12 Companies, 83 Days: The Digital Asset Custody Monopoly Is Over

In January 2021, Anchorage Digital became the first (and only) federally chartered digital asset bank in the United States. For nearly five years, they had the market to themselves. If you were an institution that needed a qualified custodian operating under direct federal oversight for your digital assets, there was exactly one option.

That’s no longer the case.

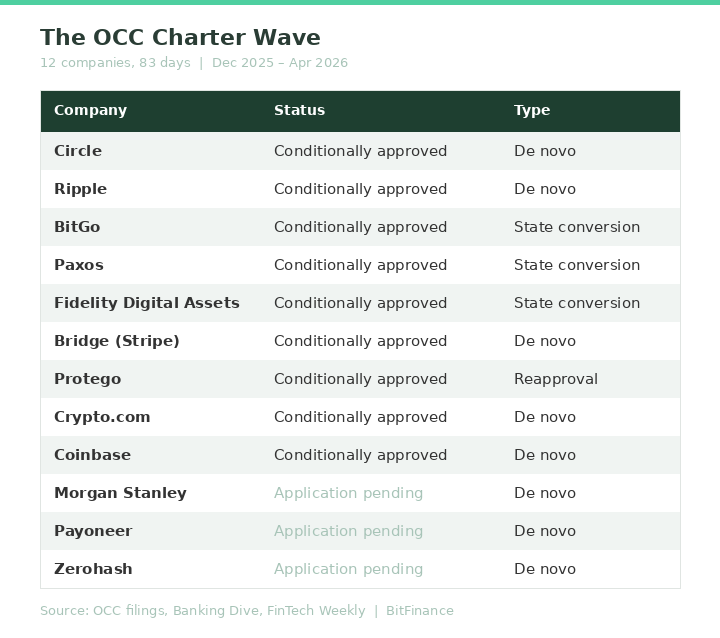

Between December 2025 and March 2026, eleven additional companies filed for or received conditional OCC national trust bank charters. Coinbase received its conditional approval on April 2. The list reads like a who’s who of both crypto-native firms and traditional financial giants. And it tells you something important about where this industry is headed.

The Wave

Let’s put names to this. Here’s who’s in the door or knocking:

I don’t know about you but that’s not a trickle….it’s a land rush.

And on April 1, the OCC formally amended its chartering language to remove any remaining ambiguity about what national trust banks can do. The regulatory text now says exactly what every one of these applicants needed it to say.

What a Federal Charter Actually Gives You

This is worth understanding because most coverage gets it wrong. A national trust bank charter is NOT a traditional bank charter. These companies won’t be taking deposits or making loans. What they get is something more specific and, for this industry, more valuable.

A single federal regulator (the OCC) instead of a patchwork of state money transmitter licenses. National operating authority across all 50 states, and the ability to serve as a qualified custodian under SEC regulations, holding digital assets in a fiduciary capacity.

That last point is the one that matters most for investors.

If you’re a registered investment advisor allocating client capital to digital assets, your custodian needs to meet SEC qualified custodian standards. Until December 2025, Anchorage was the only federally chartered option that could check that box. Now there are 9 conditionally approved entities and three more in the pipeline.

The “Not Your Keys” Argument Just Got Weaker

For years, the self-custody crowd made a reasonable case:

If you don’t hold your own private keys, you’re trusting someone else with your assets, and history suggests that’s dangerous.

They’re not wrong about the history. The collapse of FTX, the failures at Celsius and BlockFi, the Gemini Earn debacle. These were real losses suffered by real people who trusted the wrong counterparties.

But here’s what’s changed. Being your own bank is cool until it’s not. If you lose your keys, there’s no customer service line. There’s no insurance backstop. There’s no recourse. For retail investors thinking about a $50,000 or $500,000 allocation, the risk of self-custody errors is real and non-trivial.

Now compare that to an OCC-chartered trust bank. Federal oversight. Regular examinations. Fiduciary obligations. The kind of institutional protections that traditional investors take for granted with their brokerage accounts. The gap between “hold your own keys” and “trust a federally supervised custodian” just got a lot smaller.

This doesn’t mean self-custody goes away. It means it becomes a choice, not a necessity. And for high-net-worth individuals, family offices, and advisors managing client assets, the choice increasingly tilts toward institutional custody. Because the infrastructure now exists to make that the responsible option.

What Anchorage Built, and What It’s About to Lose

I want to be clear about something: Anchorage deserves credit.

They pursued a federal charter at a time when the regulatory environment was actively hostile to crypto. They invested heavily in compliance infrastructure when most of the industry was still arguing about whether compliance mattered. And they operated under direct OCC supervision for nearly five years before anyone else joined them.

Their CEO’s public statement when the first wave of approvals came through was gracious: “We never wanted to be the last.” That’s the right thing to say. It’s also the only thing you can say when the floodgates open.

Here’s my honest assessment: Anchorage’s moat was primarily regulatory, not technological. Regulatory moats are powerful, but they’re brittle. Once the regime shifts, the advantage can disappear in a single quarter. This is exactly what happened between December and April.

What’s harder to replicate is five years of operational track record under federal supervision.

Five years of compliance infrastructure.

Five years of institutional relationships built on that foundation.

The charter is a license to compete. It’s not a guarantee of competence. Anchorage still has that head start, but the lead is shrinking fast.

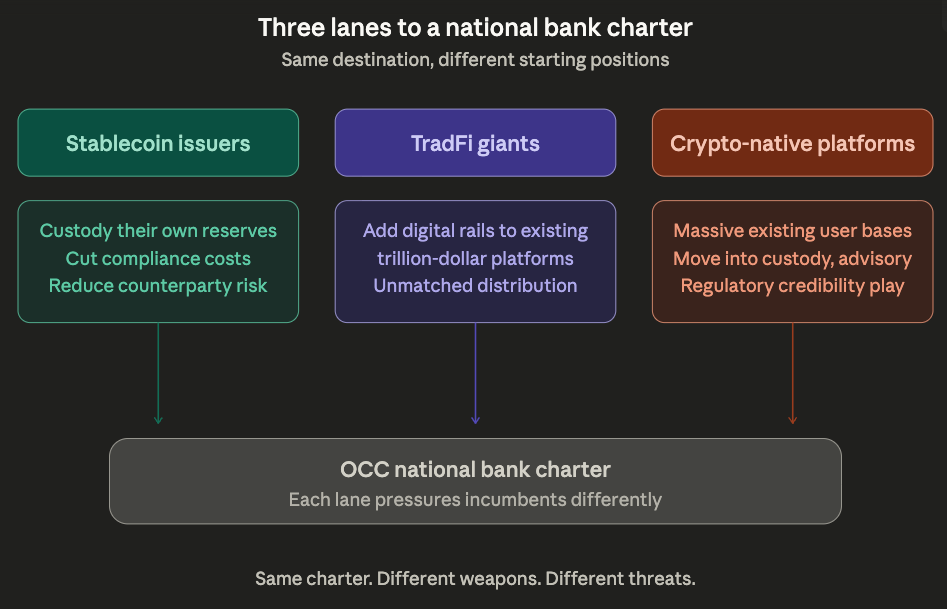

Three Lanes of Competition

The incoming wave isn’t monolithic. These companies are competing from different starting positions, and that matters for how the market plays out.

Lane 1: Stablecoin Issuers

Circle, Paxos, Ripple, and BitGo all issue stablecoins. The charter lets them custody their own reserves instead of farming that out to other OCC-approved entities. That’s a direct cost reduction and a compliance simplification.

Lane 2: TradFi Giants Adding Digital Rails

Fidelity Digital Assets and Morgan Stanley aren’t building crypto companies. They’re adding digital asset capabilities to existing institutional platforms that already manage trillions. When Morgan Stanley offers federally regulated crypto custody to its wealth management clients, that’s a distribution channel nobody else can match.

Lane 3: Crypto-Native Platforms Going Institutional

Coinbase, Crypto.com, and Bridge already have massive user bases. The charter gives them the regulatory credibility to move upmarket into advisory, institutional custody, and fiduciary services. Coinbase was explicit: they won’t take deposits or do fractional reserve banking. This is about custody and trust services.

Each lane pressures Anchorage differently. The stablecoin issuers reduce its captive customer base. The TradFi giants bring distribution it can’t match. The crypto-native platforms bring existing relationships it has to win away.

From Monopoly to Democratized Infrastructure

This is the part that matters most for advisors and allocators.

When there was one federally chartered option, you had a single point of failure for the entire institutional custody ecosystem. Pricing power sat with the monopolist. Service innovation was optional and if you had a problem, there wasn’t anywhere else to go.

What we’re watching isn’t a shift from monopoly to oligopoly. It’s a shift toward genuinely democratized infrastructure.

When Circle, Fidelity, Coinbase, and Morgan Stanley are all competing for your custody business under the same federal oversight framework, prices come down, service improves, and optionality expands.

In the not-so-distant future, putting digital asset capital into safe, secure, federally chartered custody will be as straightforward as opening a brokerage account. The adage about not trusting anyone with your crypto fades when the custodian is examined by the same regulator that oversees JPMorgan’s trust operations. That’s what the maturation of an entire asset class looks like.

What to Watch 👀

The conditional approvals are just step one. Each of these companies still needs to pass pre-opening examinations, establish internal controls, and receive final approval before they’re operational. Some will move faster than others. A few may not make it through.

The CLARITY Act markup in the Senate Banking Committee, expected in late April, will add another layer. The OCC charters and the legislative framework are moving on parallel tracks, and the companies pursuing both simultaneously are the ones positioning for long-term advantage.

Don’t think the banking lobby will stay quiet either…

The Bank Policy Institute, the Conference of State Banking Supervisors, and the Independent Community Bankers of America have all raised formal objections to the charter wave. The political friction is real. But the direction of travel seems clear.

The custody monopoly era lasted five years. In hindsight, it was always temporary. The regulatory barrier was the last thing standing between digital assets and the kind of institutional infrastructure that traditional markets take for granted. That barrier is now gone.

What comes next isn’t just more custodians. It’s more products, more services, and more competition to hold these assets. And that competition is what finally makes digital assets accessible to the advisors and investors who’ve been waiting for the infrastructure to catch up.

It caught up.

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.