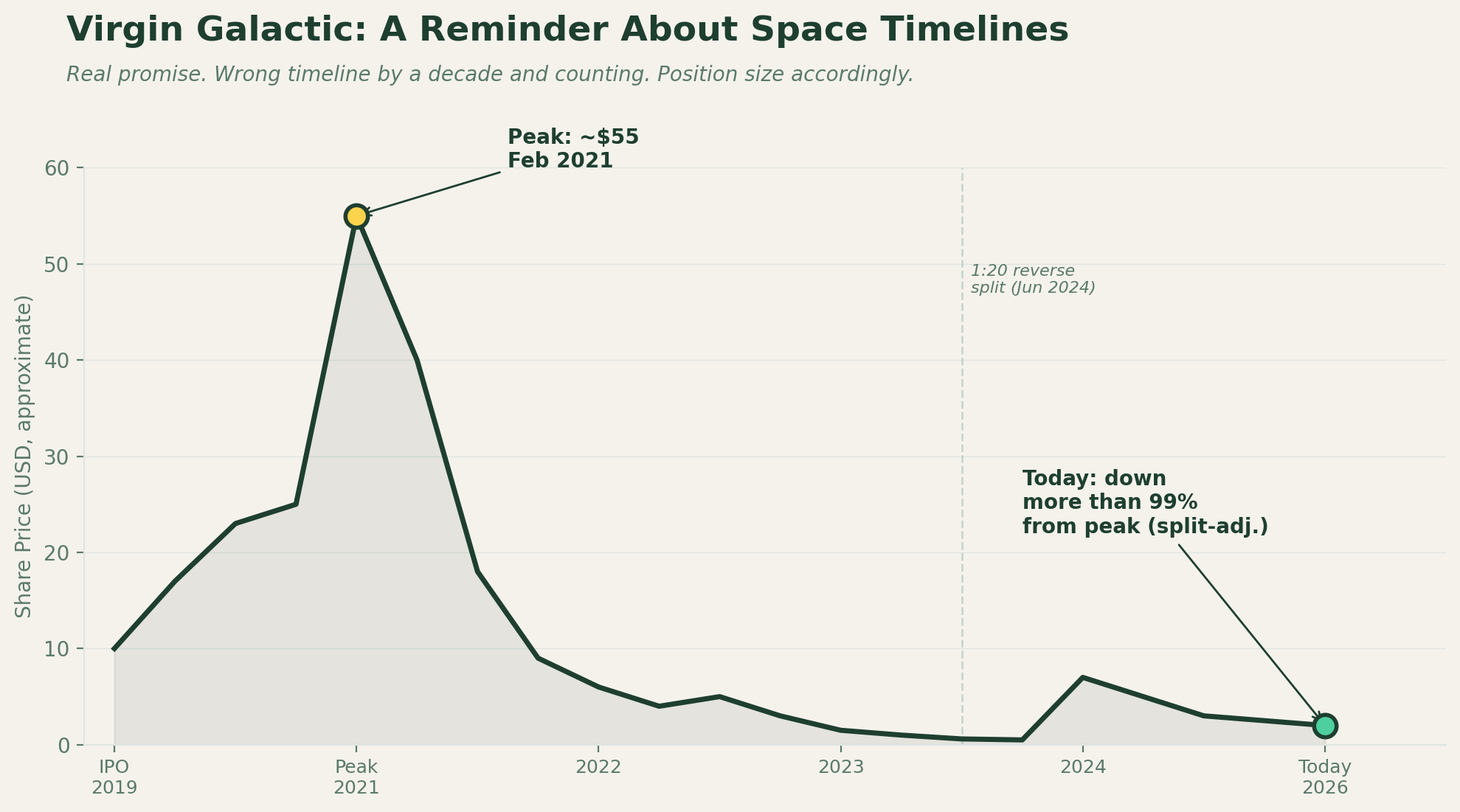

Fifteen years ago, I was a reconciliation analyst intern at Bank of America while finishing my undergrad at Boston University. One of the perks being marketed at the time was a credit card rewards play tied to commercial space travel. Virgin Galactic was supposed to be the first to take regular people to the edge of space. The first commercial flight was just around the corner. Points could one day book a seat.

That was 2011. Virgin Galactic eventually went public, then flew about a dozen paying customers, then watched its stock fall more than 99% from peak.

The promise was real, but the timeline was wrong by about a decade or more.

I tell you this because the space narrative is back, and it’s louder than it has ever been.

SpaceX files for IPO on June 12 at a reported $1.75 trillion valuation, which would make it the largest public listing in history.

Wall Street is going to spend the next six months telling retail investors that space is the next frontier (not just the final one!). Most of that coverage will focus on the rocket companies, because rockets are easy to photograph….but today, let’s dive deeper into the ecosystem of companies building this industry literally from the ground up.

A Map of the Coming Wave

The actual investable space economy is bigger than the rockets, and it’s worth understanding before the SpaceX listing repackages every public name in the sector.

Think of the space economy like building a city from scratch.

You need transportation to get there, builders once you arrive, services that earn revenue once the city is operational, communications to tie everything together, parts suppliers feeding the whole thing, and underneath all of it, the raw materials and power that make the city work.

Six layers. Each one has public companies you can actually own today.

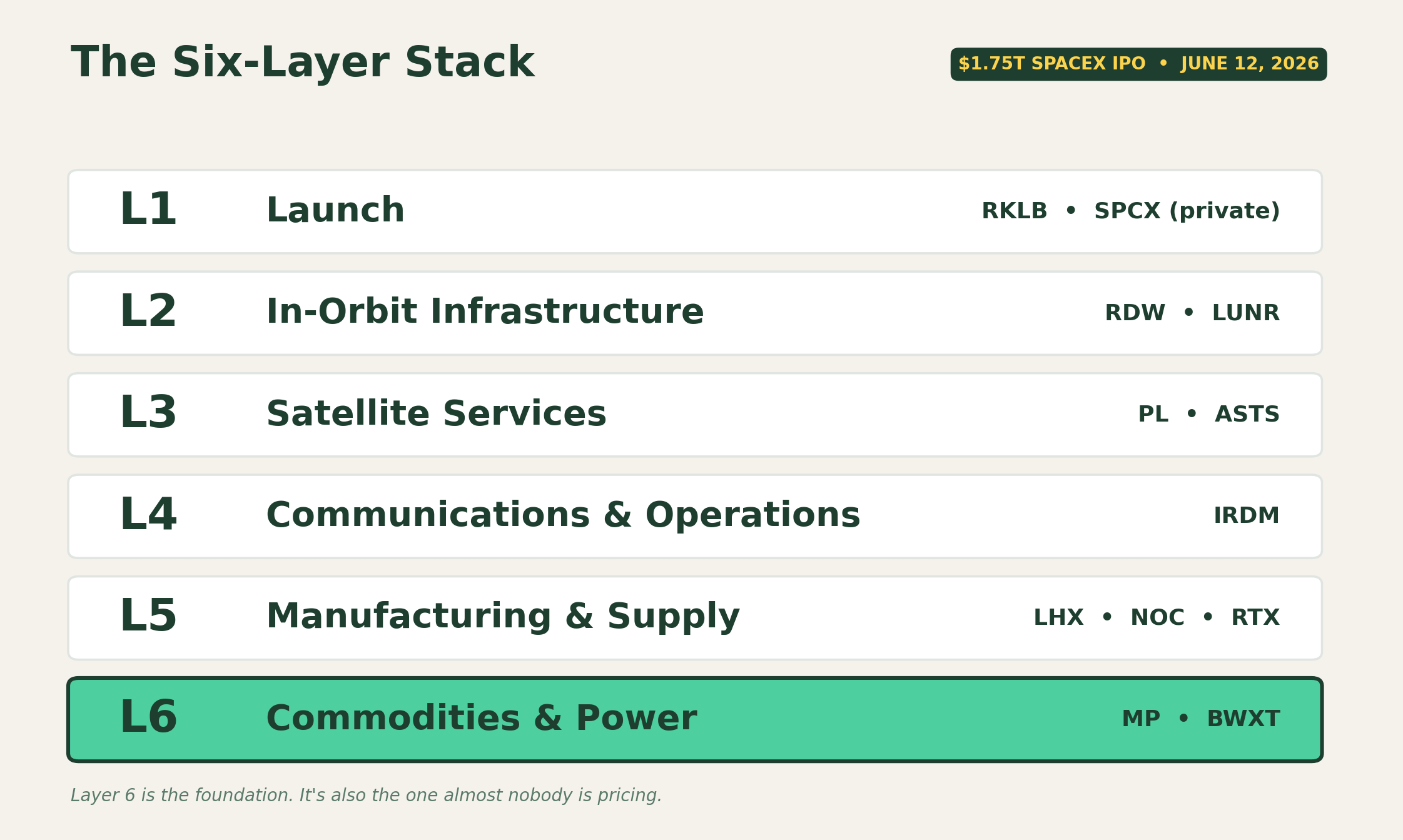

Here’s the 6-layer stack. Pay particular attention to companies the bedrock layer. To me, this feels like the sector nobody is pricing in. 👀

LAYER 1: Launch

Notable pics: Rocket Lab (RKLB)

Launch is the highway system of space. Nothing else works without it. SpaceX owns roughly 60% of global launch market share and is filing for IPO. Rocket Lab is the only public alternative with a credible medium-lift vehicle in development, called Neutron, targeting first flight later this year.

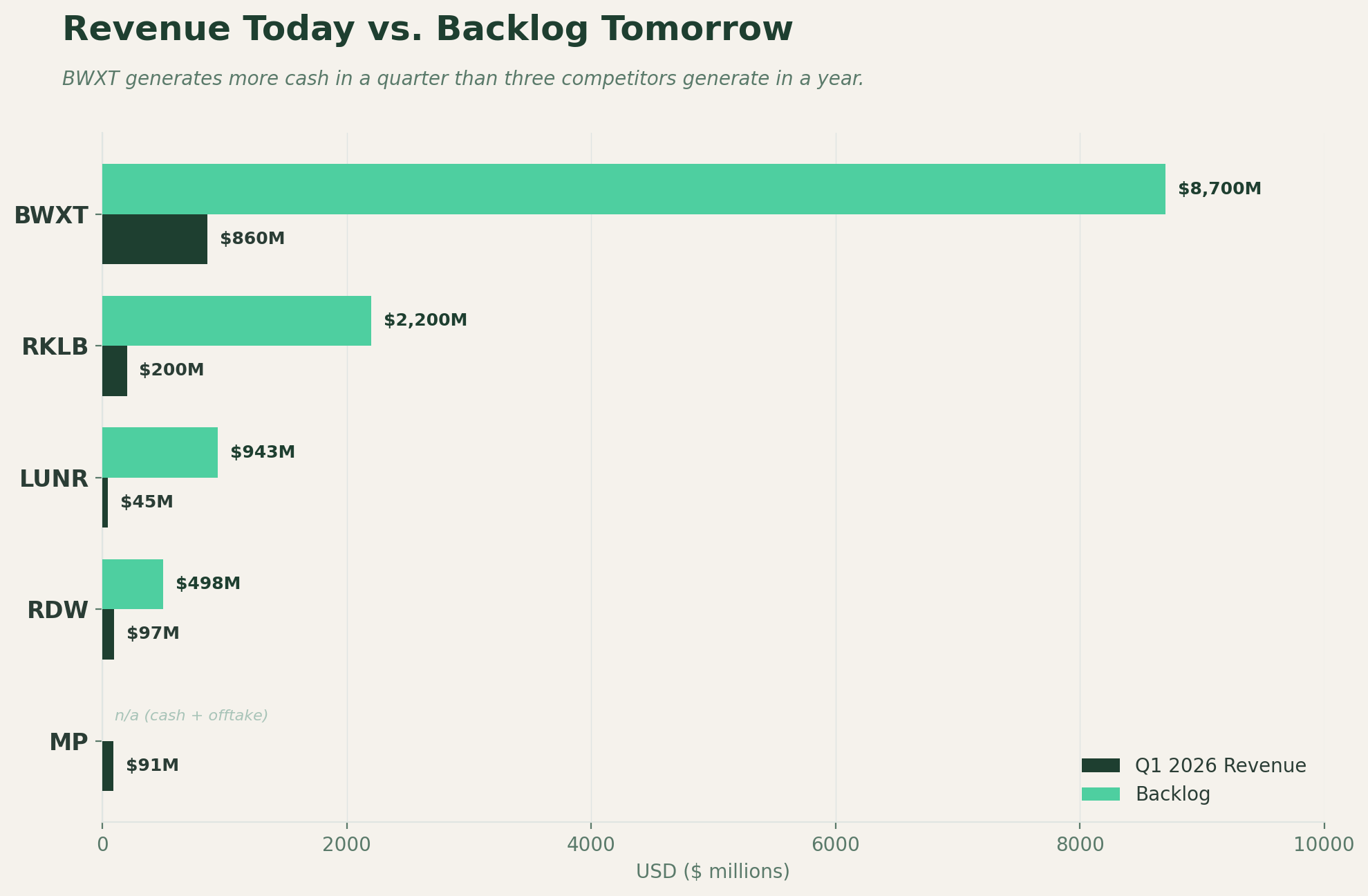

Rocket Lab reported $200 million in Q1 2026 revenue, up 64% year over year.

Backlog stands at $2.2 billion, more than double a year ago. Roughly 68% of revenue now comes from satellite components and spacecraft, not launch itself, which means the company is becoming a vertically integrated space platform rather than a pure launch provider.

The valuation already prices in Neutron flying on schedule, so any timeline slip will compress the stock quickly. Defense exposure through the Golden Dome interceptor program adds an upside catalyst.

Oh this? Nothing…just the stock trading at $7 per share 2 years ago.

LAYER 2 : In-Orbit Infrastructure

Notable pics: Redwire (RDW), Intuitive Machines (LUNR)

Once you’re in orbit, somebody has to build the platforms, the solar arrays, the landers, and the manufacturing facilities that actually operate up there.

Redwire builds parts on roughly half the missions you’ve read about. Q1 2026 revenue grew 58% to $97 million, with a backlog of $498 million. Book-to-bill of 1.92 means new contracts are arriving nearly twice as fast as revenue is being recognized.

The company is still losing money, and the share count keeps expanding, so this is a higher-variance bet that hinges on Edge Autonomy integration working.

Intuitive Machines is the only public company that has actually landed on the moon. Twice. NASA’s lunar program runs through commercial partners, and LUNR has captured multiple Commercial Lunar Payload Services contracts including a $180 million South Pole delivery booked in March.

Full-year 2026 revenue guidance is $900 million to $1 billion. The stock has run 132% in six months, which means sentiment is doing a lot of the work.

LAYER 3: Satellite Services

Notable pics: Planet Labs (PL), AST SpaceMobile (ASTS)

Satellites earn money in two ways; either by selling the data they collect, or by selling connectivity.

Planet Labs runs an Earth imaging constellation with more than 200 satellites and posted record revenue of $308 million in 2025 against a $900 million backlog. Recurring contract value is 98% of revenue, which is the kind of utility-style economics that gets analysts excited.

AST SpaceMobile is more speculative. The company is building space-based cellular broadband that connects directly to standard smartphones from orbit. If it scales, every phone on Earth becomes a satellite phone with no special hardware. That’s the bull case. The bear case is that the deployment timeline keeps slipping and the cash burn is significant.

From a portfolio perspective, it would make sense to treat this as a venture-style position and not a core holding due to the uncertainty associated with this level in the stack.

LAYER 4: Communications & Operations

Notable pics: Iridium (IRDM)

Every other layer depends on satellite networks that move data between space and Earth. Iridium operates the only constellation covering 100% of the planet, with predictable subscription revenue from defense, maritime, aviation, and IoT customers.

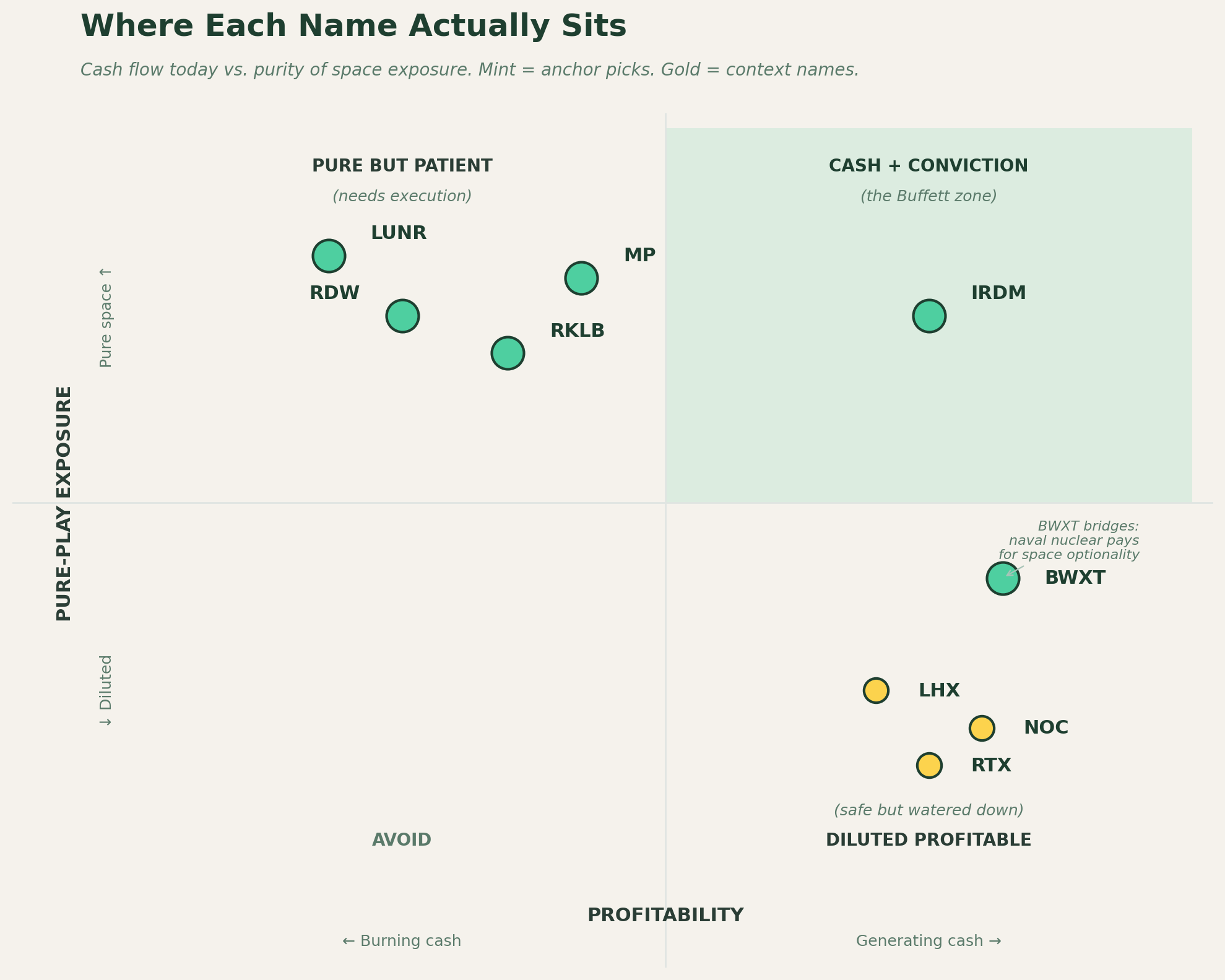

This is the boring, cash-generative name on the list and the kind of business Buffett would actually look at.

Globalstar is being acquired by Amazon for $11.6 billion to power its Project Kuiper rival to Starlink, with Apple’s Emergency SOS feature riding along. The deal closes pending FCC review. Iridium is now the largest independent public name in this layer.

LAYER 5: Manufacturing & Supply

Notable pics: L3Harris Technologies (LHX), Northrup Grumman (NOC), RTX Corporation (RTX), Lockheed Martin (LMT)

Defense primes design and build the satellites, rocket motors, and avionics that everyone else uses. The thesis here is diluted because space is a fraction of total revenue.

L3Harris build classified comms and satellites used by the U.S. Dept. of War.

Northrop Grumman builds rocket motors.

RTX builds GPS satellites…oh, and hypersonic weapons for what that’s worth.

Lockheed Martin runs the largest classified space programs on Earth.

These names give you space exposure wrapped inside a much broader defense portfolio, which is either a feature or a bug depending on what you actually want to own.

LAYER 6: Commodities & Power

Notable pics: MP Materials (MP), BWX Technologies (BWXT).

This is the layer that almost every space investment article ignores, and it’s the one I find the most compelling.

Every satellite needs magnets.

Every magnet needs rare earths.

Every off-world data center, lunar base, or deep-space mission needs nuclear power because solar alone doesn’t cut it past a certain distance or in shadowed regions.

MP Materials operates the only active rare earth mine in the United States.

The Department of War took an equity stake in 2025 and established a 10-year price floor of $110 per kilogram on the key magnet material, which removes commodity price risk from the business model.

Apple committed $500 million for domestically made magnets. Q1 2026 revenue grew 49%, with magnet production set to launch in the second half of this year. Government-aligned, structurally favored, and the only at-scale operator in a market China has historically dominated.

BWX Technologies supplies the reactors that power every US Navy submarine and aircraft carrier. That naval nuclear business throws off predictable cash flow that funds the company’s space work, which includes the Pele microreactor for the Department of War and the DARPA DRACO nuclear thermal propulsion program.

Q1 revenue grew 26%, EBITDA grew 14%, and the company raised full-year guidance. Backlog stands at $8.7 billion. This is the cleanest cash-generative name on the entire list, and the regulatory moat around naval nuclear is essentially impossible to replicate.

How to Actually Use This

Here’s what fifteen years between space narratives taught me.

The companies that survive long enough to matter are the ones with real cash flow today, not the ones selling a compelling future. Virgin Galactic had the better story in 2011. Aerospace primes and satellite operators that nobody talked about had the better business.

The same is probably true now. Two of the six layers, communications and commodities, are where cash-generative businesses sit with structural tailwinds. BWXT, MP Materials, and Iridium are the names worth deeper diligence if you want exposure without betting on timelines. The other layers are higher variance, which is fine if position size matches the conviction.

Note the “The Buffett zone” in the upper-right. Most of the heat in this sector lives in the upper-left.

If I had to build a starter basket from this list, it would lean heavily toward layers four and six, with smaller positions in layer two for the lunar economy optionality. Rocket Lab is a fine name in layer one, but the multiple already reflects most of the upside.

Buffett Framework Question: Which of these companies would I still own if the SpaceX IPO underperforms and the space narrative cools for three years? The answer narrows the list quickly to the names with cash flow today. That’s not a coincidence. That’s the lesson.

Space is going to be a real economy. It’s also going to take longer than the headlines suggest. Both things can be true. Position accordingly.

The biggest IPO in history is going to make space feel like it just became investable. It didn't. It's been investable for years. The companies underneath the rockets have been building real cash flow while the headlines waited for SpaceX.

When the noise hits on June 12, remember which layer the bedrock is on.

Until next time!

🛑 REMINDER 🛑

Quick reminder of what we’re building. Live indicators. The research behind them. The methodology taught alongside the signal. A small room where you leave knowing how the work actually gets done

I’m building the early cohort for when the Discord opens and the first indicators ship. If you want a seat, this is where to claim one.

Interested? Fill out the 30-second interest form here. 👈

Sources:

Q1 2026 earnings releases from Rocket Lab, Redwire, BWX Technologies, MP Materials, and Intuitive Machines. SpaceX IPO reporting from Reuters, Bloomberg, and Fortune.

Amazon-Globalstar transaction announcement, April 14, 2026.

Starcloud Series A coverage from Data Center Dynamics, March 2026. Department of War / MP Materials Price Protection Agreement, July 2025.

Apple / MP Materials $500 million commitment, August 2025.

NASA Commercial Lunar Payload Services contract awards documentation.

BWXT / DARPA DRACO and Pele microreactor program announcements.

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.

This article is for informational and educational purposes only and does not constitute investment, financial, legal, or tax advice. Securities mentioned involve risk and may not be suitable for all investors. Past performance is no guarantee of future results. Readers should conduct their own due diligence or consult with a licensed financial advisor before making any investment decisions.